I think as per my info only Rajapalayam Mills of Madras cement group came close to Ambika in terms of quality.However since last 3 years it has gone into problem of its own like debt etc while Ambika has moved ahead reducing debt and controlled growth.

The key differentiation for Ambika imho is

1)Technical skill of Chandran and his team which are closely guarded business secret. Chandran spends lot of time at his mills in Dindigul which works for 361 days in a year. .Though he is 64 he is very fit leads a very disciplined life style and has clean food habits. He accepts the order only if he gets advance and adequate margin.

2)Ambika customers are top notch who appreciate real high quality .The special yarn is sent to China for fabric then to Vietnam for Stiching and then to Japan as shirts in top notch premium stores.Pacific textile group is their main customer it seems.

He being a veteran of textiles industry he has learnt from the mistakes of other cos like Alok who went in for reckless expansion with huge debt.He too has taken debt but mostly from TUFS at 5% concessional rate and has now turned the co into zero debt.Focus is on increasing the EPS and dividend by reduction in interest and power cost and other savings.Now that debt is zero he will go for expansion relying mostly on internal accruals

The company seems to be a typical first gen entrepreneurial company which we very much like at VP where hands on promoter eats sleeps and breathes nothing but Ambika.His execution is superb and now that tailwinds are tehre is the co on cusp of big opportunity?

Really happy to see such a wonderful flow of discussion…this is the strength of VP - with collaborative work we are able to discuss on a company from so many angles and learn so much!

Coming specifically to Ambika - a lot of points have already been covered. However to summarize - Good thing about Ambika is that it has always had very good margins and they used to be quite stable despite high cyclicality in the industry - for eg - a comparison with Nitin shows that though Nitin has had good margins but they got badly hit in bad years (though the story may be changing now) which says a lot about the customer relationships or the niche Ambika is operating in. Its also really commendable that Ambika has focused on de-leveraging the balance sheet over last 4 years and reducing loans from about 260 Cr in 2011 to almost debt free now. At the same time the turnover has increased from 320 Cr to 500 Cr in this period without any material capex thereby resulting into significant improvement of ratios like fixed asset turns, inventory turns etc. Though there has been deterioration in margins but this kind of change is not easy possible in a competitive industry like textile - so will still need to specifically understand the reason behind this change. One reason could be - like Donald has hinted - that the co has gradually moved to 100% premium yarn in recent years and also as its a niche high end area, it takes time to scale up. If yes, then its a very good thing for the company. Also, why has it come at the cost of lower margins?

We also need to understand about the growth prospects going forward and also the capital intensity needed for the same?

had discussion with a industry person one month back, here are highlights [from memory, that time failed to make notes]

Compact yarn is in various counts starting from 10s to 140s. Ambika cotton is mainly into higher grade super fine cotton which starts from 40s and major production is into more than 50-60 counts.

higher counts [> 50s ] is a specialized field with higher margins. End market is not that large. He seems to be worried about growth and said long term growth may be ~ 15% not more than that.

Its not difficult to manufacture super fine cotton. Just like what Kitex is doing is not difficult for anyone else to do. end market is not that large. Someone cannot built Vardhaman textile like scale with only focus on super fine variety

Main thing is attitude. Ambika attitude is to focus on margins and not scale. Generally players focus more on scale than on margins.

Lastly even in China it may be difficult to find one single player with Ambika size super fine variety cotton scale. China focus where end market is large

Moat is to some extent reflected by High ROE compared to all other players. If one runs a simple screen where in to find textile companies.Filter applied M.Cap > 50crs, ROCE 10 yr avg > 10%, ROE 10 yrs AVG > 10%, Sales/total assets> 0.8 & Assets/Equity < 3x [To select companies better than Industry average]

Out of 560 companies only 15 could satisfy above simple criteria of average ROE & ROCE > 10% in textile companiesâ.Ambika is one among them.

of-coursewe still need to look for sustainability, but should give equal importance to history. Most important questions are just two in my opinion

1)Sustainabilityof ROE 2) Sustainability of growth. Ofcourse to answer these two questions, all the questions raised by donald on Industry need to be answered.

Please find attach comparision of Thiagaraja mills [TM] with Ambika cotton [AC]. Table is self explanatory… Major points to be noted

Sales CAGR of AC for last 5 years is 23% compared to 16% for TM

EBITDA margin of AC more stable compared to TM in down years like 2010, 2012. I guess major reason is AC orders Raw material against orders, i assume TM might not be doing this.

Drastic improvement in WC as % of sales for Ambika cotton from 50% to 22%

For FY 14: Premier mills [PM]was awarded gold award in exports for cotton counts > 50 in 50-500crs category. Second and third place won by GTN & Vardhman. Surprised not to see AMbika cotton. Here is the linkhttp://www.texprocil.org/cdn/gallery/3715.pdf

Please find attach Premier mills financials. This looks like a perfect comparison with identical capacity, product and export. On many paramaters PM appears to fare much better, particularly on margins and ROE front…excel file is self explanatory…

File is too large to attach. please download it from herehttps://www.dropbox.com/s/aamnofgmxaokg0h/Premier%20mills%20pvt%20ltd.xlsx?dl=0

I have been following this thread for a while. Looks like AC is definitely an above average(if not one among the top 5) well run textile companies. But we are not sure if it has a moat that its competitors does not have.

With the information at hand, have you invested into AC? (This question is only to understand when to enter. )

Great discussion. Thank you for sharing all the valuable information about the Industry,Company and the Promoter.

I came across this company sometime in last September for the first time. The numbers were decent as they are now. The working capital Requirement and the Nature of the textile Industry kept me from researching further. I later happened to see it in Kenneth Andrade’s portfolio sometime in December.As a lot of you must be knowing, Kenneth Andrade’s portfolio is quite something, he has a collection of moat businesses in his portfolio (Though i am not aware about the price at which he got in into each of them). Since, then I have been trying to find out about the moat the business has and the sustainability of the moat. The only thing I came across again and again was that, the company is into specialty yearn business that sells at premium.

I understand the company has built wind power generation facility, that ensures that power and fuel prices are low. They had a power and fuel cost of less than 5% as compared to around 10% of Vardaman (a much larger player) that will help it sell at cheaper price than a potential competitor and still remain profitable. But, this cost arbitrage would eventually be replicated and would not count in the long run as they do not have an extra-ordinary scale and hence the challenger would not have to bleed cash for a long time.

But, my question is the same as Donald Sir’s and a few others, “What is it that will ensure that the company will be able to increase prices, when potential competitors start replicating the product?”

This is a B2B business,that as per my understanding sells premium commodity.I believe, such a business requires a super manager. The present one has probably evolved into one. He is in his mid 60’s. What about the succession? What are the odd’s her/him being a super manager?

At a PE of 10x this looks to be fairly valued to me. However considering the global liquidity glut and stretched valuations of most companies in general it does not seem like a bad place to put your money.

Although it seems like a good business the un-branded textile segment is a bit commoditised and we need to make sure that the drop in margins are not due to structural factors. Margins are probably the only question mark.

Good discussion and great new look website. Well done Donald and team!

I would like to present one point of view. In most of the textile process business machines keep getting upgraded every few years and they are costlier too hence eating up capital.

Does any one have information of what are machines used by ambika cotton mills and are there any innovations going on manufacturers end to launch new machines?

I have been researching this company for the last 2 months, and fully convinced about its story. My analysis points are mostly covered in the points covered by other members. My only 2 points of concern are as follows:

What is its growth strategy?

Mr. Chandran the CEO owns only 9% in the company, rest 38% of promoter holding is held with a guy called C Bhavani who has NO position in the company. I understand from yarn industry sources that Mr. Chandran sold his stake to Bhavani in 2005-6 (around that time) when he suffered a big loss. This guy is based in Dubai and is a friend of Mr. Chandran. My point is here is that ppl in the yarn industry say Ambika is 99% the company what it is because of Mr. Chandran and the day he leaves the company or is forced to leave the company, then thats game over for Ambika. Also, who is this BHavani…i couldnt find any details on him anywhere.

Ppl in the industry have tremendous respect for Chandran and they feel the company has and will grow in the future. Chandran is known for his sharp acumen in selecting the cotton (raw material) as the one of key things in yarn is selection of raw material. His technical know and keeping track of all day to day operations is seen as v v imp and essential by the mkt players.

Time to capture some of the learnings from speaking to Industry folks

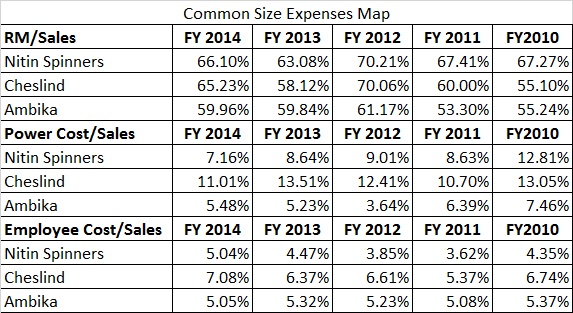

Nitin Spinners is a Rajathan based player whereas Cheslind and Ambika are Tamil NAdu based players.

For the yarn industry, RM is the biggest component of costs. Next big component is Power

Many South based players have invested in Captive Power. There are also some who haven’t like Cheslind who face huge disadvantages - much higher power costs, as also non-tariff barriers like higher peak charges, heavy surcharges for drawing higher power during peak time, and non-availability

Cotton production main season is Oct & Nov. Best Quality cotton and higher volumes is available then. Those with the strong financials are able to procure at that time in bulk and lock in prices at stable range. They have to carry 6 months of inventory.

Not everyone can take that risk, because prices can correct badly - as it happened in 2012. Correspondingly commodity yarn prices would crash badly in tandem. Most people thus prefer to buy only 2 months inventory. Accordingly they can pre-book sales for a month or two

There is also a speculative element to this. Out of 10 years, in 7 years you will find off-season cotton prices go up; which means yarn prices go up in off-season. That’swhy folks resort to 1 or 2 month pre-booking at most. But the 30% of time that prices go down in off-season, one can be badly hit. 40 count selling at Rs 200/kg usually will then seel at Rs 150/kg or less

From the Table above, It is evident perhaps, that Ambika Cotton

a) might enjoy some advantages in Cotton procurement over others, as also

b) might be fetching significantly higher realisations - for its consistent higher quality (?)

How did you calculate the RM cost? What all have you included in it? I have the numbers for NItin with me and they are slightly different. My RM cost for NItin for FY14 comes out to be 61%

Below is the table for NS.

I include COGS plus change in inventories and purchases in this… do you include anything else?

Sorry - Didn’t mention just RM cost head was taken for all 3.

We are looking first at the broad trends, so you may like to present a like-to-like comparison among the 3 using all the heads as mentioned.

These inputs from industry are great. Among players in the high quality yarn production, are we boiling down to low cost as the moat for Ambika?

In this case in addition to lower power costs, the windmills installed also help improve capacity utilization which in-turn reduces capex needs and lowers costs per $ of sales and improve revenues.

If the moat is cost-advantage, let us invert and think about what are the things that can takeaway this advantage and impact margins in a big way. Here are few that I think are some concerns

Management skills (If Mr. Chandran steps down - succession plan)

High volatility of raw material costs - increment in cost of cotton imports (although this is a challenge industry wide, it will impact margins even though will do better than the industry)

Improved power situation for textile companies (seems to have a low probability in the next 5yrs)

Hold your horses. More data to come

To bring everyone on the same page, its better to present in steps

Compact spinning is firmly established - key benefits

a) can use lower cost RM

b) productivity & efficiency

In next 10-20 years, most players will have to shift to compact from conventional, if they are to survive.

Finer counts production - is not everyone’s cup of tea. Very high level of operational skills needed. Needs professional sales & marketing too. Most players in South (50% of total yarn players) are owner-driven groups, who haven’t moved up the chain. Most rely on Merchant Exporters from TN who are doing very well. They are exporting 1000 T /month and don’t own any mills, creaming off the gains !!

Disc: These are from first level discussions with one player aimed at high-level understanding of industry. In the VP way, Incremental domain understanding comes from refining these with the next, and the next we meet by asking 2nd level, and 3rd level questions, as we understand more. You are encouraged to cross-verify every bit of this data from other sources. Data should be broadly correct, but imprecise.

Superb data Donald. Thank you for sharing this. Will try and supplement on this work by talking to people in the industry…

In the interim, posting some data on Nitin Spinners which broadly confirms your data. They are more in the 8-40 count rage as far as my understanding goes. Their realizations at this moment is 209/Kg.