Conference Call For Investors On 24.05.2017 At 4.00 PM and Investor PPT (only 4 slides)

2 Likes

Fisheries sector expected to touch Rs 1.5 lakh crore by 2020: Assocham -

https://www.evernote.com/shard/s228/sh/68bab2a5-491a-4453-bc78-d19f68db1180/ce939216a0d84d7d1b48e47118fd4114

3 Likes

Could be an issue with the firewall on my side, but unable to browse the link currently!

1 Like

Q4FY17 Concall notes:

-

Major reason for increase in feed business: Increase in volume and decrease in raw material prices.

-

Year was favourable. Farmers were happy with performance.

-

2016 was good, rains were good, prices were good. Current calendar year - as its evident from Q4, the season has started early and on a good note. Expect the year to be good.

-

Further expansion of 50k tonne in feed. Current capacity of 4.5lac mt.

-

Feed is excluded from GST.

Our feed is of very good quality + technical support to farmer has been the reason for consistent increase in market share. We should be able to achieve 85-90% capacity utilization.

Historically margins were 10-11%. Should this quarter be aberration? What is long term?

Sustainable margins have been seen around 10-12%

- We retain the client base and keep increasing the base due to quality and support

- Profitability is due to feed prices being stable. RM has come down.

There is some economies of scale. But increased margins mostly due to fall in raw material prices.

Roadmap for 60:40:

3 pillar approach:

- Increasing feed market share. 42-45% current to over 50%.

- Processing unit added 15,000 TPA. Value added products with better margins.

Will should be able to achieve full utilization in 2-3 years - Entering fish feed business.

GOI supporting it. Has good future.

Studying the total demand supply. Nothing done as of now.

300 Crore cash in book:

Using it for working capital. High profitability due to no debt.

Keeping short term deposits with MF for capex in fish feed and other expansion. Some good planning over next 1 year.

RM Prices in Q1FY18:

Raw material prices haven’t seen any big change. Remaining stable. So can expect good EBIDTA in coming quarter as no much difference currently.

Dip in processing unit:

Because shrimp harvesting starts in April-May and then processing.

Margins in processing:

5-7.5% sustainable margin. 10% if good value added product. Still working on that, doing trial runs. Yet to stabilise.

Feed capacity utilisation:

We are using 85% capacity. Will utilise fully.

Feed market in India:

10-15% growth in industry. Due to quality and support, we are getting new area as well as conversion of farmer.

Shrimp pricing:

Stable for last 8-10 months. Depends on world wide situation.

EMS concerns:

Disease risk is there but the Indian farmers have learned the lesson and they take effective measures to safe-gaurd and follow best aquaculture practices. If good practices are followed, EMS shouldn’t happen. We haven’t seen EMS in India.

Market share has increased. WC is negative. Is there more competition?

20 feed companies are there with capacity of 20lac tonnes. Yet we have taken market share.

We are keeping our prices stable. We are not reducing prices or offering discounts.

Our quality is good and we are confident that our clients will stay.

Those who are not able to sell offer discounts and credit days. But we have loyalty of customers.

50k capacity added is already implemented. Seeing 85-90% utilisation on increased capacity.

Advance from dealer network: Only around 4-5 crore.

Processing: commissioning was to happen in march, but due to approvals and trial production we should start around June.

350-400 crore revenue

Opportunity for shrimp:

- West bengal and Orissa have grown in last 1 year. Gujarat is attractive.

- We may look into exports to Bangladesh next year.

- As long as demand for sea food across world, we don’t see saturation.

- Govt is encouraging more fisheries and aquaculture.

CAPEX:

170 Cr in 2017. 70 was feed (includes 50,000 capacity) and 100 for new processing line.

2018: 25 Crore. In next 1 month or so for Hatchery.

Feed sales volume: 3,40,000 tones in 2017. 93,000 for Q4FY17.

Working capital:

80% is cash sales. 20% is 1month credit.

Fish meal cost:

100-110 during the year.

Currently around 80.

On Processing business - we usually go for spot business - usually for 2-3 months. We do have about 15 customers like Red Lobster etc

45 Likes

Thanks Ayush…Captured the important points well

_Thanks. I’m a bit confused re one thing and forgive me for my ignorance - the rationale behind diversifying into processing has been that it’s a high margin business whereas 5-7% in processing is lower than 10-12% in feeds. What am I missing here ?

Need guidance on the change in mix to 40:60 (processing:feed) from current 15:85… Implies 385:2346 goes to 2500:3800… This is assuming 10%pa growth in feed which needs a 45%pa growth in processing… Isn’t very high expectation?

Assuming growth is achievable n 10% blended margin, 630 would be ebitda in fy22… Giving 20x by being generous as it is market leader n good execution the EV is about 13500 cr (from current 5800 Crs)… 18% pa compounder!

2 Likes

3 Likes

4 Likes

Meeting a shrimp processor next week. please let me know if you have any questions related to the industry/business.

3 Likes

The thesis for investment has shifted from the growth in the feeds business where the company has captured high market share to shrimp processing segment now. Shrimp processing is a commoditized business and the most capital intensive in the whole value chain. Its a low margin business and increasing share from processing segment is likely to reduce the ROCE going forward. I have been told that the most amount of profits in the value chain are captured by farming. Does the company has its own farms or is getting into contract farming for its produce?

3 Likes

In one of the recent interviews the Chairman of Avanti quoted that they don’t have any farms.

They sell feed to farmers and buy shrimps from them.

Best regards,

Django

Hi Friends,

Avanti has done extra-ordinarily well in Q4FY17. Before taking a call, I was waiting for Q4FY17 results of other players of this industry to see whats happening and some of the things are very very interesting.

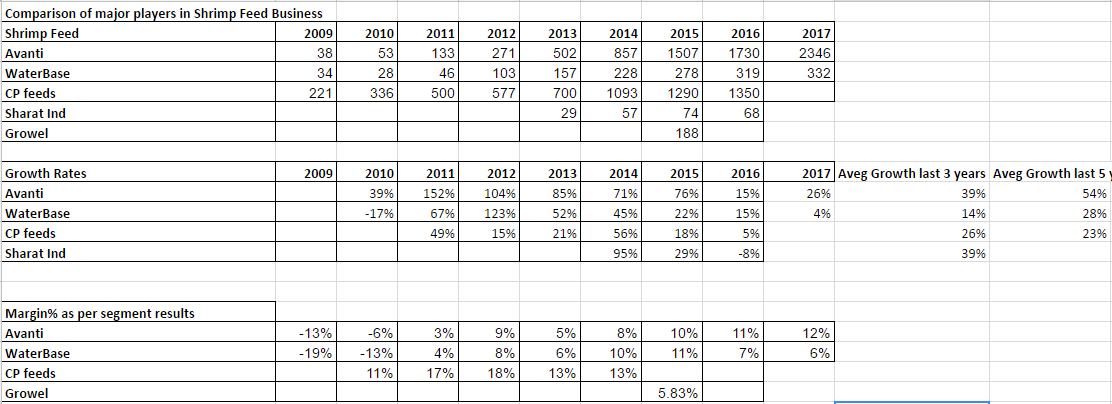

Avanti has grown the fastest despite being the biggest players in the feed segment (7 times bigger than the 3 rd largest player of the industry Waterbase). So despite being at 45-50% market share, the company continues to grow at high rates and gain market share. Plus the company continues to be more profitable + the working capital keeps getting reduced. So in a way this feed business is a super cash cow! There is contrasting difference between the performance of this company and others. I’m sharing the updated comparative analysis sheet:

The difference in margins between Avanti, Waterbase & Sharat and the working capital requirements is contrasting!

Yes, fall in raw material prices has helped Avanti in margin expansion and one doesn’t know how long it is sustainable but its interesting to see that others like Waterbase, Sharat Industries haven’t benefitted - they have neither been able to grow nor expand their margins (surely they should too benefit in coming times but its surprising to see the difference in this qtr). So probably, Avanti is able to capture this benefit due to its brand value, preference with farmer, strong distribution network etc and has not been under pressure to reduce the prices and pass on the benefits. It was heartening to see that the company has undertaken expansion of another 50k tonne in capacity despite a big expansion done recently of 1.25 lac tonne and they seem confident to be able to utilize this capacity. So for FY18, we may see another 25% growth in the feed segment (co may do 80-90% utilization of the full capacity vs 3.4 lac tonne done in FY17)

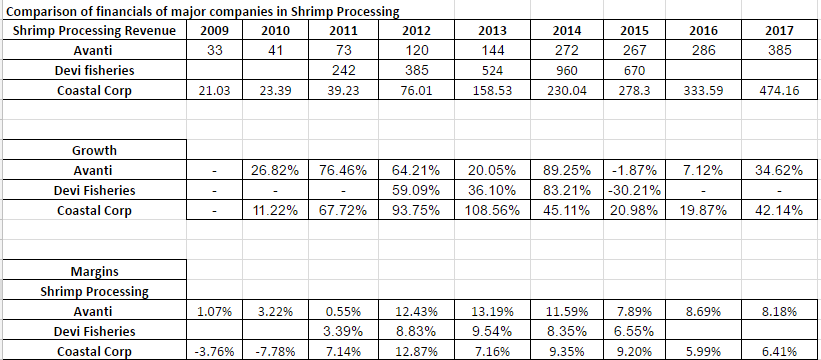

Coming to the processing side of the business, the management seems very confident on scaling up with the new plant. They aim to do 350 Cr in FY18 and probably 1000 Cr in 2-3 years from new plant. Here is the updated comparative sheet:

I think Avanti can do well here too, as they have huge amount of cash surplus and they are trying to focus on the value-added segment (though it will be small to start with) but all the other companies in this area are under lot of debt and have to incur related expense while Avanti will have advantage of own funds.

On valuations - Yes, the valuations are no longer cheap, as in past ![]() Lets see how things evolve.

Lets see how things evolve.

Do share your views

Regards,

Ayush

Link to results of Waterbase - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/f559c641-6773-4dc7-ae07-e5031319f8a1.pdf

Link to results of Sharat Ind - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/34a6f270-b753-487e-814b-7f6335c7267f.pdf1

Link to results of Oceanaa Biotech - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/11f4346c-9fb7-471d-b2c5-442ba7303b8c.pdf

Link to results of Coastal Corp - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/88274f24-3cd7-4cbd-80ab-fc566cbdf2bb.PDF

40 Likes

I think, they will have to pass on the benefit of lower RM prices. Despite the noise or positioning of feeds and integration with farmers; feed is essentially a commodity business. Also, historically, Avanti has passed on both the increase/ decrease in RM prices; at times with a certain lag. So remarkable fourth quarter results should be seen as an aberration with margins normalizing towards 1Q.

Its processing business will ramp-up, but the key to not is that Thai Union owns 40% stake in the business; so accruals to Avanti would be in the range of 60%.

There is no doubt Avanti has done exceedingly well - established a sort of a “Brand” in a commoditised market, where they had the advantage of being “close” to the farmer and constantly monitoring farmer productivity/processes in local farms, monitoring own and competitor (CP) FCRs, supporting the farmer all the way. They executed extremely well and continued to add distance to their peers - in a field where big MNCs and other Corporate players like Waterbase have (relatively) faltered! Full marks to them. I am a big advocate of Avanti’s business model/competitive strengths, despite the “mis-perceptions” about the seasonality/disease perceptions of the sector.

Now Shrimp Processing part really needs to be questioned hard. I keep wondering about some facts about the nature of the business/complexity. Not sure we have done enough diligence, or have most of the data-points that we need to collect.

1.Competitive Strategy/Positioning

Shrimp Feed was an Oligopoly situation, and Avanti started running away with leadership position around 2013 onwards . There were/are unconfirmed reports of a price-cartel situation among top players. In 2015 they could raise prices from Rs 50 to Rs 74, almost at will

Shrimp Processing - the situation is reversed. Avanti is among one of the many players, and a late entrant. There are several players bigger than Avanti operating in the market for many years with established relationships with customers abroad. Avanti will have to scale up business from scratch. We probably can’t see any distinct competitive advantage that Avanti will enjoy vis-a-vis entrenched Competition - even with Thai Union tie-up.

2.Scaling up Capacity/Complexity

While we can go into the capital requirements/intensity numbers, it is more important to perhaps to note the complexity differences. Unlike feed segment, shrimp processing scale-up is directly linked to labour scale-up. Labour sourcing/and keeping them occupied (contracted) through lean seasons at a much higher scale of business than the 380 Cr today is a major challenge. It is even more difficult for value-added processed products, as skilled labour/training is scarce. We were told during our primary field-research, that world-wide value-added segment sales were no more than 20-25%. Even a very competent player like Devi Sea Foods (only 0% CVD company in US market from India) does value-added less than 20%.

It will be interesting to find out why Devi Sea Foods has seen scale-down in business during 2014 to 2015, and what is the status now?

3.Sustainable Margins

As per Management, in good years (global shrimp prices not contracting - affects the farmers/and feed players too) 10-12% were feasible in Feed segment. Processing is generally at least a couple of 100 basis points lower margin, so processing could see 8-10% margins, or less. In bad years (global shrimp prices contracting) feed segment margins could be between 8-10%, and processing could fall to 6-8%, or less.

Having said that, it should be noted that it is an extremely nice position to be in the lifecycle-maturity of a business - when you are close to saturating market coverage in one segment, and throwing out significant Cash - you have another segment opened up - which is capital-hungry, and probably can continue to absorb significant amounts of capital at decent return ratios, for a number of years. Speaks a lot about Management Savvy, in my book!

It is good to keep faith in Managements with an excellent track record like Avanti. Let’s not forget TUF accepted a minority shareholding in the JV - when asked they said, we have complete faith in Avanti Management - they are the Boss in Indian Market. Remains to be seen how scale-up happens. The Management is no doubt extremely confident - but we should do more to establish why they are so confident, or come away puncturing a few holes on the dramatic scale-up envisaged.

27 Likes

Ayush,

Its a great feeling to see you share YOUR MIND on this forum…again. Reminds me of the earlier days when you were actively doing this. Really hope those days come back. Somehow, you and the other senior members had pulled back in the last two years (just when I joined) so I missed the fun…live. But reading your previous msgs in various threads was truly enlightening. You have no idea how much it helps this community to know “How great investors think”. This one msg of yours truly speaks your mind. Having seen such a msg after a long time I couldn’t hold back from appreciating the good work you are doing. Pls do keep sharing your thoughts proactively…on not just the stories working well like Avanti but also the ones goig thru tough times like MPS, AYM, Mayur, Kitex, etc. Sharing info, news is good work but sharing your mind is great work and sets you apart from other great investors. Hats off to you and thanks again for your generosity.

Warm regards

Rajesh Rajput

15 Likes

Avanti added to MSCI small cap index http://www.indiainfoline.com/article/news-top-story/msci-india-index-msci-index-changes-15-stocks-added-while-11-deleted-in-small-cap-index-117053100675_1.html

3 Likes

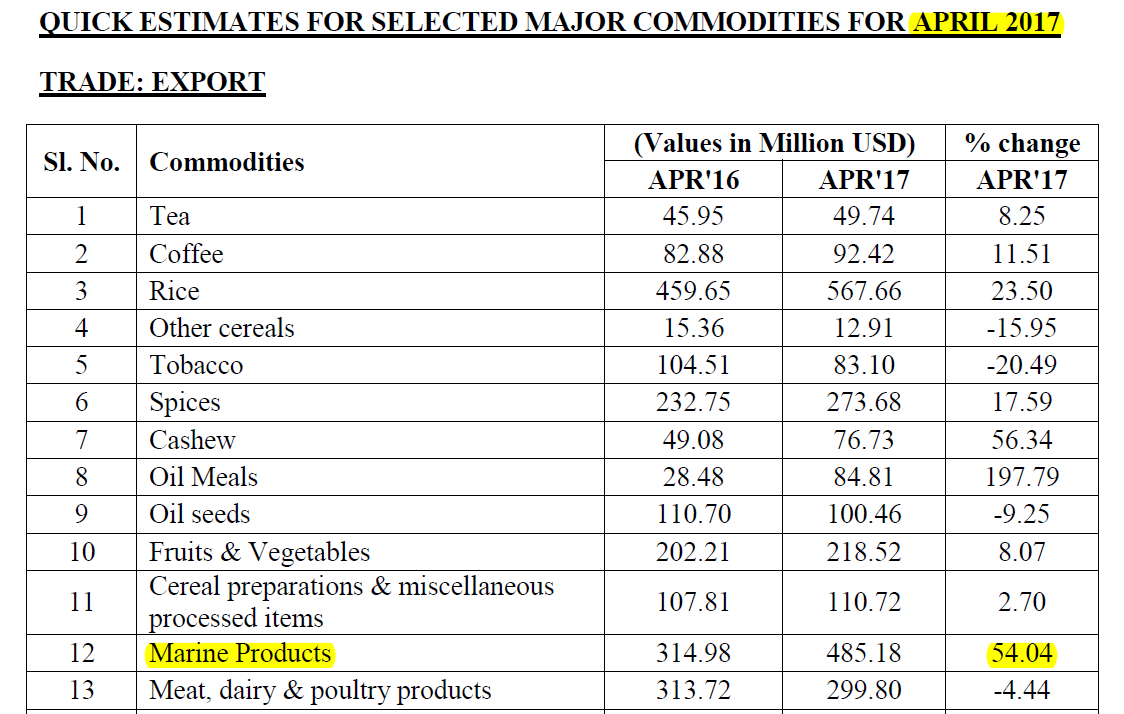

A strong start to FY18 with solid growth in Marine products exports of 54%.

13 Likes

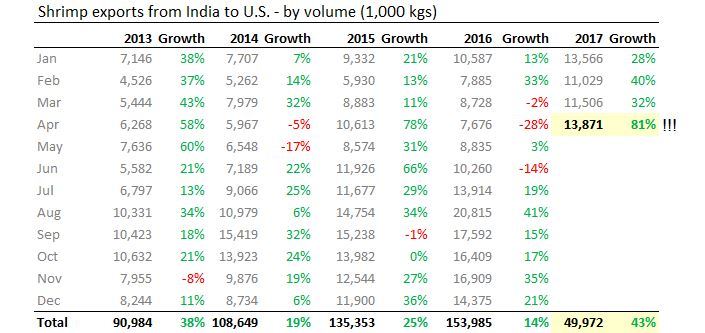

It is not good performance; it is record breaking performance !!!

81% growth over the same period last year. Highest % growth in last 52 months (partly because of low base effect).

Well done India. Go Avanti…

Source: https://www.st.nmfs.noaa.gov/apex/f?p=169:2:0::NO:::

18 Likes

Low soya prices could be one reason for the farmers anger in MP…The irony is the same reason could lead to happiness of another farmer - the shrimp farmer…The silver lining is that atleast another type of farmer is doing well for the same reason. Incidentally it will benefit companies such as Avanti feeds due to falling raw material prices and booming demand for its products due to record exports of shrimps in Apr and May FY18…

5 Likes