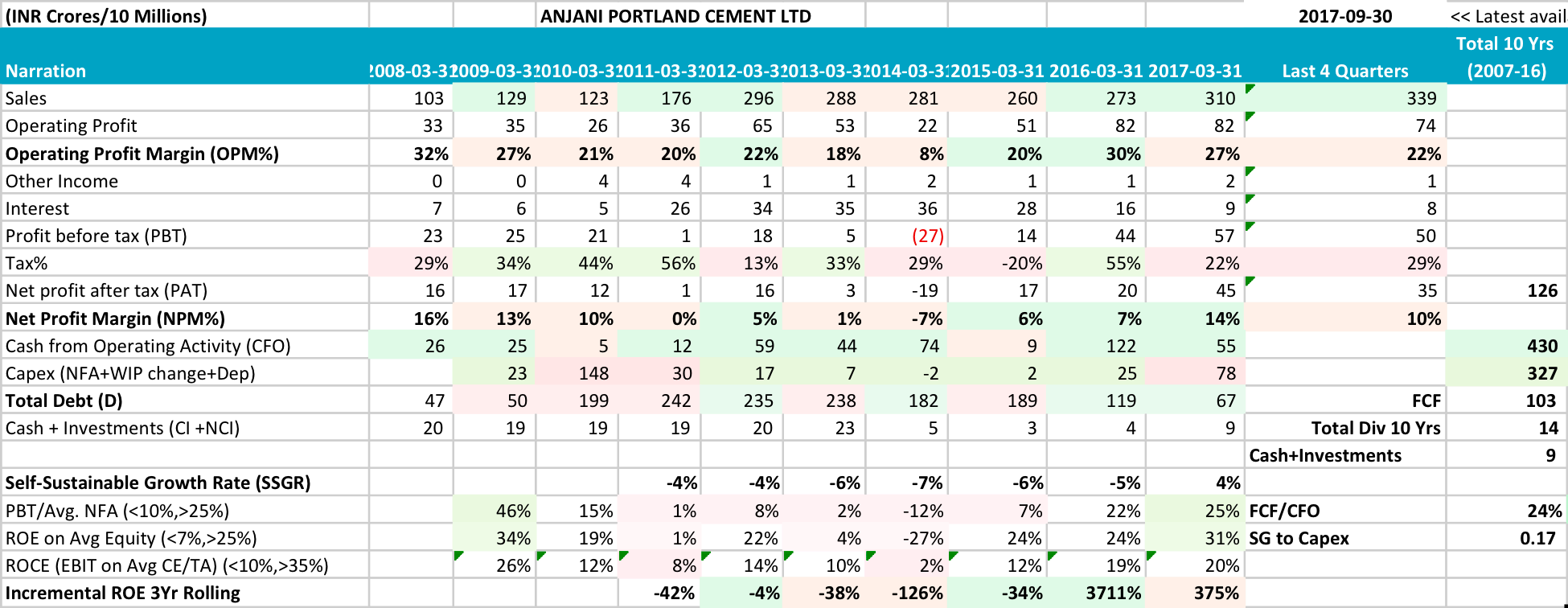

Anjani Portland is a small cement manufacturer with presence in Andhra Pradesh. It is closely linked to the cement cycle, as is evident from its financials. However, the firm has been able to pay down its debt significantly- from 242 cr in FY 11 to 80 cr now. This makes it far better placed to weather a downturn. For instance, an increase in the price of coal as well as increases in freight charges ate into operating margins in Q2FY18. However, the NPM did not decline as drastically as in FY12 and FY13, since interest costs are far lower now. Like most cement cos in the south, the firm operates at ~70% capacity. EBITDA margins have been at their lowest for the last 4 quarters yet Anjani is valued at just 7.8x EV/EBITDA, which is at a significant discount to many of its peers who have more leverage.

I see this as a mispriced bet. The replacement cost of a 1 MT cement plant is estimated to be USD 135-140 per MT. With 1.15 MT capacity and given that Anjani’s capex still has 80% of its life remaining, this would put its replacement cost at ~ INR 800 cr + another 80 cr for its captive power plant = a total of INR 880 cr. It currently trades at a market cap of INR 600 cr, which provides a 30% margin of safety.

Risks:

-

Freight costs are up 150% this quarter and the explanantion provided by the management is that the have moved from ex works pricing to FOB. However, other cement cos have not seen such a sharp rise in freight costs

-

Their presence at a single location may restrict their growth in the future.

Disc.: Invested