Notes from Arihant Concall April ‘24

Sector going through difficult times. Company not hoping for much growth this year however is taking steps (incorporating wholly owned US subsidiary to onboard clients directly) and hoping for the business cycle to eventually turn (Ecuador competitiveness decreases due to duty and awaits EU approval for its facility).

-

One thing I would like to understand is that most companies explain that Ecuador is not a threat as its mainly into commodity and Indian companies into value added shrimp. If this is the case then why is Ecuador a threat to Indian Shrimp processors?

-

As the primary producers in Ecuador are highly consolidated (noted that there are 20-30 large corporates into aquaculture) and enjoy economies of scale the basic price is always going to be more for Indian Processor due to fragmented farming sector. This is a worrying sign which the management also agree. The only plausible explanation the management gave is that their farming area is limited being a much smaller country.

Insider Trading Penalty by SEBI:

While imposing a penalty of Rs32 lakh, market regulator SEBI directed Apex Frozen Foods Ltd (AFF)’s promoter, chairman, and managing director (CMD) Satyanarayana Murthy Karuturi, his wife and promoter Padmavathi and their son in law Ravi Kanth Sankuratri to disgorge Rs91.06 lakh earned illegally while in possession of unpublished price-sensitive information (UPSI). Does Market dicsounted the said matter…?

Any views on fresh investment by MIT?

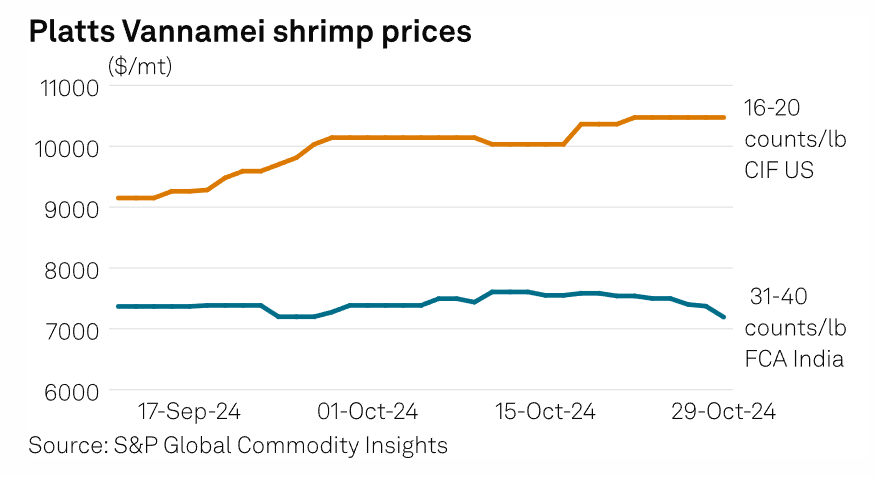

There has been a rise in global shrimp prices from Q1 this year (one can go to Google and search global Shrimp prices and open the trading view link to see it, I’m attaching a snapshot of the same)

As it can be seen from Q1 end till October the price rise is more than 10% well that’s huge. This price rise is not reflected in Q2 result of Apex frozen food which is into shrimp processing (Frozen Shrimp and Ready To eat shrimp). So I’m assuming this price rise might be seen in Q3 result (to be confirmed from Apex Frozen Foods mgmt in their concall)

Yes, In call management mentioned that from Q3 onwards that improvement in the price would be seen. Even though there is some relief with the improvement in the prices but there won’t be big jump in numbers especially margins beyond 10%

I am also wondering what’s their view on this commodity business, but their picks are very interesting. Shrimp price started raising since june’24 at the same time MIT entered.

In the recent concall mgmt told the impact of shrimp price rise will be seen in Q3 results. Here are the concall notes.

Can Apex really get the benefit of raising shrimp prices ? Management was highlighting the issues of procuring the raw material in concall (due to high prices). Also they dont have owned farms. They need to rely completely on farmers to procure the shrimp. Any idea if there is any shrinkage in the area of shrimp cultivation due to the issues the sector has seen in last few years ?

As per latest concall of Avanti, shrimp price appears to rise which is due to CVD imposed on India by USA. It can increase topline but nothing arrives at bottom-line.

So price rise of shrimp in recent time is not accepted by Avanti management.

I attended Avanti concall. I was the person who asked the question regarding shrimp price rise. In trading view we can clearly see from Q1 end shrimp prices has risen by 12% that can’t be due to duty hike duty hike which is in single digit. So their claim of no price rise is baseless. There must be supply demand mismatch. Supply from Ecuador is facing challenges due to energy problem there from the month of September this is from Apex concall. Also Apex management has told there is a lead and lag effect between getting the benefit of shrimp price rise. I asked in Apex concall about the time of getting benefit of shrimp price rise they told it will be reflected in Q3 result. Same thing they mentioned in presentation. As per my understanding Avanti on the other hand will not benefit much from this as they are mostly into shrimp feeds.

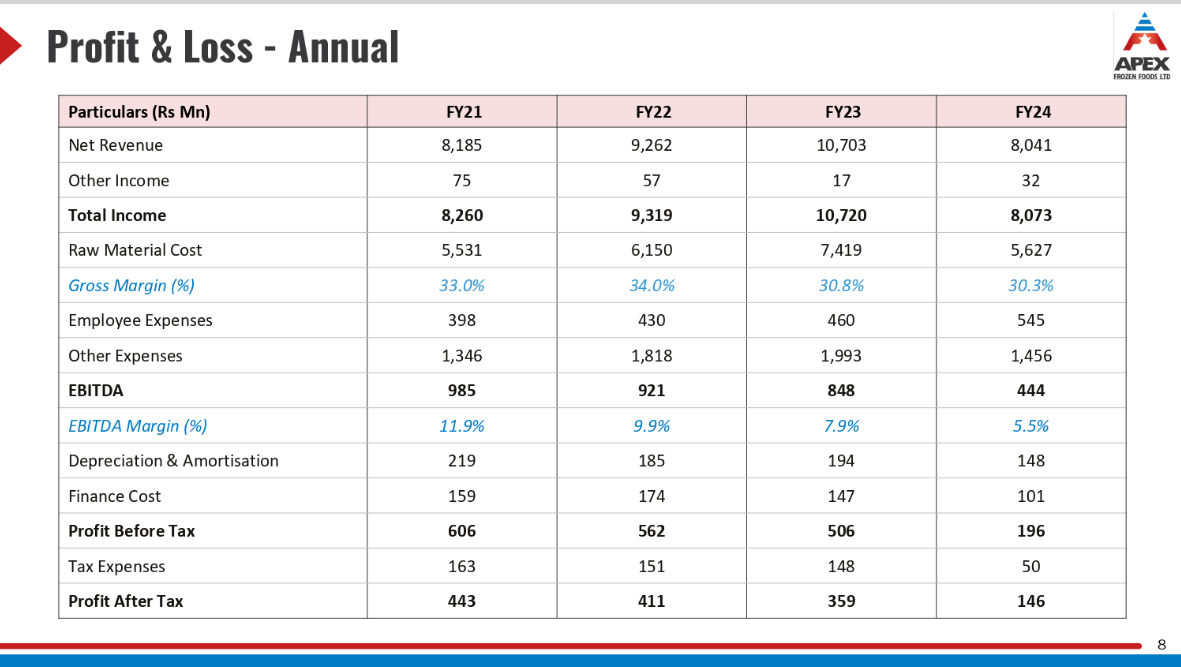

Why do you think so ? Compared to feeds, shrimp processing looks to be small. But its better than Apex frozen foods both revenue wise and margins perspective. Margins have remained stable around 14% in the last 6 years, where as Apex’s margins have degraded from 11% to 5.5%

Both the companies have more or less same shrimp processing capacity.

Avanti - 36K MTPA (out of this 7K MTPA commissioned in Mar24)

Apex - 34K MTPA

Farmers stopped cultivation of shrimps in the past few quarters due to low selling prices, they are not able to get any profits. This this caused the supply issues, still I don’t think so many farmers are cultivating shrimps till prices gets stabilise

Are we not looking at a classic mean reversion play?

Why there is mismatch between management commentary of both the companies? Is it due to conservative approach of Avanti management to promise less and deliver more? Requesting all senior members to share their views. This could be the good learning case for next shrimp cycle.

You don’t need any commentry to check global shrimp price. Go to tradingview and search global shrimp prices. Or search in google and open the tradingview link.

The delta in earnings is better for bad players when underlying comodity price rises which is the case now. Avanti maybe being a bigger player has better pricing power when purchasing raw shrimp or maybe they have shrimp farming. As the overall contribution of shrimp processing is small for Avanti so I think the benefit of shrimp price rise

will be not much to total number of avanti.Apexx doesn’t has shrimp farming. This is main reason for margin fluctuations. I don’t know if Avanti has shrimp farming as well. But Apex being a shrimp processor should benefit from shrimp price rise .sharat industries on other hand has shrimp farming as well they are getting the benefits.

There’s one point missed for advantage Avanti with the increase in shrimp prices, that is, now they can increase feed prices as the farmers can afford it.

The US Department of Commerce’s (DOC) decision to impose a Countervailing Duty (CVD) of 5.77% on Indian shrimp exporters, with slightly varying rates for two exporters, marks a significant development in the seafood trade. The increase from the preliminary determination of 4.36% came as an unexpected blow to Indian exporters, particularly as CVD rates for Ecuadorian and Indonesian exporters were significantly reduced.

This decision presents a dual challenge: heightened pressure on Indian shrimp exporters’ margins and intensified competition in the US market from Ecuador and Indonesia, whose cost advantages may now deepen. Farmgate prices in key producing regions, such as Andhra Pradesh, have already fallen as exporters attempt to mitigate the impact of higher CVD rates, further straining farmers already grappling with global oversupply and declining export returns over recent years.

The Seafood Exporters Association of India has expressed concern over the high CVD rate, emphasizing its potential to hinder competitiveness. However, the association remains optimistic about seeking revisions during the next review process, while also preparing to present their case to the International Trade Commission.

India’s ability to navigate these challenges will hinge on strategic price adjustments, operational efficiency, and leveraging its strong market position. However, the immediate repercussions underscore the need for resilience and adaptability in a highly competitive global shrimp market.