As per my understanding, Farmers do not easily switch from one feed supplier to another based on lower price of feed or easy availability etc. If we think from customers view point, initial investment of ~ INR 6 lakhs per acre is a big sizable capital investment. And they would like to go with a reliable and trusted company with a proven track record. I guess, Avanti draws a big advantage here, as they are continuously striving to improve their end product (shrimp feed), for example by reducing FCR from currently ~ 1.4 to 1.2. If FCR is lower, it improves economies of a farmer. May be this has been one of the driving factors for increase in Avanti’s market share in over supplied feed market.

Another advantage which i see here is off take of shrimp from farmers by Avanti. With their target to increase the contribution of processed shrimp to 40% of their annual turnover in coming years (currently being 15%), Avanti is well poised to address multiple issues and turn them to great business opportunities. With a definite off take arrangement from a big player like Avanti, this would assure farmers of steady revenue and would remain loyal customers to Avanti. This would also help Avanti address pesticide issue with farmers and continue to maintain their track record clean.

At some time in future, Avanti has indicated to enter fish feed business. This in my opinion would draw heavy competition for Avanti from major players (like Cargill etc). This any ways has not yet figured in current valuation.

Industry runway in my opinion is expanding with reports of China currently importing, rise in volumes from US. Icing on the cake would be rise in domestic consumption of shrimp (which is currently low and may take some time).

Of course, risks as detailed in this forum extensively (which I am not repeating again here) continue to remain. Also, high profit margins during last few quarters could be an aberration due to lower input costs and could see some correction in the coming quarters. Again, any temporary setbacks in the business due to any headwinds in future could be handled well by Avanti, thanks to their strong balance sheet position.

IMHO, an interesting year ahead for Avanti/investors.

Disc- invested in Avanti. Views are biased. Not a buy/sell recommendation. Please do your own due diligence.

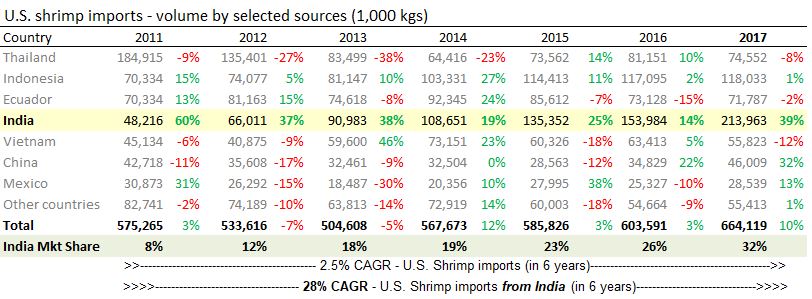

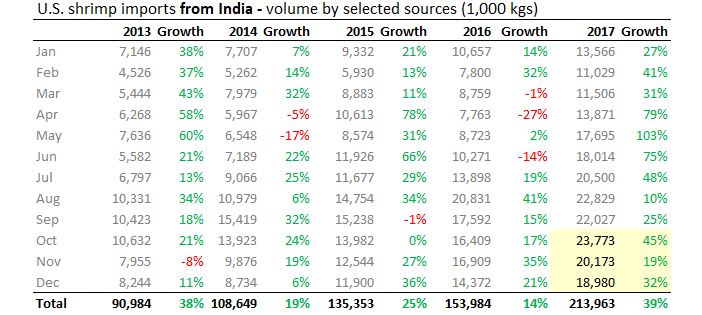

Shrimp exports to US in Dec 2017 were at 18,980 MT (Dec 2016- 14,315). Overall, CY 2017, total exports from India to US is 213,963 MT ( 39% growth over 2016). Interesting aspect to note is that no other country showed such high month on month growth in exports like India. And for the full year, only China’s export growth was 35% closest to India (though in absolute numbers Indian exports are 4.5 times higher than China). Few other countries like Argentina, Honduras growth is 50-70%, but absolute full yr volumes is low.

Definitely good results… but as per concall mangement gave guidance of 5-8% processed shrimp margin and 10-12% feed margin… they are consistently cloaking 14%+ Net margin. Is this margin sustainable?

Also, they have guided for sales of about Rs 7000 cr (1 Billion USD) sales by FY 2021-22. At this growth rate, they will easily beat their guidance. Are they just being conservative or are they seeing some competition or slow down in sales going forward?

Disc: Not invested. Looking at it as long-term investment prospect.

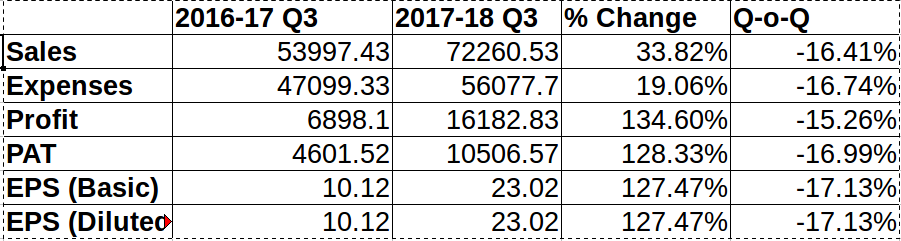

OPM continues to be around the 22% mark like the last two quarters. Owing to seasonality QoQ revenue has dropped. The amount of drop is similar to Q2-Q3 of FY17 (18% vs 17%) so I think that’s in line with what’s to be expected. YoY of course is great with 32% rise in revenues and 128% rise in PAT. Overall pretty solid numbers. However processed shrimp contribution to profits has reduced significantly from around 22% to just 8%. It looks like Net margins on the processing business is deteriorating. Not sure what might be the reason.

Nice catch. If you compare the processing margin with that of Apex, it looks very low. Apex’s op. margin is around 12% where as it’s 7% for Avanti. Not sure how feeds business is still giving them 22% margin (positively surprised) even when management cautioned us that it was not sustainable in Q2 call.

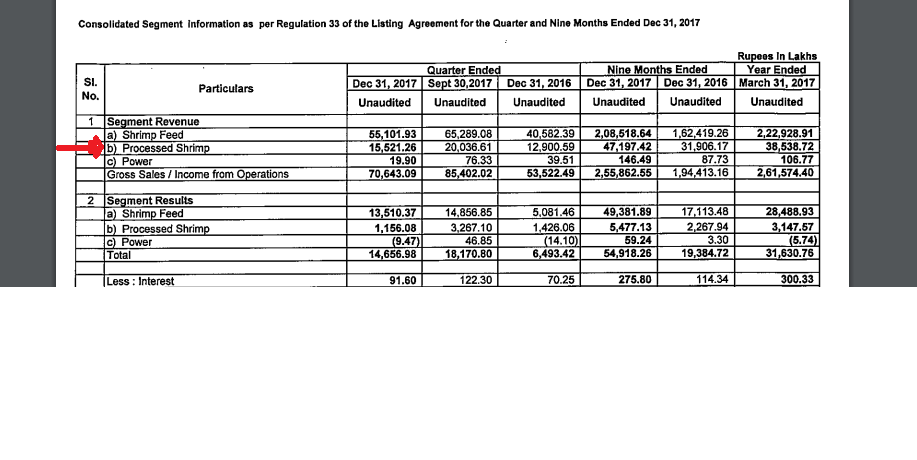

Yes the segment-wise numbers have some interesting info.

For shrimp processing

PBT Margin Dec 31,2016 = 11%

PBT Margin Sept 30,2017 = 16%

PBT Margin Dec 31,2017 = 7%

Revenue contribution Dec 31,2016 = 24%

Revenue contribution Sept 30,2017 = 23%

Revenue contribution Dec 31,2017 = 22%

Profit contribution Dec 31,2016 = 22%

Profit contribution Sept 30,2017 = 18%

Profit contribution Dec 31,2017 = 8%

So revenue contribution is almost same but margins being down, the profit contribution has deteriorated. When comparing PBT margins, last couple of quarters Apex seems to have clocked around 11% so Avanti’s 7% does seem quite less.

UPDATE: This post has been updated to change Net Margin to PBT Margin and also the conclusion because on PBT Margin basis, Avanti’s PBT margin on shrimp processing is lesser and not same.

Hey nice observation. @Donald a few months ago had mentioned that the processing business usually has a couple of 100 basis points lower margins. So like you have explained last quarter was an outlier perhaps.

3.Sustainable Margins

As per Management, in good years (global shrimp prices not contracting - affects the farmers/and feed players too) 10-12% were feasible in Feed segment. Processing is generally at least a couple of 100 basis points lower margin, so processing could see 8-10% margins, or less. In bad years (global shrimp prices contracting) feed segment margins could be between 8-10%, and processing could fall to 6-8%, or less.

Sorry for asking but where to see the net margins from the results which were out? i cant find them anywhere…if there are not there…can you please let me know how to calculate it?

@Mahendra243 - Just divide segment results (PAT) by segment revenue for the net margin. For the contribution, divide the individual contribution by the total contribution.

It is PBT because the Rs.16,182.82 number matches between the PBT in consolidated results and the profit before tax as mentioned in the segment results. Please see these two sections in the two tables.