Thanks,There was another interview on ET Now.Any link of that?

Q2 results

Any reason of increased cost of raw material? Increased from 75% to 88.6% QoQ which seems to be one of the primary reason of net profit decline of ~16% QoQ. (Along with the minority interest of 3.4 Crs paid to TUF)

Ayush bhai wats your view on Avanti results. Top line growth is very good. Bottom line again subdued. Expenditure is increasing every quarter. Kindly guide

The question is do they have the pricing power to pass on the price increase or they are holding the line on price in order to increase their sales and market share?

Looks like the profit margins have halved. Let me hypothesize a theory to explain it, and we can see if evidence points towards it.

They sold a lot of shrimp feed, maybe like 60% more in volume. Shrimp prices crashed, and they ended up with 30% sales growth. If the cost of raw materials per unit volume also increased a bit, resulting in 30% de-growth in profits from the shrimp feed.

Facts: 30% sales growth and 30% profit de-growth of the feed division.

But I’m not able to find evidence for

- The shrimp price crash: (did not)

http://www.indexmundi.com/commodities/?commodity=shrimp

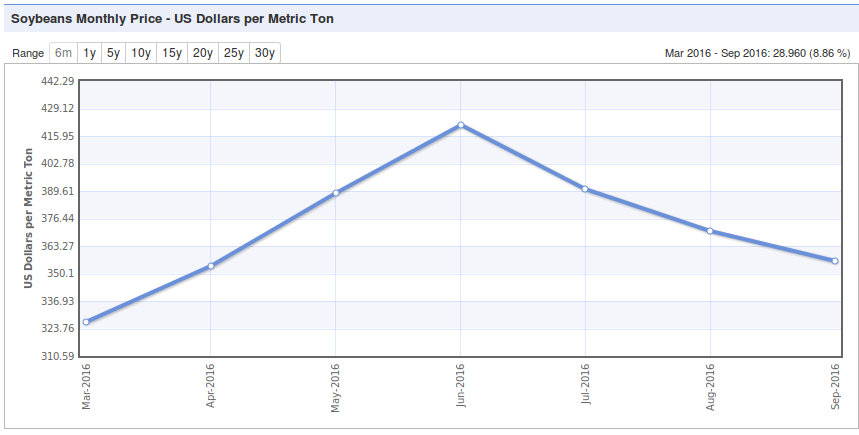

- Soybean price rise: (did not)

http://www.indexmundi.com/Commodities/?commodity=soybeans

So what really happened here?

1 Like

Please find below my analysis of Quarterly and Half yearly results. I could be completely wrong in my analysis.

What people seems to be ignoring is the increased margins in Shrimp processing. Although profitability wise impact is minimal (due to much lesser percentage from processing), going forward I think this might be deliberate strategy on part of the management. The competition has increased in feed business where 2 more players have come in and have tried to underprice the encumbered players. Bear in mind the industry itself is not growing at fast rate this year. Despite of being the biggest player, the company has shown very good topline growth. According to me next few quarters will be testing in terms of margins but good thing is that the company has achieved a good size with a very good balance sheet, so it has capacity to suffer which smaller players may not have.

My guess is Avanti (with the increased capacity) will be adapting the strategy of giving up some margin in feeds ( may be till irrational competition reduces) but getting a guaranteed supply for its processing division and ensuring higher utilization of the processing plant (where the capacity has also increased) .

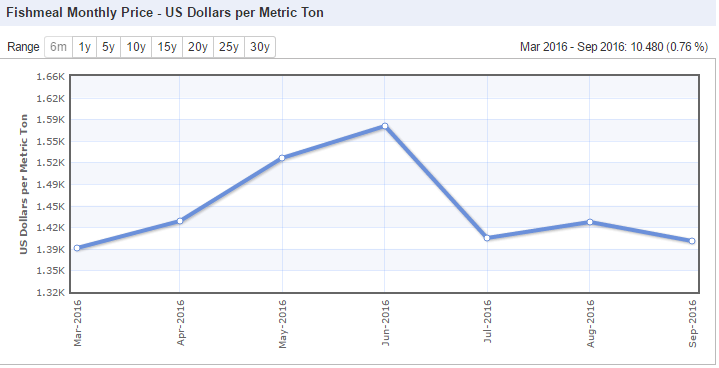

Apart from these there was significant jump in soya and fishmeal prices in Q1 which has been slowly coming down but still above last year levels. There might be some impact of that as well

Would be interesting to see Waterbase results this time around.

Disclosure: Forms more than 10% of my pf. No transactions in last 30 days.

3 Likes

@Gaurav_Agarwal Yes, not only the soya meal prices, the fish meal prices (bigger cost than soya) also rose for sometime

Fishmeal - Monthly Price - Commodity Prices - Price Charts, Data, and News - IndexMundi

At the time of AGM there was discussion about the rising inputs costs and declining margins in the feed segment to which the management acknowledged that though in past they have increased prices but this time they choose not to do the same. Probably the same has been done seeing the increased competition and to maintain and grow the market share.

In past also I remember couple of periods (20011 and 2013) they have had margin hit for couple of quarters.

Lets see how it evolves this time. The good thing is that the industry seems to be doing well and the company seems to be gaining traction in processing segment. Another very good thing is the super efficient balance sheet of the company…the feed business throws out cash. While peers are having high working capital requirements.

Regards,

Ayush

Disc: Invested

9 Likes

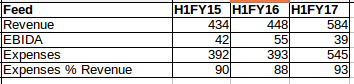

Taking cues from @ayushmit .

Please have a look at the prices of raw material for shrimp feed for h1fy15 and h1fy17.

It can be concluded that prices of raw material for h1fy17 is lower than h1fy15.

The table below shows the expenses as percentage of revenue has gone up in h1fy17 compared to h1fy15 in-spite of raw material price being lower in h1fy17.

Both the data does not fit in simultaneously.

6 Likes

The results are no longer there on BSE & NSE websites and also on Company website. Is it just me or something else going on?

It is very much there in NSE website eventhough it is missing in BSE. Just now I checked.

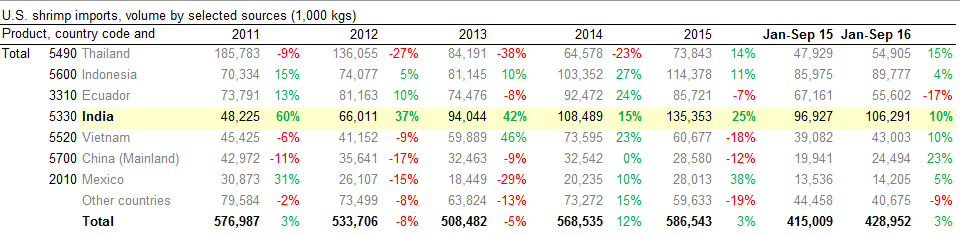

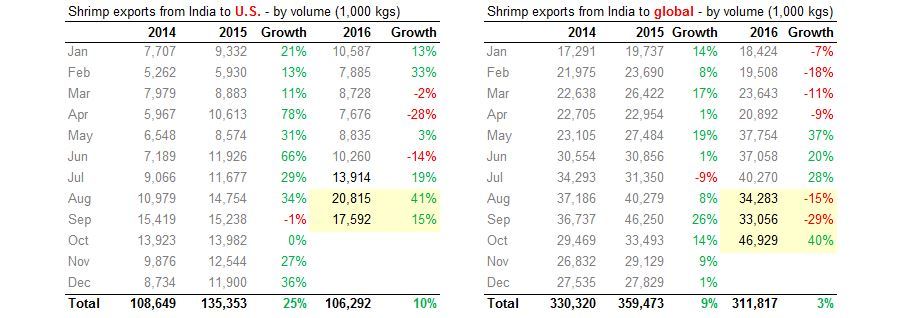

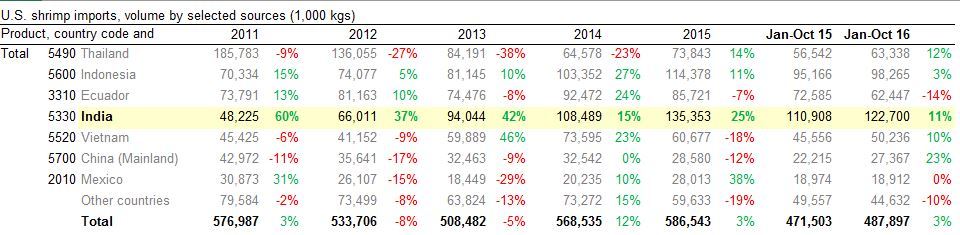

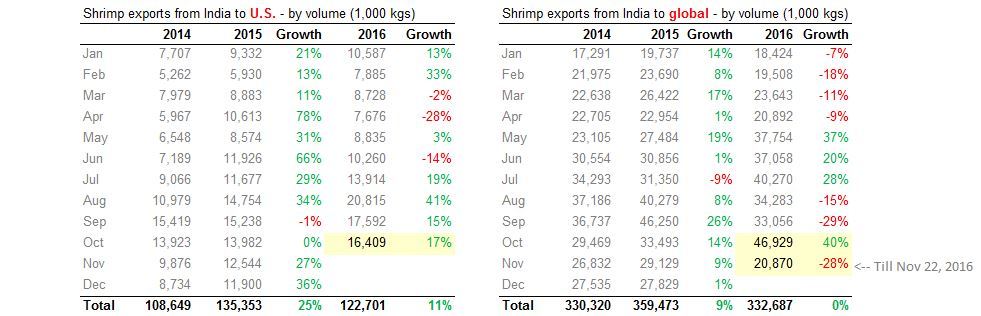

India shrimp exports (figures and analysis - by volume)

To U.S. (source: www.st.nmfs.noaa.gov/apex/f?p=169:2:0::NO96::: )

- India records good growth in Sep '16; 15% growth over the same period last year.

- India at top by increasing lead over Indonesia.

- US’s shrimp imports (from India & others) increased by 3%, compared to 2015 same period.

To Global (source: www.zauba.com)

- 19% growth in Oct YoY.

- Note that zauba data may not be completely accurate; just use to get the trend right.

10 Likes

Yesterday Waterbase Q2 came bad and they mentioned in the quaterly release letter,that results were bad because of Shrimp disease. Does anyone has idea on this ? You can check its letter to BSEAF4958DE_416B_45BB_9159_32141C82E345_192147.pdf (604.2 KB)

1 Like

@nil_71, thanks for highlighting. Disease outbreak is a high risk item. We track monthly shrimp export numbers for exactly the same reason i.e. to spot early indications of drop in export numbers (if any). Thankfully, for now, the data is giving no such indication. Let’s keep monitoring.

India shrimp exports (figures and analysis - by volume) - New data

Seems Indian shrimps demand is intact. Shrimp price is okish. Increase in the area of culture is giving 10-15% growth. However rise in raw material price and oversupply in shrimp feed market (capacity) is putting pressure on the bottom-line growth; this could continue for some time. Next season could be interesting for Avanti; to be driven by optimum utilization of shrimp processing plant and feed plants (new capacity).

Disc: Invested. Have trimmed my position in early Nov '16.

4 Likes

@lustkills, Thanks Sandeep Bhai for beautiful snapshot which is really worth more than thousand words.

Total Import to US from 2011 till 2015 is almost unchanged. India gained the most at the expense of Thailand and China and already has the Lions Share among the pool although India used to be in Lower order during 2011. What could enable Indian exporters in General and Avanti in Particular to continue the momentum on a much higher base?

Does any valuepickr has a handy note to help on the above question?

After the Q2FY17 results of Waterbase, its pretty interesting to see the competitive landscape. Avanti continues to maintain leadership

Despite having the highest market share in the industry, the growth rate is better than several other players + more importantly the balance sheet is better. The business is throwing out cash for Avanti and its operating on negative working capital. While Waterbase seems to be having a risky balance sheet to achieve higher growth.

Avanti is continuing to get greater advance from its dealer network which is not available to others.

Regards,

Ayush

18 Likes

I was just trying to identify the potential revenues from the Shrimp Processing business.

My thought process is as below:-

- Identify the peak potential revenues based on capacity.

- Use a realistic capacity utilization to understand realistic revenues.

- Use Thai Unions’s shrimp processing business Revenues to understand if the revenues we consider for the JV are reasonable.

Current shrimp processing capacity = 25 T per day

Plans to expand the same to 75 T per day or about 23000 T PA

Source: Thai Union Acquires Stake in India's Avanti Frozen Foods | The Fish Site

Last 5 year average realization per T of shrimp processed

Thus, if operated at 100% capacity - this facility can do 23,000 T X INR 679,443 per T or INR 15627 mln.

However, I understand that shrimp processing cannot operate throughout the year. So, conservatively, say it operates at 60% - then the potential revenues would be INR 15,627 mln X 60% = INR 9,376 mln.

(If 60% is too high or too low, I do not know)

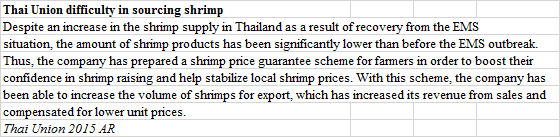

Now, from Thai Union’s Annual Report for 2015, we get certain indications of it facing issues in sourcing of shrimp. Look at the following comments:

Thai Union 2015 AR

Thai Union might have plans to diversify its sourcing base from within Thailand to from more towards India.

Look at some of the comments in the article above:

“Avanti Feeds is our reliable long term partner in India. I found this relationship very important and has been very fruitful so far. The firm’s strong management team has been consistently delivering great results in recent years, making us a very happy and proud investor of the company. With India becoming an important shrimp processing base for export markets and potentially a major market for seafood in the future, we just cannot miss it. It will hopefully serve as our springboard for even more strategic investments there, should other interesting opportunities arise,” said Thiraphong Chansiri, President

and CEO, Thai Union Group

“We aim to expand our shrimp processing network into India in order to diversify our sourcing and operational risks. Also, added production capacity will help accommodate growing demand for our shrimp products globally. Avanti Frozen Foods’ capacity should compensate our current raw material shortfall in Thailand. India’s shrimp farming sector has not been affected by serious disease outbreaks, such as Early Mortality Syndrome (EMS), like Thailand, China and Vietnam. I am very positive about this new investment. We believe the mutually beneficial partnership with Avanti Feeds will make us a strong player in the promising seafood sector in India,” commented Rittirong Boonmechote, President Global Shrimp Business Unit, Thai Union Group.

“Due to its existing profitable operations and customer base, the firm will be immediately profitable in its first year. Currently, the existing factory has a workforce of 750. The new plant, once completed

and up and running, will add this figure up to 2,250.”

The above comments suggest that there some crystallized plan by Thai Union to source shrimp from India.

Now this INR 9,376 mln that we have arrived at - let us understand how big or small is it from the context of Thai Union:-

Thai Union might then use the JV to buy raw shrimp, process it and export it to the parent that might just package it and export further OR may be the JV could export directly from India to US/EU after packaging.

I am just thinking one needs to relate the potential revenues of the JV to the COGS of the shrimp division of Thai Union (it could be with sales of Thai Union as well but let us take COGS conservatively):

Shrimp sales of Thai Union in 2015 (Dec) is 36.2 b Baht which translates to INR 67,047 mln.

Shrimp division COGS (using consolidated COGS/Revenues ratio) would be 30.6 b Baht which translates to INR 56,625 mln.

Thus, the potential revenues of the JV (INR 9,376 mln) translate into a 16.6% of the Total requirement of shrimp by Thai Union.

It seems reasonable that Thai Union would want to shift sourcing base equivalent to 15% of total requirement from Thailand to India.

However, it is interesting that Thai Union is using Avanti for the same and not doing it alone. Because, Thai Union gets only 40% of profits of the JV, we will need to be watchful of transfer pricing going forward.

Also, Avanti gets only 60% of those revenues effectively (from a profitability perspective) which is about INR 5,625 mln. So, could Avanti get an effective sales of INR 5,625 mln at the revenue from - say in Mar’18 when the total shrimp processing capacity of 75T should be fully operational (versus INR 2,861 mln of shrimp sales in FY2016).

Another question I had was on the Feed capacity. In the 2016AR, the Company states the feed capacity will increase by 125,000 and by 40% in the coming year (that is FY2017). Doesn’t it imply that current capacity pre-expansion was 312500 T and will go up to 437500 T now? AGain, they said this shall lead to revenue growth of INR 500 crs and profit growth of 5-7% - just wondering whether they were implying a margin drop as profit growth is far lower than revenues.

Let me know if you disagree with the broad thesis above as my understanding would be much lower than many of you on the group. Thanks.

10 Likes

Hi Rohan,

Excellent work done. My analysis/ projections for next few years also points to be similar numbers. Regarding margins, according to me last year was one off and seeing this years numbers close to 10% is more sustainable till value added processing comes into play. For me following are the key things to watch out for next 2-3 years :-

-

There is not much product differentiation between the players so I think the differentiating factor is company’s distribution network and staying with the farmers through the whole cycle. Can other companies replicate this strategy or offer a good enough product at lower price and take away this advantage?

-

Does the irrational competition subsides or not? This for the first year after many years when there was no price increase due to 2 more processing players entering into feed.

-

Processing scales up as expected. There are some well eastblished incumbernt players so it wont be that easy. The relation build over last few years with farmers should help. TUF JV should provide the necessary support.

-

Given the company has done major capex last and this year. Going forward, I expect the dividend payout ratio to rise substantially to 50% and above (TUF has also done the same). I would be equally happy to see this getting postponed because of need of capacity expansion of the processing facility. Food for thought - Accelya Kale (yes a completely different industry with lower risks) over last 5 years has sales growth of 10% CAGR, Profit growth is 16% CAGR while Market cap CAGR is close to 60% as dividend payout had increased from under 20% levels to above 80% levels.

-

Lastly the industry risks like disease,cyclone are also key things to track as well. Also globally, we need to keep track India’s exports vis-a vis other countries. The good thing is we get monthly data for US and we can see data for other geographies from Zauba (which might not be 100% accurate but help us see the trend) . We also get weekly global data from undercurrent news and siamcanadian. But in my opinion, even if the India’s exports to US slows down there is ever increasing Chinese demand to fill the gap as well as the market share gain in processing (which is close to 1% for Avanti vs 40%+ market share in feed) should provide 15%-20% sales growth for Avanti over next 2-3 years

Latest Oct US sales from India up 15% https://www.undercurrentnews.com/2016/12/07/indias-shrimp-exports-to-us-continue-to-tick-up/

Disclaimer There is a valid concern of too many moving parts and variables to track in this industry because of which almost all fund managers stay away. Do your your analysis. Invested so I am biased

5 Likes

Sharing this video which says Vietnamese shrimp export companies adding some substances which make shrimps bigger in size.

Not sure though, how much it would impact other players since anything which US imports would have undergone some inspection. But if its true can we say Avanti could gain anything from this, assuming they are not following this kind of practice.

1 Like