Amulya Leasing & Finance Company sounds like a leasing and boring company, however its core business is Plastic pipe through its subsidiary Apollo Pipe (Competitor of Astral and Finolex)

Apollo Pipe (APL) is part of sudesh group and is in business of manufacturing & marketing of plastic pipes & flitting.It is leading manufacturer with highest capacity at single location in northern india.

APL is diversified and focused into value added products such as cPVC, Column, Ribbed screen, ring fitted and plumbing pipe & fittings.

The current capacity of the company is ~45,000 MTPA which is expected to increase to 50,000 by FY17 end. Current capacity utilisation is 70%.

Its derive 70% of its sales through retail, 25% from government orders and 5% from institutional orders.

Financial Highlights:

Apollo Pipe is a small company and reported net sales of 200cr and net profit of (Pre-minority interest) 10 cr in 2016. ROE of the company was robust at ~20%. Debt to Equity stood at 0.6x.

Key Points:

As of now name of the company sounds boring and companies with boring names are easily overlooked, and therefore often trade cheap. According to Peter Lynch, the shares of a company with a boring name, or the shares of a company which operates in a dull industry, will often be undervalued.

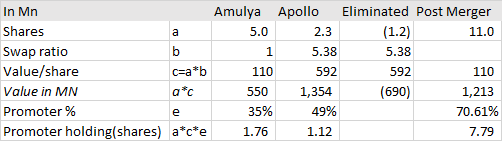

Amulya Leasing currently hold ~51% in the Apollo pipe and rest of the holding is with the promoter family. Recently, company has decided to merge the Apollo pipe with the Amulya leasing, post which name of the company is proposed to be changed to Apollo Irrigation. Post Merger, Promotors will have 70.62% shareholding in the new company and rest would be public holding. Company, expect merger to be completed by march 2017. Successful merger can trigger rerating for the company.

Company is targeting 1000 cr turnover over the next 5 years, led by shifting focus of the group from APL Apollo tube to Apollo Pipe. Company would be setting up new manufacturing facilities, target Pan India Market by leveraging APL Apollo Tube distributor network and would be adding valued added products to the portfolio.

Expansion is expected to be funded by internal accruals and debt. Management is confident of maintaining >20% ROCE & ROE.

Valuation: The stock is trading at ~11x FY17 Expected profit as compared to Finolex PE of 25x and astral PE OF >50X.

Key Risks includes increase in competition, failure of merger/change in group plan etc.

Firstly, nice catch on Peter Lynch’s approach-that is good

Following are my comments

Could you share the source of the data on order book, capacity, expansion, management intentions? I could not locate this from the company website

You are correct that promoters will hold 70.62% post merger. However, the Amulya minority shareholders are not getting the correct swap ratio-they were holding 65% of 51% in Apollo Pipes so they should have owned 32.5% in resultant entity. However, they only hold 29.4%.

As per the valuation report and swap ratio, each share of Amulya is worth only Rs 110/share(and this broadly relates to the valuation of Apollo Pipes). Why should one enter the share at Rs 200? If the promoters thought Apollo Pipes is worth more, they would surely have squeezed out more…since they hold 35% in Amulya but 49% in Apollo Pipes

3.5) The share price has jumped from Rs 112(Open offer price) in Mar 16 to Rs 200 now. The open offer had failed-is this why they are trying to merge?

4)Better value unlocking was to spin off the shares of Apollo Pipes or demerge the division. Also, ideally merger would be to merge APL Apollo and this entity-without this, business conflict will still exist and one set of minority shareholders would be shortchanged. The rationale for this is not clear.

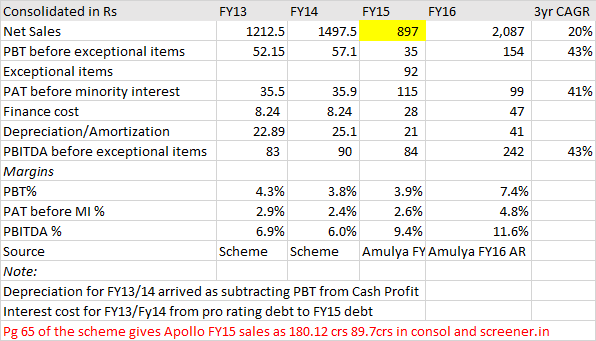

It is not clear why profit & sales improved in FY16…can you throw some light on the quantum jump in FY16-is it just a way to boost the ratio?? All numbers in Rs Million

6)Pg 65 of the scheme states FY15 sales as 180crs while financials states 89.7 crores. Which is correct?? Please note financials need to give 100% of the subsidiary sales even if just 50% is held, so pro rating is not the answer.

Given the issues above and the seemingly low present valuation, I think will give this a pass until better clarity emerges on reasons for underlying improvement of sales in FY16-in a situation where all other companies struggled to show sales growth.

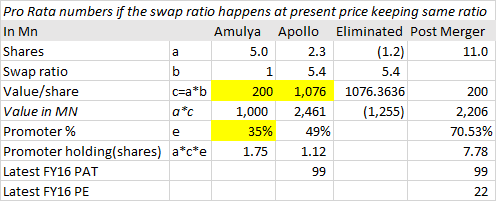

The merger to be approved will need approval of minority shareholders (and a special resolution). This is unlikely to happen if the valuation remains at 110/share(refer scheme of merger) as versus the current market price. Hence, if the merger is approved, the Amulya valution would need to be at CMP i.e Rs 200/share. If we revise the Apollo Pipes valuation also, the resultant entity would trade at 22 P/E basis present price and hence no upside. A classic case of efficient market hypothesis. However if merger fails, there is downside risk from holding company discount, yet no upside risk.

Knowing this, the promoters decided to sell 50% of APL to Amulya for just 9.9 cr at mere 19 cr valuation in Nov-14, when APL was expected to close yr 2014-15 with 200 cr sales and 14 cr profit. Going by their own admission of valuation, APL should have been valued at 800 cr

So much for ethical management and fair value

Pls go thru the last 6-yrs ARs to understand - Amulya Leasing was always a shell company mostly after acquisition by Sudesh family. I don’t know why promoters buy finance companies but some people do It’s hilarious to see how ARs can be written for companies which don’t do any business. Am amused to see their website now.

It looks like everything is playing out to a plan created yrs back to help the dear brother.

Disc, though not reqd based on my comments: Not invested

This is one story that has intrigued me though I haven’t gotten into the details ever. The link between APL Apollo Tubes and Amulya Leasing was the one grey area I wasn’t too comfortable with when I was contemplating my investment into APL Apollo Tubes in 2014. I eventually took the plunge and went ahead because the story was just too good even after adjusting expectations for this grey area.

APL Apollo Tubes promoter family is now focusing on improving corporate governance, hence the change of auditor to Deloitte and subsequent changes in some accounting policies. My perception (based purely on business performance and the vision articulated by the management) of the promoter family is that these are very grounded, street smart people who know how to get things done. APL Apollo Tubes will end up being the darling of investors going by the business potential and the length of the runway available to them. I would be surprised if they do something silly in APL Apollo Pipes/Amulya Leasing from here on since that will reflect badly on the bigger business as well (APL Apollo is valued at 2200 Cr now and is likely to be valued at 4000+ Cr 3 years from now - of course as per my own conservative analysis)

In such scenarios where there is a large corporate action coming up, my approach has always been to sit by the sidelines till all news is out in the open and then take a call. I do not like analyzing situations where I have to cut through promoter intent behind a corporate action in addition to analyzing the worthiness of the business. I am waiting for the event to play out, will then look at this story

Some notes-

Apollo pipes is into plastic pipes as well as fittings.

Current production is 2500 T per month… Largest players in industry are at 15-17 kT per month. We are in top 10-15 players in industry. This is a fragmented industry with only few large players.

Capacity is 3200 T per month.

So, utilization is 80%. This is as good as full as can’t operate at more than 80-85%.

New production is coming up with 700-800 T in next month.

Then working on Gujarat expansion… Looking for land there… Plan is 1000 T per month from there.

So, final = 5000 T… We will be in Top-6 then… Funded largely by internal accrual.

No agreement with Apl Apollo. Just some distributors may be common and promoters are common.

Industry has 40% capacity with unorganized players. Gst will help organized.

Major push now on branding… Doing plumber meeting, dealer meeting.

Target= 25% growth.

We try to maintain prices (new capacity coming up, so we are not taking price cuts to sell that).

Realization per kg= 80 rs.

Crude movement affects revenue but not ebdita.

Ebdita/kg stays nearly same.

WC cycle= 90 days.

15-45 days is usual credit period.

Merger- got exchange approval recently.

Now to go to Court.

Expect to do in 6-7 months.

Looks like the re-rating triggered by merger talk has largely played out at this price. It’s prudent to wait until the event actually happens and see what picture emerges.

This merger with a listed company is more like an IPO of Apollo Pipes to get the later listed. Nothing wrong with that. Avoid the hassle and costs of IPO.

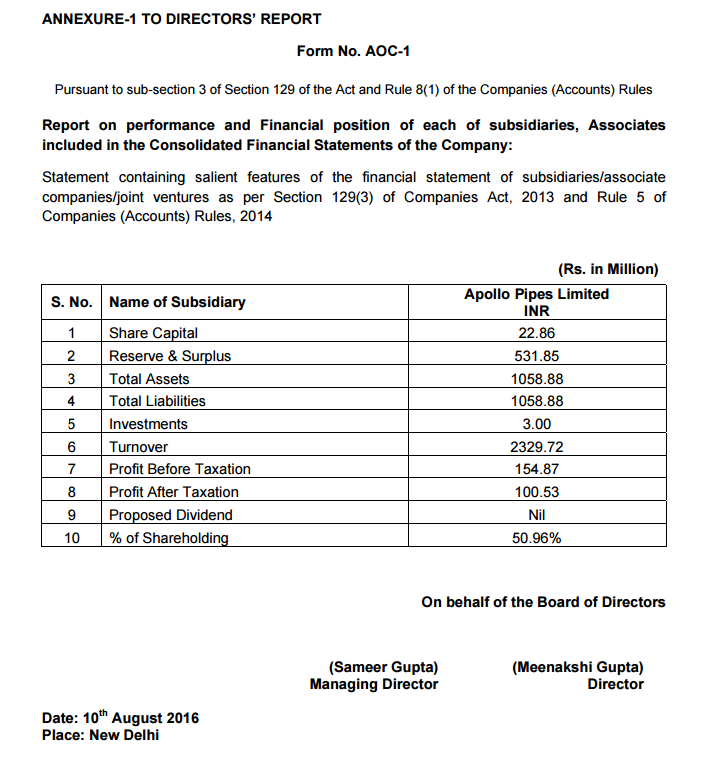

This is from the 2016 AR. Annexure 1 contains the financials of the subsidiary Apollo Pipes. The account equation says Assets = Liabilities + Equity

In this subsidiary, Assets = Liabilities with no twin entry that balances the equity side. I found this odd. Sharing here to get peer views on this issue. Anyone else found this odd?

Hi All,

Posting discussion on some other thread here. Possibility of demerger in 2 months (not verified but expected) hence inviting comments from fellow members who are tracking this…pl suggest if it is it right time to enter.

I recently analysed the company and it looks like a good pick to me even at current prices.

Amulya leasing is a holding company of Apollo pipes, maker of PVC pipes based out of North India. Apollo pipes and Amulya leasing will be merged and name will be changed to Apollo Irrigation. Apollo pipe is a private company. In the merged entity, promoters will be having a 70% share. Amulya has no other business rather than being a holding company. At current price of 300, post-merger P/E would be 21.5. Talking about the industry, I see PVC pipes to be doing good in the coming years with housing, irrigation headwinds. Management is expecting 25% revenue growth and I think it is possible beacuse of the low base. Organised PVC pipes is 60% and I think it will increase rapidly.

PVC pipes are light weigh, corrosion free, long lasting, durable, no reaction with chemicals and have longer length and thus joint free.

Capacity is 48K mt/year. 500-Sales staff.

Talking about financials, margins in pipe industry are fairly constant and crude doesn’t have a big impact. Gross profit margins are 26% and Ebitda margins are 13.3%. Raw material cost is 74% which is 3% higher than Astral pipes, the leader in the market and this may be because of the price premium they would be charging. RoE and RoCE are comfotable at 22% and 20%. Working capital cycle is better than Industry leader with Inventory days and Receivable days at 35 and 52 vs 48 and 66 for Astral. One reason for this may be 70% sale to the retail segment and 30% to Institutional. On the investment side, it has 3,00,000 shares of APL Apollo tubes which at current price will fetch 50cr.

In such a small company with revenue of 240cr and M-cap of 150cr, I think one or two years time and one major capex can do wonders and help company reach entirely different orbit.

On the debt front, it is pretty comfotable with EBITDA/Interest of more than 10. Tax payout is 33% constantly thus we are safe on that front.

Taking about the management, company is a part of APL Apollo group and they have been wealth creators. Younger brother looks after the pipe business and are extremly effecient. APL apollo tubes is India’s largest steel pipes company and has shown consistent high growth.

Brand they use in pipes is APL apollo and it is very well known in the market beause of steel pipes division.

In terms of margins, Q417 was exceptional with EBITDA margn of 16.2% and raw material costs at 72%.

Taking about valuations, it is available at 21.54 P/E post merger and revenue multiple of 1.38.

Astral has a P/E of 77 and revenue multiple of 5.58.

Finolex has a P/E of 21.6 and revenue multiple of 2.67, they also have a raw material plant

Concerns -

1- It is under the GSM security list and we have to pay 100% margin even in the cash segment

2- Capacity that Finolex and Astral have. They have huge excess capacity but I think in a Industry that is set to grow at 15-20%, there is enough space and every company can make a mark for themselves. Plus, I am not worries since revenue for Amulya is still very less

3-Delay in the merger

I think market will rerate it with merger taking place and if 25% growth happens, it will be a huge wealth creator.

I am new to valuepickr and will be happy to get feedback!!

Sorry for asking a stupid question but does the GSM rule still apply if the merger happens. GSM was there because exchange only looks at standalone numbers and once merger is completed the standalone numbers will be quite good?

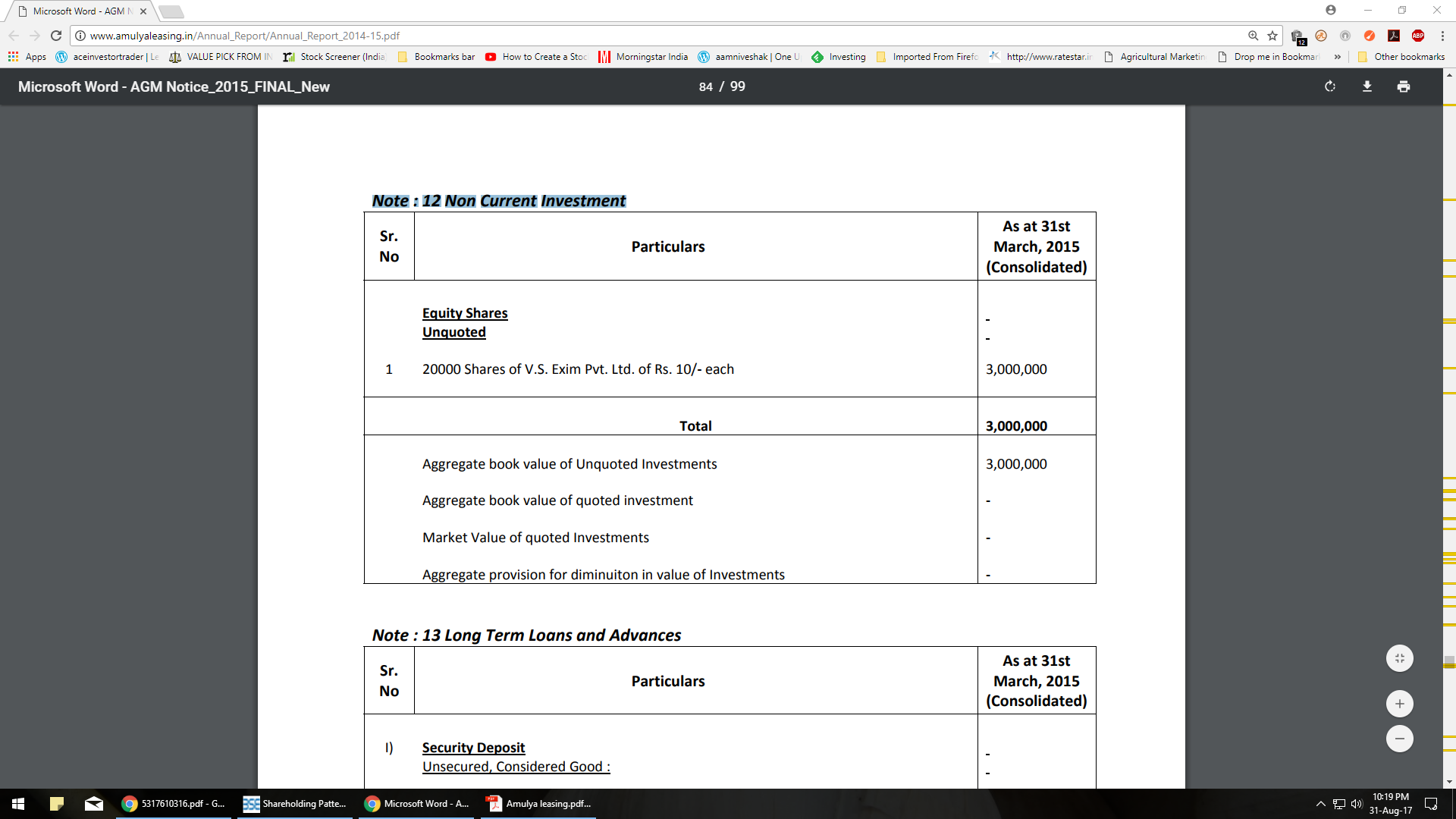

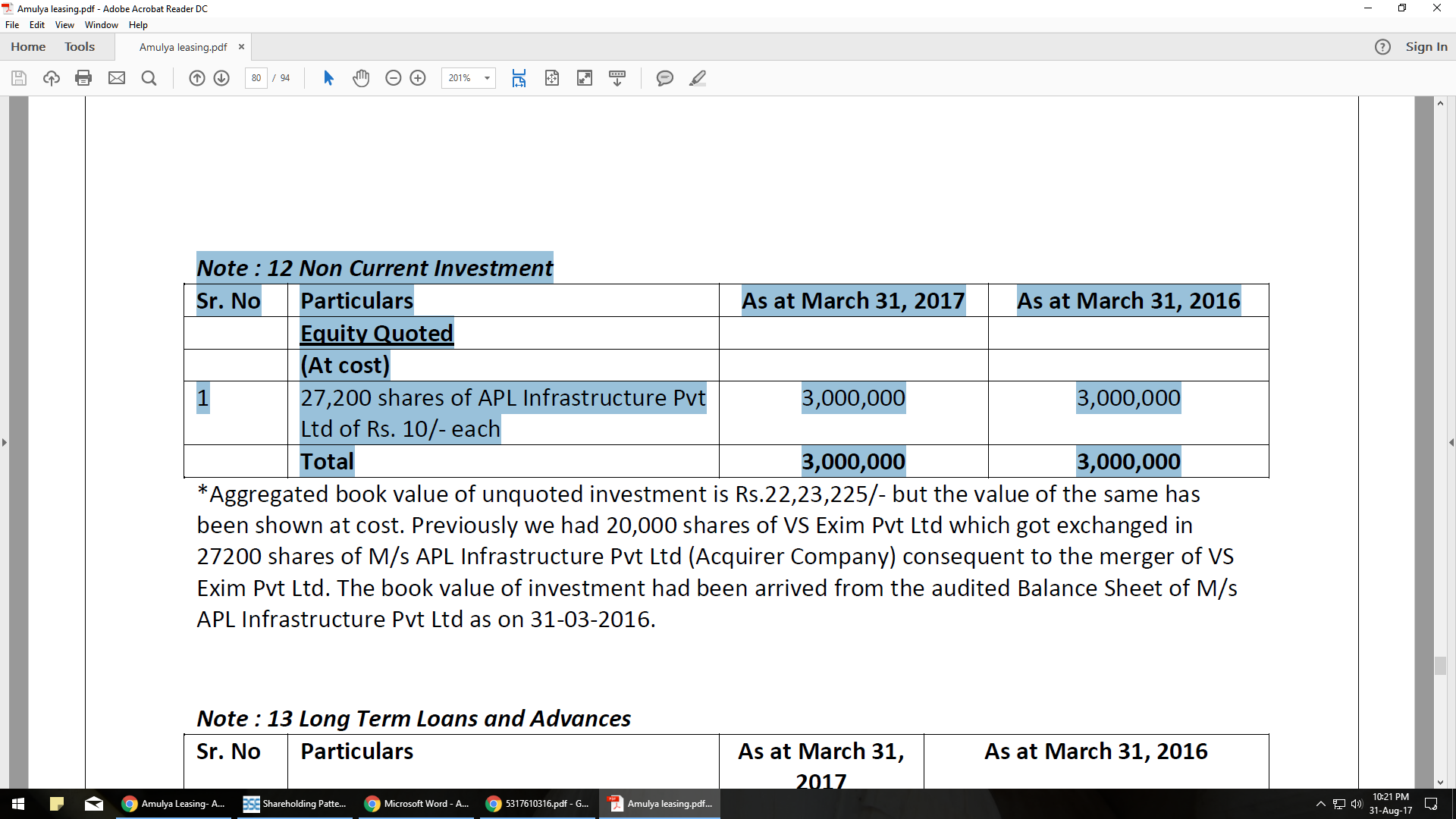

I m attaching the screen shots for the Note : 12 Non Current Investment, Year 14-15, 15-16 and 16-17. I found some discrepancy and i could not find the solution so just requesting boarders to look in to it. If holding shares then just write mail to the management for clarification as i do not hold it right now.

Could not the relation in terms of Value wise between APL Apollo Tube, VS Exim Pvt and APL Infrastructure Pvt ltd.

If we just consider the APL Apollo Tube as the right holding then the value will be around 47 Crore for a 140 Crore market cap company.