Hi, Is there a link to the report that you can please share?

From Q3 results -

Volume growth of 15% as per their press release

Revenue at 100 Cr from 87 Cr

Gross Margins show a spike to 31% from 28%, guess this will be for all PVC players for Q3

Other expenses to Sales shows a spike to 13.5% from 11% which is due to integration of the Kisan Pipes plant which is not yet running at optimal utilization

EBITDA and PAT margins should trend higher as they sweat their assets more, by the looks of it the higher gross margin might be a one off

Seeing YoY PAT anyway is misleading due to the tax rate change. At CMP stock appears to be pricing in a 13-15% growth rate, if the story can get back to growing at 20% it might look interesting and get the market more excited.

4 Likes

Promoters have allowed the warrants to lapse by not acquiring within 18 months. Is it something legal which can be done?..promoters would have not allowed warrants to lapse if current share price is higher? 26eac3dd-6640-4cd0-aff7-2add4bec8dea.pdf (391.3 KB)

Discl: presently holding tracking quantity.

That would typically mean that the 25% up front payment promoters should have made at time of warrants issuance will now be forfeited by promoters and retained by the company.

1 Like

Yes. Promoters were supposed to subscribe these warrants at 590 rs. Now stocks is available below 250 rs. This lockdown will impact company growth and high valuation. Promotor might be waiting for low prices to add.

Results are out link here - Presentation:

The reason they have not converted the warrants are on slide 31:

- The Company had allotted 2,485,000 fully convertible warrants, in addition to 950,000 equity shares, on preferential basis to Promoters and promoter group in October 2018 at a price of ₹590 per share, which were to be converted into equity within 18 months from the date of allotment

• The promoters during this 18-month period exercised 1,125,000 equity shares. Post conversion of these warrants, the promoter shareholding of the Company increased to 47.11%

• However, given the current macro-environment, the promoters believe it is prudent to not undertake any

further investments owing to the following reasons:

> The Company currently holds a strong cash balance and is more than adequately funded for existing growth plans

> Given the unprecedented situation, focus now primarily is on improving its utilization levels at the existing and new capacities scheduled to be commissioned in the coming fiscal

> To avoid further equity dilution without commensurate growth opportunities in the current environment.

• Accordingly, the promoter group has decided to not exercise their right to convert the remaining warrants into equity shares and 1,360,000 warrants allotted in their favour now stand lapsed

• Overall, the promoter group remains committed towards the business operations and are confident in its

growth outlook

2 Likes

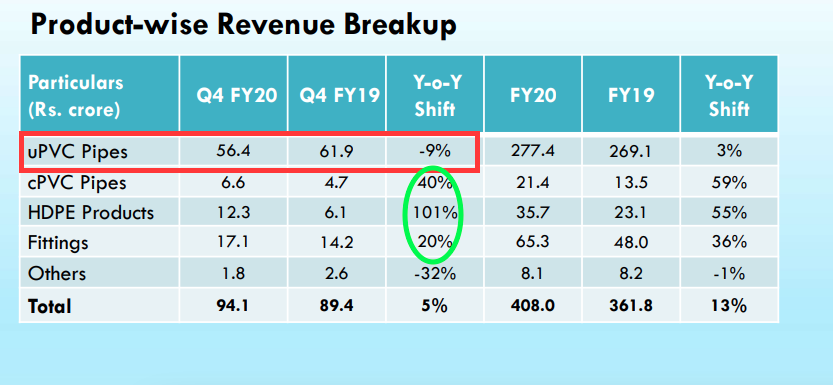

Q4 results update: ( q4’20 vs q4’19 - comparison)

- increase in revenue of 5% from 89.4 to 94.1 crores (with the fact that the half the month of march was lost due to covid related shutdown)

- EBITDA margins are pretty much stable (marginally down by 70bps) ~ 11%

- Profit before Tax also was stable at 7.5 crs

- Net cash of 128 Crores.

Note:Volumes for the quarter, especially in the month of March were impacted due to the plant closures and suspension of logistics activities caused by the COVID-19 outbreak - 9721 MTPA

-

9% revenue drop in uPVC pipes, which forms close to 66% of their revenue, compensated by increase in other segments growth.

FY 20 Update: -

13% year on year growth in revenue from 361.8 to 408 crores.

-

EBITDA margins are pretty much stable (marginally down by 70bps) ~ 11%

-

Profit before Tax increased by 11% to 37.7 cr from 35.6 crores

-

for the full financial year - 3 segments cPVC, HDPE and Fittings have shown good growth year on year, but again uPVC the main contributor has marginally increased by 3%. to be monitored…

-

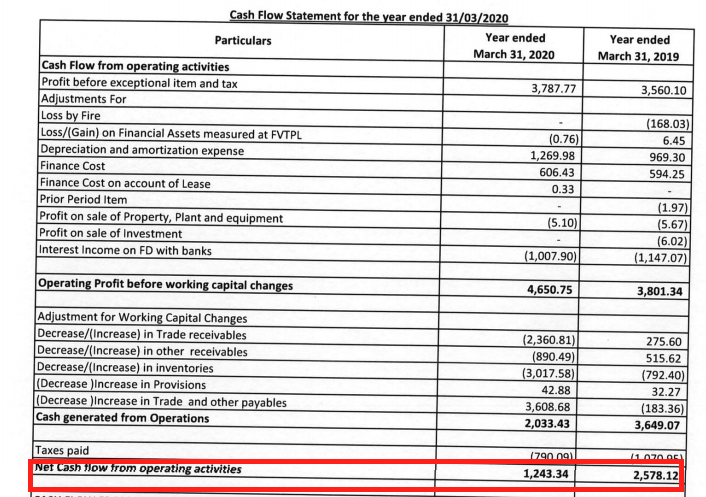

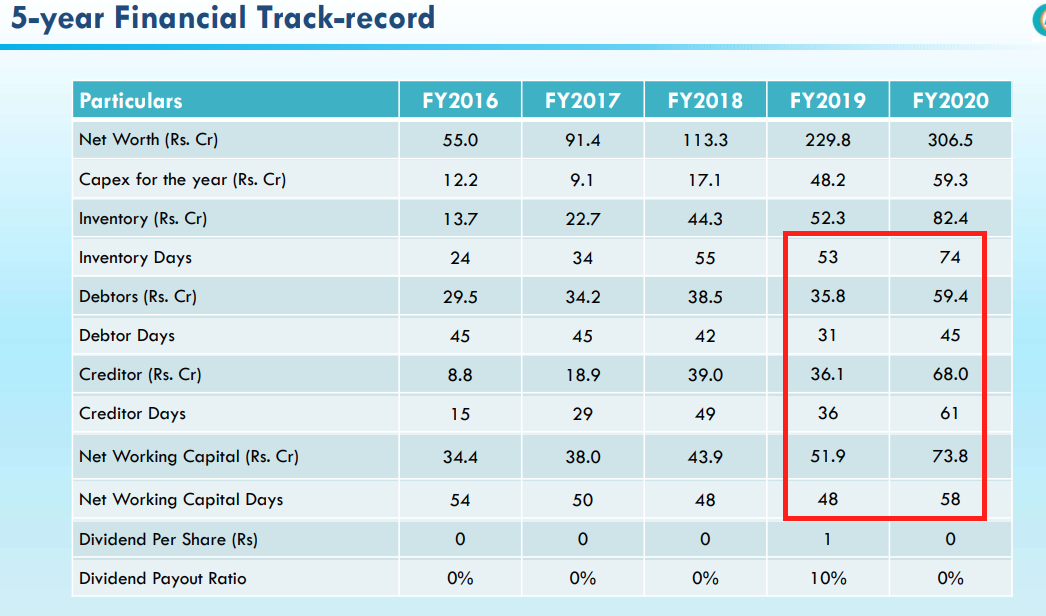

Increase in debtor days( although worrisome back to old 45 days mean reversion), WC days and inventory days - which needs to be monitored. This shows a lot of cash has been stuck in inventories and debts to be collected.

- Layer this with the CFO v/s PAT for the year: 12.43 crores in FY20 v/s 28.5 crores in FY 20

- Layer this with the CFO v/s PAT for the year: 12.43 crores in FY20 v/s 28.5 crores in FY 20

-

In FY20, volumes stood at 44,692 MTPA an increase by 12%

1 Like

Acquisition of 125,000 equity shares worth Rs 387.79 lacs by promoter & director

1)Well the promotors only subscribed to 45% of warrents. They are now telling that they have sufficient cash balance, then why did they issue so many excess warrants(55%) in the first place?

2)How come now they are thinking about equity dilution? When it was already clear at the time of issue of warrents that x number of equity will be diluted.

So its simple promotors do not want to buy because the market price is low, they issued warrants expecting to increase their holding at cheaper cost vis a vis buying directly from market.

4 Likes

APL Apollo promoter Sanjay Gupta and APL Infra banned by SEBI from dealing in securities for 2 years… anyone following this? Neither are direct shareholders in Apollo Pipes. Company says no material impact

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1b5d3cef-8307-4797-b198-e65c3beee441.pdf

Here is the SEBI order:1592919878978.pdf (929.3 KB)

2 Likes

anyone attended AGM, any takeway ?

Apollo Pipe gave good Q2FY21 results. Consistency of these numbers will be the key going forward. Every year company reports one exception quarter. Volume growth was good at 19% for the quarter due to pent up demand, for full half the volume growth was muted.

- Sales growth of 28% yoy. Pat growth of 63% yoy.

- Doubling capacity of Water Storage Tanks at Sikandrabad facility by November 2020.

- On the whole, the Company is aiming towards a healthy capacity upgradation and is on-track to achieve a total production capacity exceeding 100,000 MTPA by March 2021. Current capacity is at 84000 MTPA.

- Raipur facility with 7200 mtpa will be operational by March 2021.

Regards

Harshit Goel

4 Likes

Q3 FY21 concall notes

DATE:18.01.2021

PVC PRICE IMPACT ON VOLUMES?

-Prices are almost at peak. There will not be much volume impact as there is no alternatives. But due to high prices there is some deferment of demand.

-PVC imports - 50-60% of domestic demand is catered through imports.

-With prices at all time high we are very cautious so that we may not have to face any inventory loss going forward. Working on minimum level of inventory.

FIDELITY INVESTMENTS

Impact on volumes ?

There is some pressure on demand due to high prices as dealers & retailers are making need based purchases.

Inventory levels at dealers & distributors are going down so there might be filing up of inventory in current quarter. Therefore demand will sustain.

-Volume growth of 7% is inline with industry growth.

- In Q3 there was 30-40% price hike in PVC prices as compared to Q2.

- EBITDA levels are currently high due to inventory gain but on a normalize basis expect to maintain 12-13% of EBITDA MARGINS

Geographical Distribution

TUMKUR plant contributes 10-15% of revenue

From DADRI plant we are also supplying to all the parts of country , so there is an element of stock transfers.

On overall basis South Contributes 10-15% of revenue & we expect it to go up to 20-30%

-Working on reducing delivery time to dealers from 10-12 days to 48 hours which will help us going forward.

FITTINGS contribute 20-25% of Revenue

Raw Materials- Have started sources from domestic sources like Reliance. Currently it is about 10-20% which will go up to 20-30%

Capacity utilization – Currently at 50-55%. At peak levels it can go upto 70-80%

PVC price sustainability – Prices will remain at same levels at next 1-2qtrs & there might not be any major correction unless supply situation normalizes.

-Optimistic regarding demand from agriculture sector as in Q1 demand will again come up due to seasonality.

- Fittings growth was around 30-32%.

CAPACITY EXPANSION

Adding Capacity across all locations except AHEMDABAD .

CAPACITY WILL GO UPTO 1,25,000 MTPA including Raipur plant & we can do a turnover of around 1000crs.

ROCE & ROE’s are currently at lower levels but as & when we reach optimum utilization levels within next 2 years & achieve turnover of 1000crs. Roce will be between 25-30% & Roe will be +20%.

CAPEX GUIDANCE

CAPEX – this year capex was around 50crs & more than 70% has already been done

Going forward Capex will be limited to 20-25% of Annual Ebitda Levels & all the capex will be funded through internal accruals.

5 Likes

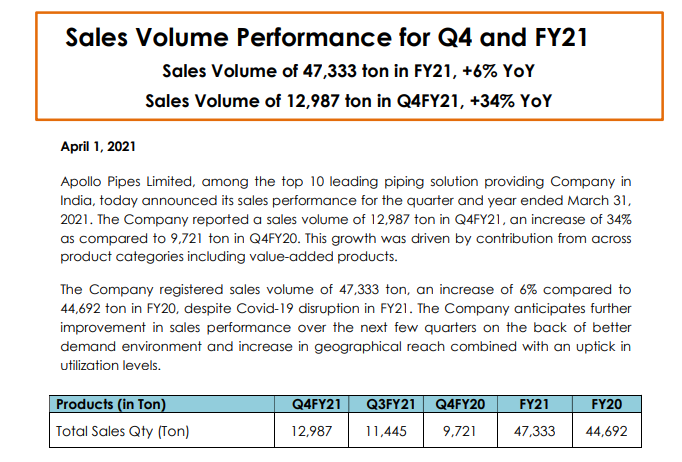

FY21 Sales Volume Performance

3 Likes

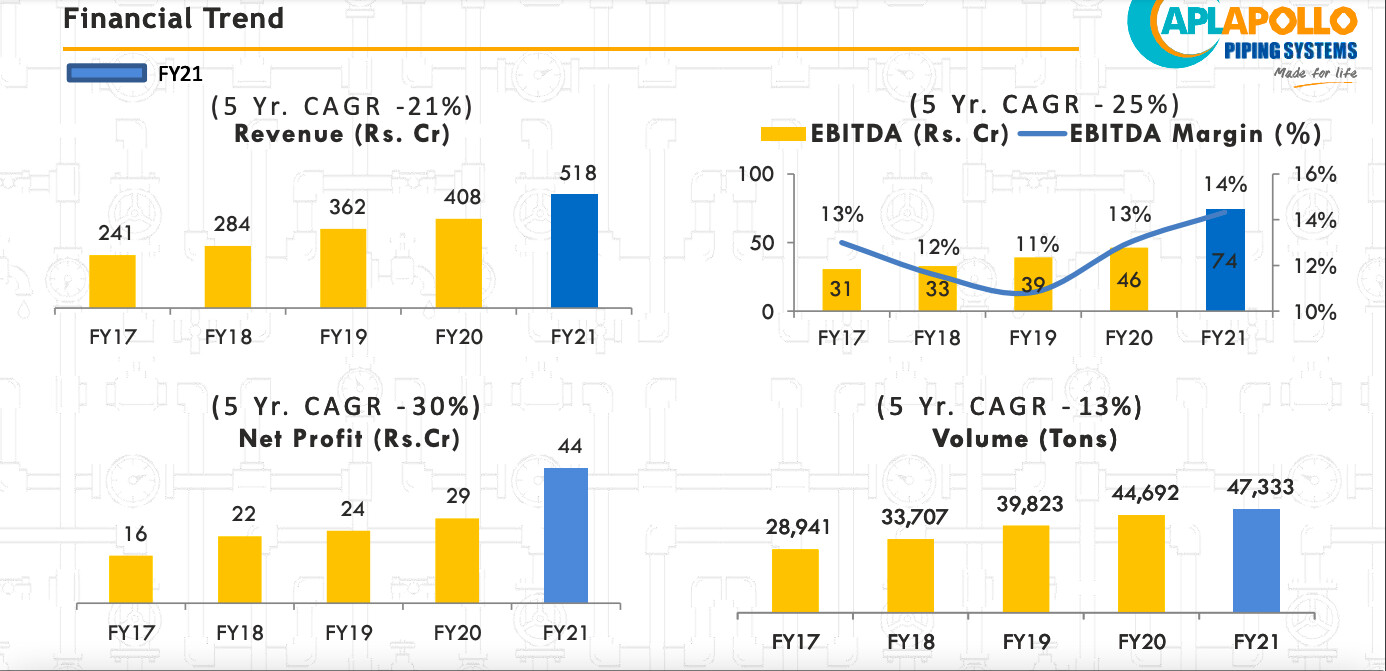

Q4 and FY21 results out:

Performance Review for Q4FY21 vs. Q4FY20

Sales Volume higher by 34% to 12,987 tons from 9,721 tons

Revenue higher by 85% to Rs. 174.2 crore compared to Rs.94.1 crore

EBITDA higher by 158% to Rs. 27 crore as compared to Rs. 10.5 crore

Net Profit after Tax up by 169% to Rs. 16.6 crore compared to Rs. 6.2 crore

Performance Review for FY21 vs. FY20

Sales Volume higher by 6% to 47,333 tons from 44,692 tons

Revenue higher 27% to Rs. 518.1 crore from Rs. 408 crore

EBITDA higher by 60% to Rs. 74.3 crore compared to Rs. 46.4 crore

Net Profit after Tax up by 56% to Rs. 44.5 crore compared to Rs. 28.5 crore

Interesting point to note in mgmt. commentary:

“Our latest range of Water Storage Tanks are seeing strong acceptance

in the domestic market and accordingly, we have already doubled the capacity for this product at our plant in Sikandarabad (Dadri) and also commissioned 1 unit at Tumkur. So, on the whole, the planned capacity additions should enable us to deliver improved sales momentum, going forward”

2 Likes

Given that the market has ignored this, not a major concern. The details of the case also indicate this was a legacy issue and not a recent one, has nothing to do with business operations of any of the group companies.

In almost every company there are transgressions, pick up any of the blue chip names today and one can dig up some dirt on the promoter/management at some point of time over the past 10 years. What to ignore and what to focus on is where the trick is in India.

A rule that works well is that promoters rarely knowingly transgress when the business is doing well and value is being created. It doesn’t make sense for someone to cross the lines for 2 Cr when the stock price (and hence net worth of the promoter) is compounding at 15% per year.

That said, doing due diligence on every single business one holds should be part of the process. No exceptions here.

Disclosure: Invested for self and customers, no transactions in the past 30 days

2 Likes

So I was going through the thread from the beginning.

I don’t know whether management has said the above lines “Targetting 1000 cr sales” as mentioned by @ravijain88.

Also I can see from the Financial highlights, the company has 200 cr sales then. (Aug-2016 when this thread was created)

Now 5 years is over and even if I discount the covid year fully, now we are exactly after 4 years, but if we see the sales of the company its just 518 crores which 50% lesser than the management target.

Despite the fact the company is growing at 21% CAGR, but the management has over promised in my opinion.

Even if see the above concall notes posted on Jan-2021, the management said the same.

I have a huge belief and trust on APL Apollo group promoters and I invested on other APL Apollo group like Apollo Tricoat/APL Apollo and they are exceptionally doing well there.

Even here in Apollo pipe they are doing a great job but… ![]()

I doubt whether they can able to achieve the 1000 cr sales by the End of next year, given the fact this industry is extremely competitive and lesser margins.

From 500 to 1000 in 2 yrs which means a whopping 40% CAGR(approx) is needed.

Screenshot from Q4 and FY21

I couldn’t find proper data prior to 2017 even in screener.in

Eagerly waiting to see the management execution in the upcoming quarters whether they are over promising again and again or they walk the talk.

VP members are free to add, If I miss or unaware of any info.

Disc : Invested and adding continuously in the recent correction.

2 Likes