As we all are aware Astral is last few years is quite aggressive towards creating brand for itself.

| Year |

Revenue |

Advertisement & Promotion |

|

| 2022-23 |

5158 |

153 |

3% |

| 2021-22 |

4394 |

125 |

3% |

| 2020-21 |

3176 |

106 |

3% |

| 2019-20 |

2578 |

91 |

4% |

| 2018-19 |

2507 |

87 |

3% |

| 2017-18 |

2073 |

68 |

3% |

I understand some of these may be non recurring in nature and shall result in higher EBITDA margin. Management in call saying 17% to 18% margin is sustainable.

1 Like

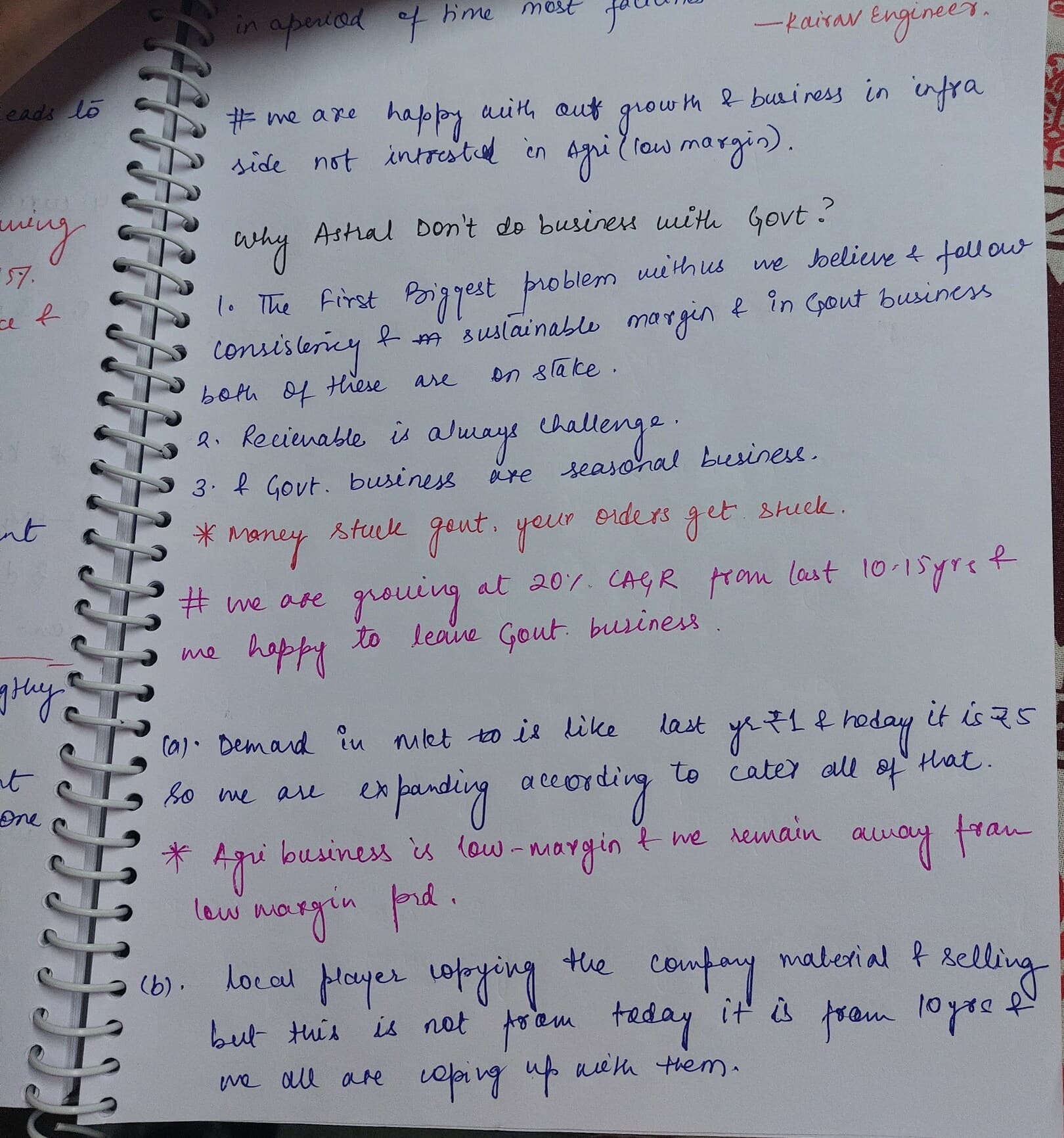

Why astral not deal with government for business? from their recent con call

3 Likes

Hi all,

While reviewing the old concall of astral found that - Management can be transparent and along with that hard working.

3 Likes

Market size and market share: Segment-wise market size and company’s share is as follows Pipes – Rs.

37000 crore/9.6%, Adhesives – Rs. 18,000 crore/4.7%, Adhesives UK – Rs. 14000 crore/2.4%, Paints – Rs.

58,000 crore/0.4% and new businesses – Rs. 25000 crore/0.8%.

The above is from the report of sharekhan in March 2022. (https://www.sharekhan.com/MediaGalary/StockIdea/Astral-3R-May18_2023.pdf)

Below is the 2Q2023 (2QFY2023-2024) concall:

Now to summarize all the four verticals, we are very happy with the performance and we

are confident that this growth momentum will continue and we will keep working hard to

gain the market share and last but not least that our core vertical that is pipe, you can see

that in spite of higher base, we are still gaining the market share and with brand getting

more and more stronger will gain more and more market share in the coming time because

we are adding a lot of new geographies in terms of manufacturing facility, which will help

us to grow market share and reduce our trade cost.

@hitesh2710 Sir, May I request you to please let us know how much market share Astral has in above verticals as on date

4 Likes

Astral Limited Q3 FY-24 Earnings Conference Call January 30, 2024

Plumbing Business:

-

In Q3, the demand scenario is very robust, and we can deliver 15% volume growth in Q3 and 24% volume growth in the first nine months of FY24 in the plumbing business

-

In the plumbing business we can deliver an EBITDA margin of 16% in Q3 and 17% on a nine-month basis against our guidance of 15% to 17% EBITDA margin.

Pipe Business:

- As communicated in the last concall due to robust demand in pipe verticals Company has decided to aggressively move into expanding its capacity. As communicated earlier we are putting in three new plants, and all are going as per schedule

Guwahati Plant:

- A 22,000 metric tonne plant already started production on the water tank last quarter, and from January, we have already rolled out our pipes, so we are expecting some sales in the last quarter from this plant

Hyderabad & Kanpur Plants:

-

A 70,000 metric tonne and Kanpur plant 60,000 metric tonne, expansion activities are going on in these two locations in full swing. Hyderabad first phase of construction is almost over by March and in Q1 we will be starting to put machines and by Q2 end commercial production will start. The Kanpur plant layout is in progress and shortly the construction work will be started.

-

During the first nine months we have increased the capacity from 2.9 lakh metric tonnes to 3.29

lakh metric tonnes, 30,000 metric tonnes increase in the capacity.

Adhesive and Sealant:

-

Our state-of-the-art plant at Dahej is in operation and giving good results in terms of energy saving, and cost reductions what we originally planned and what we have reflected in numbers is going to be exactly seen in the coming quarters after one or two quarters as the plant gets fully functional at the scale and the inventories of different plants which has already been there and made at the older locations are sold in the market

-

Our Indian adhesive operation has given excellent growth in Q3, with top-line growth of 17%, and on a nine-month basis 15% in value terms. In volume terms, it is much higher due to the fall in chemical prices. Even EBITDA for the quarter was very healthy at 16.5% in Q3 and on a nine-month basis it was 16%.

-

Our UK adhesive top line has grown by 9% in value terms, and in volume terms, it is growing much faster, but in EBITDA terms it has given a negative 3% EBITDA in the last quarter mainly due to inventory loss and heavy FOREX loss due to the fluctuation of GBP and US dollars

Paint Business:

-

In the paint business we are getting ourselves ready with lots of new products at the plant and various systems and MIS in the back office at the same time we are creating a team to launch the Astral brand in a few states from Q1. So, in Q1 we are coming out with our launch of Astral brand products, and we will be addressing a few markets, at Phase-1 of it and slowly and steadily increasing the reach to different markets and almost completing our reach to the entire country in coming one to two years with the new brands, new products and new complete range of product line.

-

Due to this we are confident that in Q1 next year we will see a substantial improvement in the numbers and presence of brand Astral in the market. We are in the last leg of production which will be done in the Q4 post and we are foreseeing a continuous journey of growth, and the paint business has always been in a positive EBITDA number and whatever the sales have been happening and happened is always in a positive EBITDA number

Bathware:

- Compared to last quarter’s sales of Rs. 17 crores this quarter the Q3 sale was (+20) crores, which is very healthy and continuously improving. Since this is a new segment for us, we don’t want to rush and we want to grow slowly, steadily with steady and consistent growth

4 Likes