The two shades of DPD - Nice cover article in the May edition of Maritime Gateway.

Basically, what they say is that more DPD volume is making it difficult for the consignees as segregation has to be done at the port and the containers have to be cherry-picked for each client. That makes the dwell time longer. And port infrastructure doesn’t support this kind of activity. That’s why most ports are built for CFS model.

CFS operators can do two things -

Concentrate on export and domestic, and less import.

De-notify some of the areas in CFS and use it for warehousing.

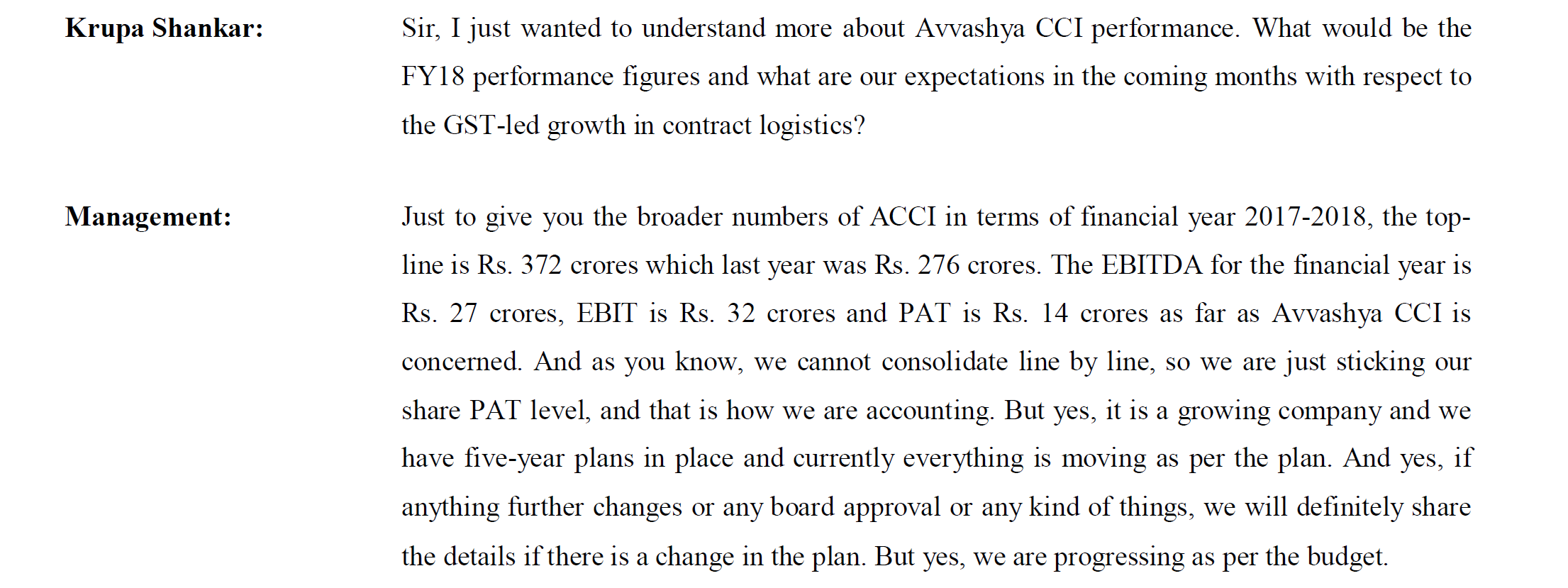

In last concall during reply management said that under ACCI revenue for 2017 -18 is 372 cr compared to 276 crores year ago. screen shot of concall is attached.

how ever PAT figures are matching in concall and AR.

Mahindra logistics (ML)is also in contract logistics, mainly supply chain management. ML’s revenue and profit are increasing quarter on quarter.

This quarter the share of profit from associates and joint ventures increased to 3.30 cr, which includes profit from ACCI.

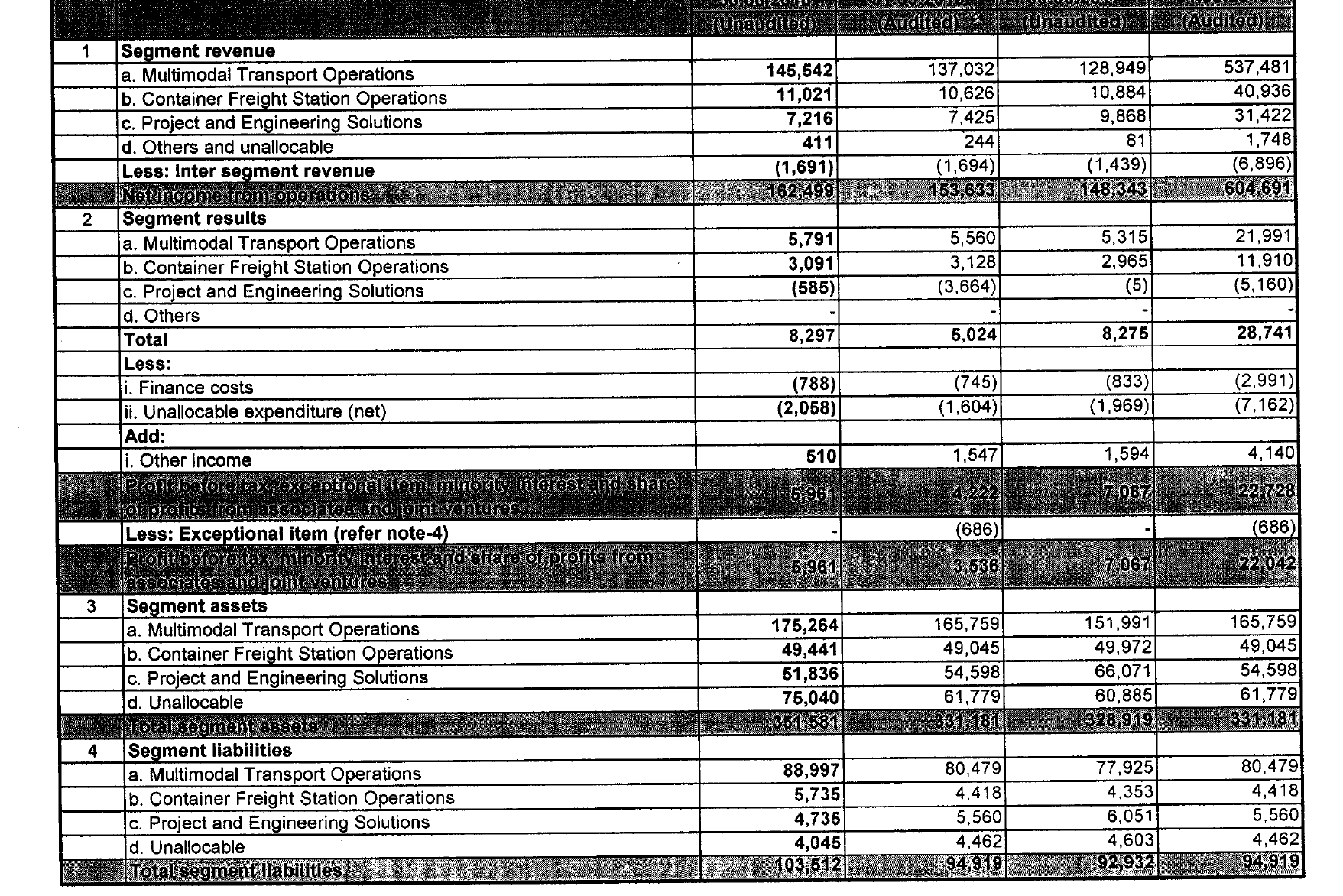

In last concall they also said that Project and engineering segment seeing utilization grow from 35% to 50% but we dont see any growth in revenue from P&E segment.

Infact revenue declined from 74 cr last quarter to 72 crore this quarter.

Waiting for concall.

I think the utilization was expected to grow up not because of increased revenue but rather by sale of unproductive assets. In other words, say there were assets were worth 100 Cr and utilization was 70%, then revenue say was 70 Cr. Now if the company sells, assets worth say 20 Cr (which were underutilized), and the company is able to generate revenue of about 64 Crores, then utilization became about 80%, despite decrease in revenue.

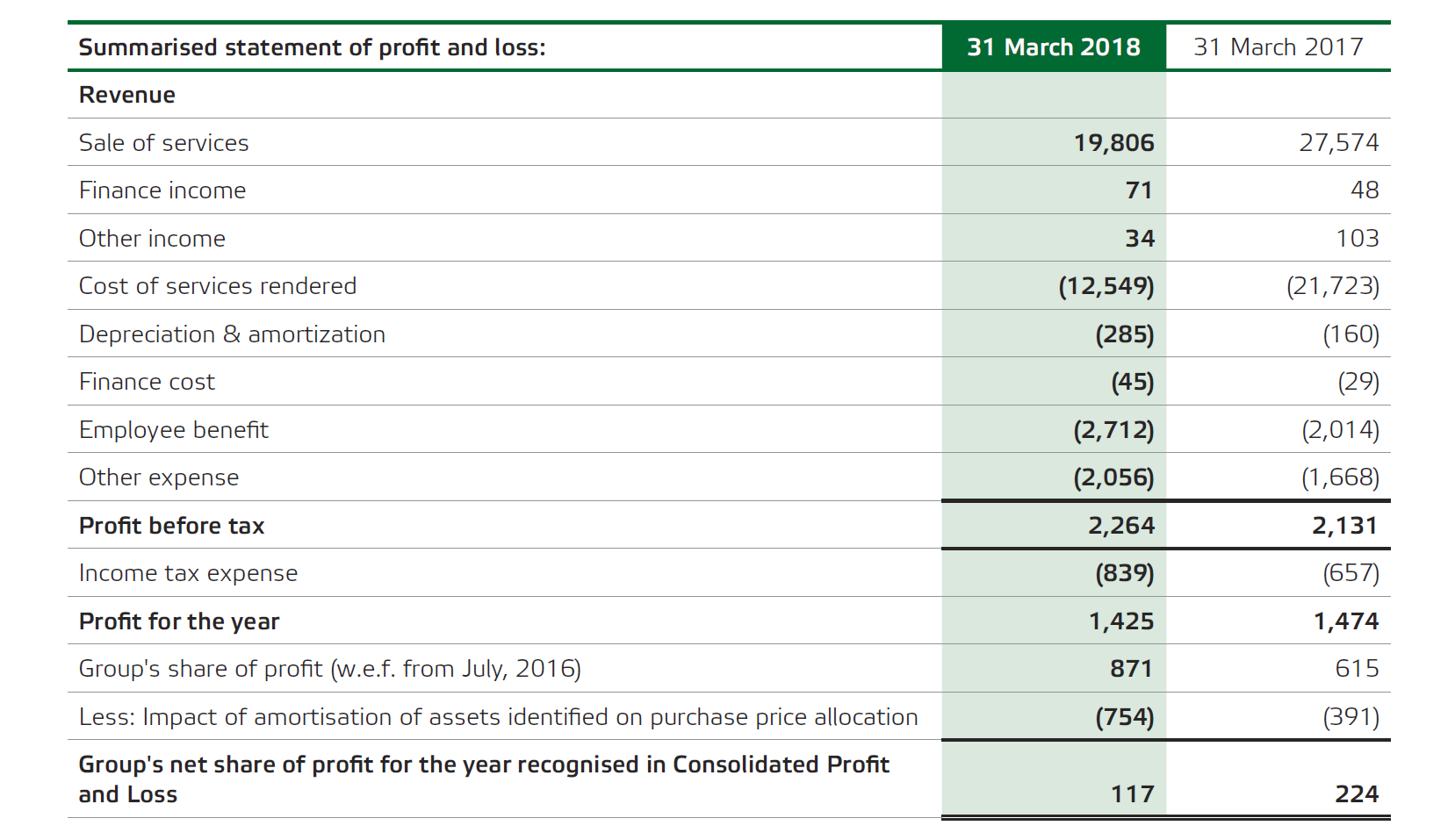

Not sure, but given that Allcargo holds about 60% in ACCI, 3.3Cr share of profit for Allcargo translates to about 3.3/60% ~ 5.50 Crore profits for the ACCI as a whole. So given last years total profits of 14Cr (averaging about 3.5/Qtr), there is significant rise in the profits for this quarter.

Revenue part from Balance Sheet is mismatched. Will definitely need more clarification there.

Yes. Assuming that other JVs and Associates also contributed positively for the total profit, the company’s aggregate profit from JVs & Associates has definitely improved at 3.3 Cr vs 4.8 Crore for the whole of last year. Even considering the write-down in investment of last year, there is somewhat an increase in the share of profit.

But certainly more clarification needed from the management for exact figures

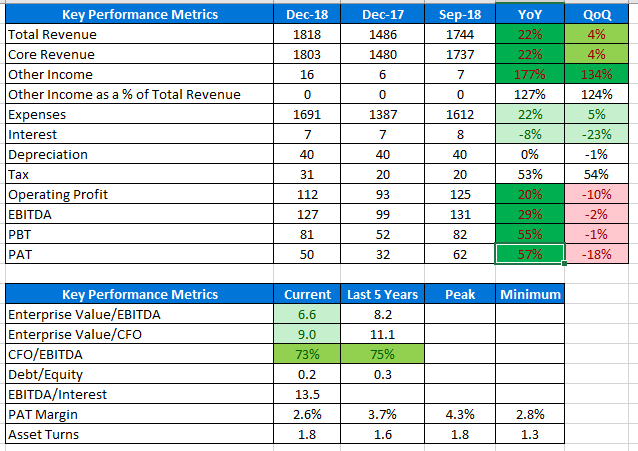

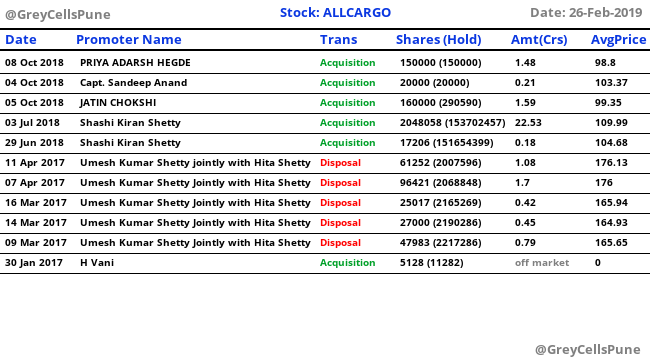

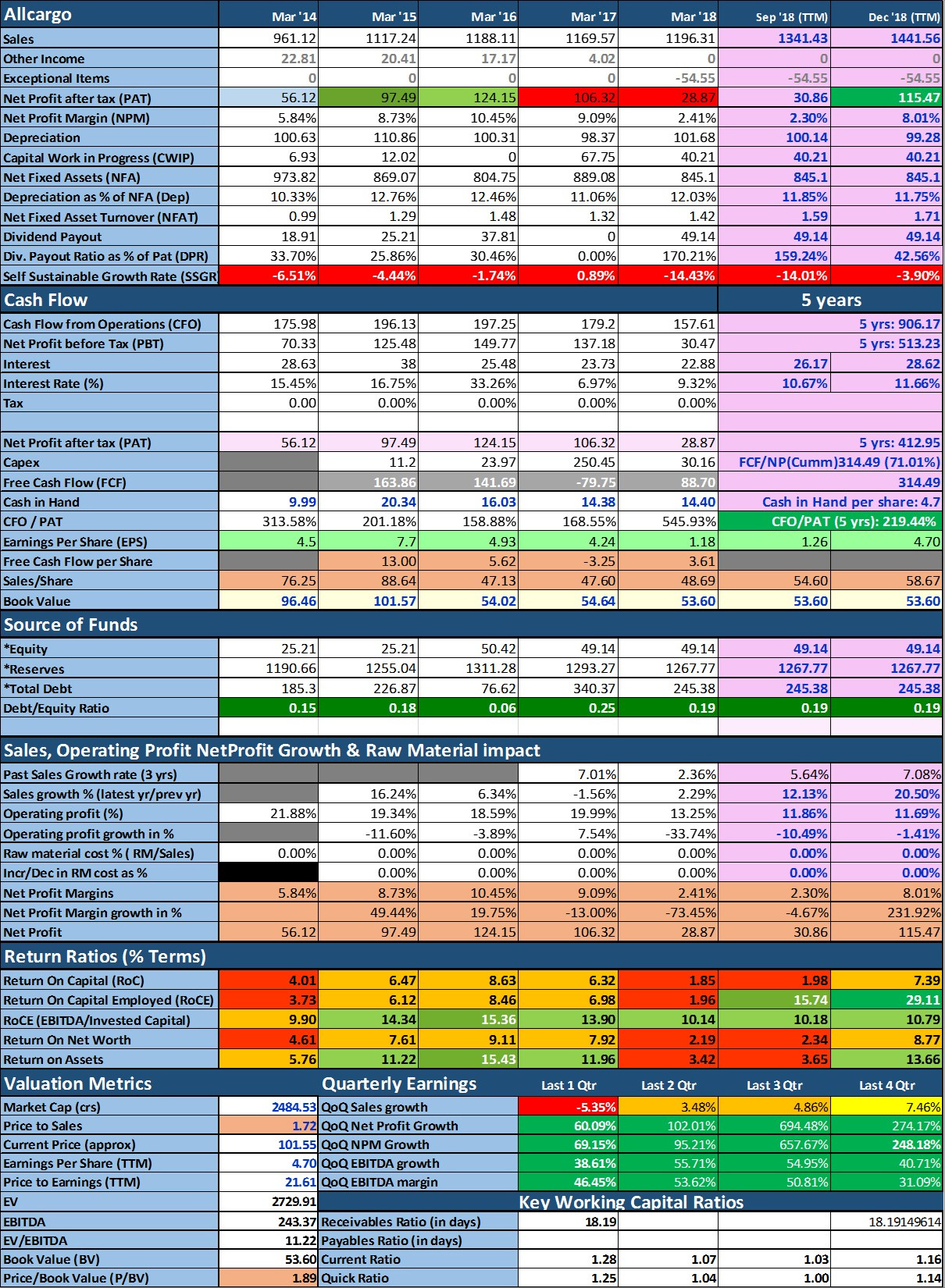

Super results by Allcargo. Last quarter looked like P&E division losses are bottoming out and this quarter further improvement. Company is currently doing 2.8% PAT margin against normalized margins of 4.2% and avaiable at 9x cashflow from operations at lowest margin. Also, 3 warehouses which should add to top line and hopefully with better margins should start adding in next 12-18 months. With light balance sheet, company has sailed through tough times. Also, recently promoter accumulated around 110 from open market. Not best of the business but think current valuation provides enough margin of safety. More of value valuation gap play for me

Disc: Recently invested as part of value valuation gap play

@maven26

Looks like you have posted the standalone numbers.The consolidated numbers have revenue for 2018 as 6k crores and book value close to 80 rupees.

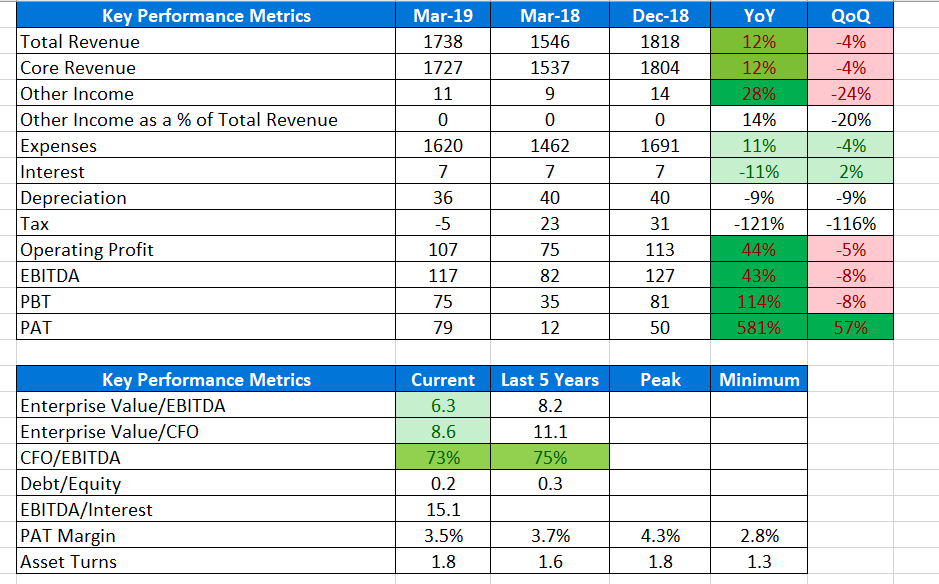

Cyclic turnaround continues and P&E division is back to profit. Core businesses keep doing well. Both top line and bottom line growth is back. Margins from worst 2.6% have improved to 3.5% and close to 5 year average of 3.7%. Leverage position looks stronger with EBITDA to interest improving from 13.5 to 15.1 QoQ. Overall, good results. Need to check how has been cash flows