Anyone attended todays analyst/investor meet ?..Please do update on that

From their investor presentation.

•Pressure on booking with continued sluggishness in the market. 1.65 lsf in Q1FY16

vs 3.52 lsf in Q4FY15 vs 4.51 lsf in Q1FY15.

On concall today AHFL management informed that its highly unlikely that they will be able to meet the guidance of selling 1800-2000 units. Given weak market conditions, they have not given any guidance/timeline for recovery

I joined the conference call today and posted a couple of questions to Varun.

1->Management feels this is the worst slowdown they have experienced, accentuated by the fact that they are a bigger company now so feeling more pain.

2->In terms of their intervention to accelerate bookings, they don’t feel discounts will help. They are more relying on increasing “Happiness Quotient” for existing customers so that they can get increased sales through referrals. Already about 90% of bookings is happening through referrals.

3-> Impression I got was that the fact that their projects are currently largely based around Industrial townships (which contributed to their good performance with low land cost, etc.) is pinching them now with slowdown which is more acutely felt in such areas currently. As long as the slowdown persists, they will be launching more and more projects in big cities like Kolkata and Chennai where customer profile is more robust and income streams more differentiated. Having said that, they would be taking on the bigger boys and not sure how their current business model will hold up in these big cities. I am optimistic though considering their execution track record.

2 Likes

Co was rep by Varun Gupta, Whole Time Director.Key takeaways of call by Capital Mkt

Booking in Q1FY16 stood lower by 53% at 1.65 lakh square feet (lsf) compared to 4.51 lsf in Q1FY15 . Booking in Q4FY15 stood at 3.52 lsf. Sharp decline in area booking compared to previous quarter due to sluggish market condition. Decline in booking for the company is lower than the industry. The company expects sluggishness to continue.Unsold inventory in completed projects as end of June 2015 was 94539 sft.Deliveries or area handed over in Q1FY16 increased to 2.36 lsf compared to 0.07 lsf in Q1 FY15 due to higher area being handed over in partnerships (2.34 lsf in Rangoli Garden).Area constructed in Q1FY16 stood higher at 5.33 lsf compared to 5.16 lsf in Q1FY15. But that was lower by 16% compared to 6.31 lsf in Q4FY15. Area constructed though declined on sequential basis, the company is generally on track for execution and achieving the construction target. Construction will lead to achievement of overall delivery schedule.As the company follows the project completion method of accounting, the profits varies with project completion. FY16 will see improvement in profit recognition as the company expects more deliveries in Ashiana Town Beta, Rangoli Gardens, Ashiana Anantara, Ashiana Navrang, Ashiana Utsav (Lavasa) and Gulmohar Gardens.Entered into a JDA with Bengal Shriram for development of senior living/regular housing project on land measuring 19.72 acres. Entire project to have a saleable area of 18 lakhs square feet (approx) . Submit plan for approvals in 6 months.

Lavasa - Change of guard has caused delay in issuing occupancy certificate.The company looks at delivery of 1800 units this fiscal.Market behavior is not on expected lines. For FY16 area booking of 2.2 msf (up from 1.812 msf in FY15) is incredible difficult.Lavasa phase I, Gulmahor phase I, anatara one tower will get completed.

Chennai project is on late stage of approval and expect the launch will happen in next 2-3 months. Kolkata project will get launched in next fiscal.Enquiries dip by 25%, there is also delay in conversion of site visits to bookings as well as the customers are deferring their decisions even though affordability is not an issue.Market has to improve for the booking numbers to turn robust. However the company expects the foray into Chennai market with launch of a new project and another new project in Bhiwadi during this fiscal will bring in additional volumes in case of new bookings.FY16 will be challenging in terms of Cash flows. However, given the receivable from total booked units, we do not see execution (area to be constructed) challenges.

5 Likes

splendidly explained!

what do you mean my accounting policy change? can you please be little more specific?

Brahmal Vasudevan’s Idria and Goldman Sachs also invested in Ashiana Housing via a QIP of Rs. 200 crore at Rs. 215 per share.

all prudent portfolio managers too are bullish about it

Yesterday was the AGM. Did anyone attend? Any updates?.

Indianivesh has comeout with the update after Q1 results. Can be found here.

Use the highlighted region to get the pdf.

Hi Milind, AGM was attended by me.

AGM was presided by Vishal Gupta.

He was really concerned about the current real estate situation. They are working in 6 cities now, out of which they are really strong in 3 cities. The remaining 3 they will strengthen depending upon the response of their initial project. The internal relation between the brothers is really very strong. QIP money will be utilised as and when they find the opportunities. He refused to give any growth guidance.

2 Likes

This thread seems to have gone very quiet after the dismal performance of the stock price in the past few months !

Q3 & Q4 FY 16 - company should be recognizing more than healthy revenues.

Broker consensus - FY 16 rev figure in the vicinity of 600 crs. & PAT of around 200 crs. Current mkt cap around 1435 Crs. FY 16E PE ~ 7x.

Given the current gloomy state of affairs in real estate sector - has ashiana been battered enough? Is value starting to emerge for a 3-5 yrs holding period?

Views invited…

Disc. Invested & adding…

2 Likes

Realty sector is in a bad phase right now. No doubt about it. Sales have really dried up.

However that is an opportunity to cherry pick in this sector and Ashiana for me stands out. This is not a company I would trace every quarter. I believe in the management of this company which has created shareholder value in the past and will continue to do so given their high focus on ROA and conservative financing. For me, this management is an iconoclast and I would want to back them up knowing that my money is in safe hands.

Disc: Invested.

1 Like

Most corporates houses have not done well in 2015 and there has hardly been any growth. I believe 2016 is going to be no different and hence the real estate sector will continue to face challenging times. Ashiana Housing last 2 quarters have been dismal and the stock was trading at a much higher price than what it deserves. Even at the current price, I believe the company is expensive and it might touch 100-110 if the global market continues to remain uncertain which I believe it might.

Though I like the management, I believe the entry point of the stock plays as much as a role in investment return and hence I feel the stock is expensive even at current levels. I might consider averaging only once it shows better results.

Hi

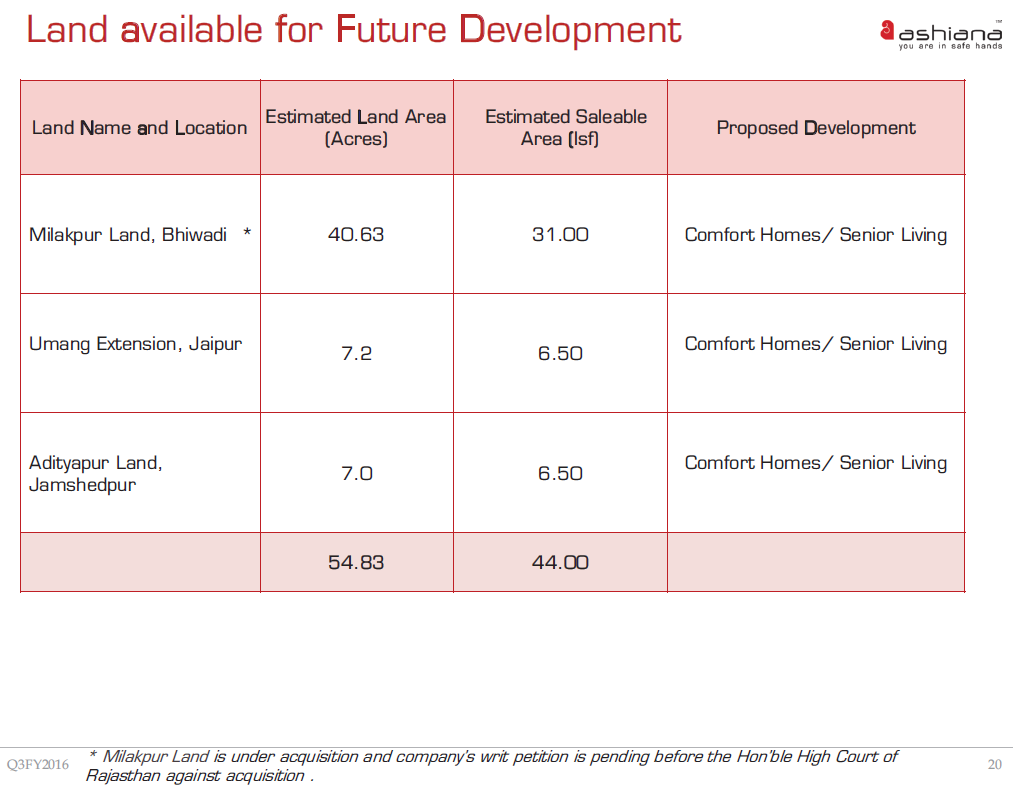

Some body help on the below Estimated Saleable Area (Lsf):

From Q3_Investor Presentation page 20:

Estimated Land Area = 54.83 Acres = 54.83 x 4840 Sq.Yards = 54.83 x 4840 x 9 Sq.Feet = 23.88 Lakh Sq.Feet.

But in the presentation they are saying 44.00 Lsf.(Lakhs Square feet)

Am i missing some thing here or their calculation is wrong ???

Regards

i think u need to consider that these will be towers. so effective sale-able area per acre of land will get a multiple.

1 Like

oh…ok…I got it now thank q…

The information here is FSI is 2. Typically low rise apartments. Price in tier 2 low rise apartmenrs should tie with reported asp

I hope that the new Real Estate bill is going to change the fortune of some of these infra and Real estate guys.

Its an official sector now, soon may be a part of infra core too

Results are out. EPS has gone up from 4.93 to 12.66. At an industry avg PE of 25 stock looks quite attractive.

Invested: sitting on a big loss

1 Like

Thanks for sharing. I can dream of the profits tonight. However, volatility in quarterly/ annual earnings gives me nightmares! How do we anticipate/ predict/ extrapolate future earnings? We can not. PE has to be low to cover the volatility in earnings. Conservative 15 - max 20. Must keep some marking of safety.

Disclosure- Invested at a significantly higher price than current. Hope to cover losses now!

2 Likes