(Reuters Breakingviews) - Indian developers are going downmarket. Luxury homebuilders are shifting their attention to cheap housing. Demand is strong thanks to a raft of government incentives. A boom could provide a big fillip to the economy, creating demand for everything from cement to home furnishings.

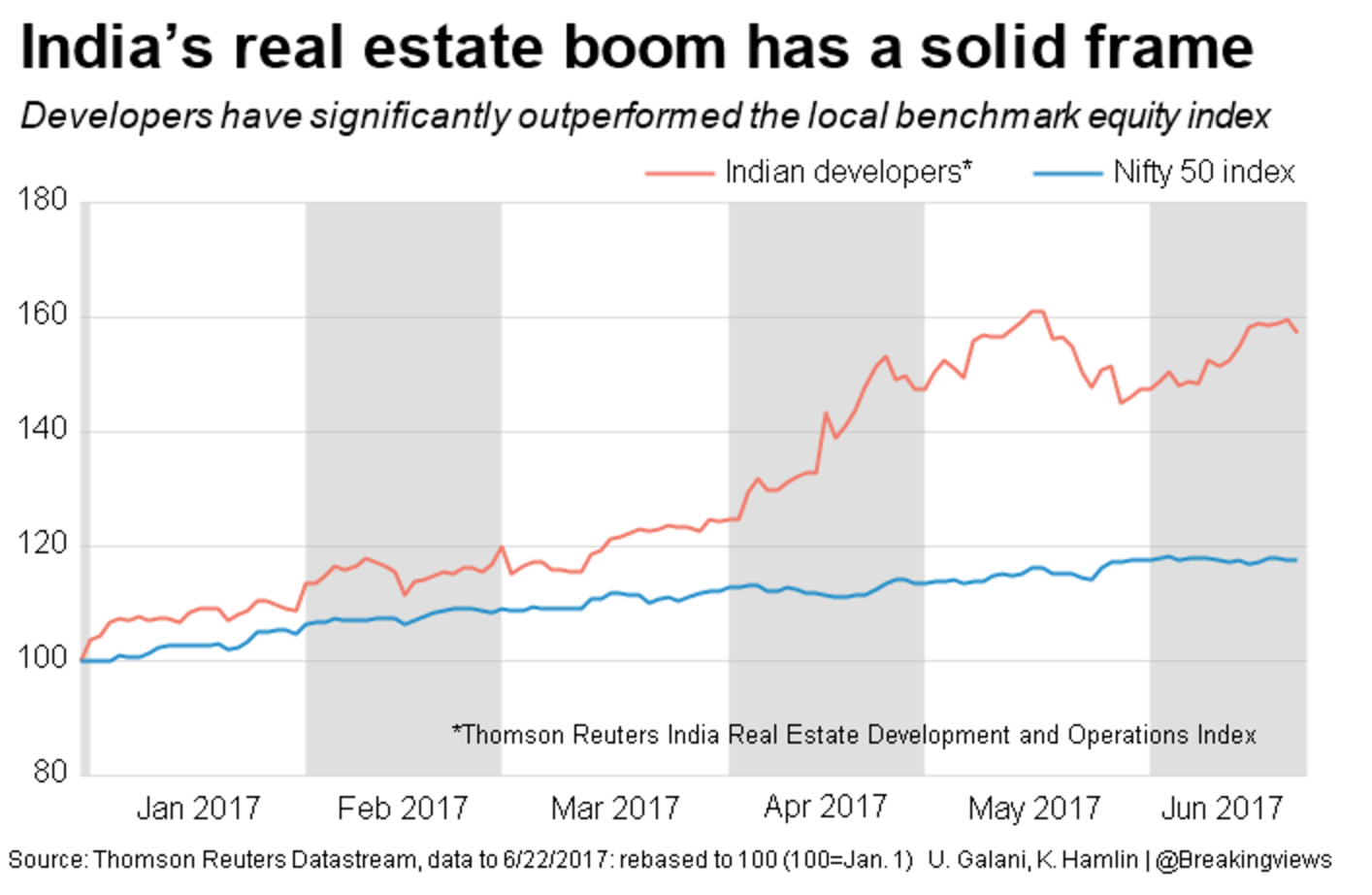

This all helps explain why the Thomson Reuters sector index is up almost 60 percent this year, more than three times the benchmark Nifty Index. And why Shankara Building Products , a newly listed midcap, is touted by one hedge fund as potentially India’s answer to Home Depot, the $190 billion U.S. DIY giant. Politicians just need to play their part and keep the supply of land coming.

Yes. One of the condition is that profits are subject to MAT. However, since we are eligible to MAT credit for 8 years it does not hit P&L statement.

It will definitely affect the cash flows.

Wonderful thread initiated by @bheeshma… Just want to add the pipes manufacturers like Astral CPVC pipes and fittings, the largest manufacturer and suppliers of Pipes , companies producing Di pipes for potable water supply such as tata metaliks, Jinadal show, Srikalahasthi Pipes may get the benefits of affordable home projects… Any thoughts specially about Tata metaliks, Astral, Srikalahasthi Pipes and pipes industry as a whole, as many fund houses has shown much interest in these companies… Thanks.

Guys what will be the second order effects of this policy?

I think banks will receive a greater portion of funds that are at present saved by individuals as home loan payment… the investment cycle will boom.

The consumption will be greater from lower sections of society like labours.

Decreasing apartment prices as developers will always tend to overestimate and builder more than required in addition to the existing luxury apartments.

Other second order effects - Housing demand from middle/upper middle class too will increase due to ego/envy of seeing people below them having their own homes. This will help listed mass market players with big brands.

I think consumption at grass roots level will not increase because of affordable housing. On the contrary I think it will reduce to compensate for increased spending on EMIs. I agree with your other points.

One key question, for this segment which is mostly unorganised how does bank financing work? as in how and on what basis will HFCs approve a loan for them. I mean they have no pay slips etc. And will the rate be higher? And mortgage cover will generally be very low since the property is more likely to be situated in the outskirts where liquidity is a bug issue in case if bank action on default. What’s the haircut they do?

My point was that inorder to carry out the construction works , lots of people will be employed. They will be from the lower classes from rural areas travelling to cities for work. These people will have disposable income to spend.

They will atleast try to indunlge in some good clothing, food , fmcg products at the base entry price levels. Maybe they might even go for 2 wheelers for commute etc. So consumption in these areas might increase.

Since profit margins in affordable housing are on lower side and further, with REAR bringing in elevated working capital requirements and increasing costs further, would that mean they would have to drive even more bargain with building material makes or suppliers which will squeeze their margins further(although volumes would increase which may compensate that). Further, with RERA, since delays and frauds from builder side would decrease substantially(assumption) - would the lenders to these developers be big big beneficiaries ? because their risks will be reduced substantially and at the same time lending would also increase substantially?

The HDFC chairman reserved high praises for the current government at the Centre for its housing initiatives.

“This government’s policies on housing are practical and implementable. With the benefit of four decades of experience in this field, I can confidently say that I have never been as optimistic about the housing sector as I am currently,” Parekh said.

The government has pulled out all the stops to increase home-ownership in the country and every constituent in the housing chain has been incentivised and encouraged to play their role in the affordable housing mission, he said.

Developers in the affordable housing segment can now avail full tax deduction on profits. Further, the government has accorded infrastructure status for affordable housing to open up more avenues of lower cost, longer tenor funding. Customers can also get subventions and subsidies on home loans and can now use up to 90% of their provident fund money for housing purpose.

“No other major sector of the economy has been given such attractive incentives,” Parekh said.

Parekh also expressed his happiness about reputed builders entering the affordable housing space, but speedier approvals are needed, he argued.

Thanks Mridul - This can become a very important factor in the context of RERA - as you mentioned for LAP providing NBFCs. Also to note (currently) Land Acquisition funding is only available from NBFCs and Private Equity Funds - Banks & HFCs are prohibited there - though Mr Parekh and HFCs are lobbying hard to be granted permissions.

Working Capital for starting a project mostly comprises of costs towards obtaining Completion Certificate (CC) from Municipal Corporation. Once Project starts, the developer can count on Buyer Loans. So this is NOT a very significant cost component. And certainly not a constraint for the Big/established Developers.

The company, which last month got Rs 200 crore funding from private equity player KKR, today launched two projects — comprising 1,900 units — which will be constructed over the next four years.The projects have been launched after registering them with state regulator under the new Real Estate (Regulation and Development) Act.

With the launch of the two projects, the company has so far announced the development of 9,300 units in 9 projects — all under the Haryana affordable housing policy.

Signature Global will build 1,448 units in ‘The Millennia’ project and another 448 units in ‘Solera-2’ project. The selling price has been fixed at Rs 4,000 per sq ft of carpet area. The apartments will be sold through a draw in a price range of Rs 20-25 lakh.

“The demand for affordable housing is increasing each day. We had launched 7,405 affordable units in 7 projects and with the new launches today, we have added 1,900 more units.Now, we would be developing over 9,300 units under 9 projects,” the company’s chairman and co-founder Pradeep Aggarwal said.

The project cost is Rs 400 crore which will be funded through internal accruals and funds raised from KKR.He said the company plans to launch around 20,000 more affordable units in the future.

The headache is only till the project launch till which point of time the developer needs to bear the cost of land acquisition and approvals. Once the project is launched, RERA specifies that 70% of the collections from the buyers need to be kept in a separate account dedicated for the project to bear the cost of land acquisition, construction cost etc.

The point here is - only larger developers will have the capability to carry the upfront costs without any inflows given the land acquisition costs are pretty high in tier 1 cities (infact land cost might be the single largest cost component). Most of the funding raised by the real estate players is to cover the land acquistion and approval costs.

Just to clarify: CC denotes commencement certificate i.e. the approval to start construction.

Affordable housing is great. Why is the Euphoria now ? Because PMAY incentive of 3000 crs.

My Qs is will it be enough to sustain the euphoria ? Ultimately we need end consumers to buy this. Are the end consumers solvent enough to ride this euphoria ?

Is 3000 crs enough to support this euphoria ?

There is an article in today’s Business Standard that also support that Yes, there is an euphoria and a significant number of players want to enter this market

National Housing Bank (NHB), the apex financial institution for the segment, has got six applications in the past six months from entities for starting a new housing finance company. Those applying include the Piramal Group, JM Financial and Hero Group. This is in addition to 11 approvals that it gave in the past 12 months.

One more it received last year is under consideration. What is interestingly is that most of these newcomers are targeting home loans of Rs 10-15 lakh. Clearly indicating an impending boom in the affordable housing segment.

“New entrants are clearly excited by the government addressing the supply and demand-side constraints,” says Sudhin Choksey, MD, Gruh Finance. Affordable housing has been a part of the ruling Bharatiya Janata Party’s election manifesto. The rise in new HFCs started with the government coming to power three years ago. About 30 new ones have come in this period, taking the total number to 85. “These new entrants are also making a natural progression to an HFC from an NBFC (non-bank finance company), seeing a larger opportunity,” says Choksey.

The progress in implementing PMAY has been limited so far. However, the pace has started to pick up. NHB has signed memoranda of association with 34 states and Union Territories; at least 700,000 housing units have been sanctioned across states. The infrastructure status awarded to affordable housing in this year’s Union Budget is likely to support supply creation.

“The rush for opening of HFCs indicate the impending boom in affordable housing,” says Sriram Mahadevan, business head at Happinest, the affordable housing project from Mahindra Lifespaces. “To see the real surge under PMAY, one will have to wait till the year end.” Mahadevan himself is waiting for approval to launch a project at Palghar that will have a majority of houses under Rs 20 lakh each. “”

Precisely! Initial amount is required in bank for project approval. Once they have the approval, they will launch the project and get do advance bookings, the fund from which will go to escrow, which can be used by the developers for that specific project construction. There are going to be checks as to how and in what phases the escrow fund can be utilized.

These regulations are actually going to help larger, stable, reputed players as competition from small, fringe players will drastically come down due to this initial fund requirement. Also, builders with good reputation will be able to book the project earlier in order to actually fund the construction. Players that lack public trust will find the going very difficult going forward.

What now need to be seen is the margins these larger players can reap from this segment. Volumes are definitely picking up and so will be the competition in this segment among established players. Good way to play this theme is financiers like Indiabulls housing finance (which has a very established construction finance and LAP portfolio), Piramal (which has entered construction finance recently and is doing very well. Housing finance segment will get saturated soon in my opinion as there are no entry barriers and everyone is extremely aggressive about it. Only those with access to funds at lowest rates in the market, with best cost to income, good branch network and reach, and technological superiority will have a long runway in housing finance segment.

Just attaching one press release from IB Housing post demonetization where they have spoken clearly as to how they are going to benefit from the event.

Investors were wary of their LAP and construction finance portfolio, but with the advent of RERA and this demonetization event, their LAP segment and construction finance is going to do very well.