When Buybak is less than 10% of market cap and promoter is participating through tender offer route, I consider that as tax efficient quasi dividend and ignore buyback price as any signal to valuation. This is tax efficient way to return money to owners particularly, promoter which I believe are in highest marginal tax rate bracket. This my view and may be wrong.

Discl: No investment in Aarti Drugs

9 Likes

Disclosure: This is one among my Buy & Hold stocks…holding these stocks for the last 4 years…and added on dips… I am happy with the overall return it has given me so far in whatever form it may be. My capital grown by 5 times.

My rationale for investment.

(1) I have not come across any corporate governance issue to the best of my knowledge.

(2) Good product range -import substitute API

(3) Selected under PLI scheme …mainly capex plans …through internal accruals.

(4) Not depending upon USA so far … .so no USFDA issues- most of its its exports to ROW…

(5) 60% promoter holdings with no share pledging gives me confidence to buy and hold for further gains !

Anyway , not married to the stock…if I find any change in business climate in this company and I spot a better opportunity…will move away…and I may or may not be able inform this forum.

4 Likes

Is anybody aware of aarti drugs plans on peptides or any management commentary on it. Looks like peptides API are favored increasingly for oncology, diabetes and more to come.

1 Like

Is the buyback shareholder friendly?

• Buyback are generally shareholder friendly for the existing shareholders because the reduction in the outstanding shares increases the company’s return on equity.

• But in the case of Aarti Drugs, the buyback price of Rs 1000 is favoring the exiting shareholder rather than the existing shareholder.

• On 20 March 2020, the price was Rs 122. Buyback at that price would have been friendly to the existing shareholder.

1 Like

021b9e6c-750d-4ed7-b76b-131b4e75c219.pdf (bseindia.com)

Q4 results from Aarti Drugs

The raw material inflation looks steep. Will have to look out for the management commentary on the same and weather they have hiked prices to offset it in Q1. Waiting for the concall to be avlb

Dis : invested

2 Likes

Sept 2021 results https://www.bseindia.com/xml-data/corpfiling/AttachHis/5a908dbf-ff0a-483d-9f8b-b83389f62758.pdf

Any one done estimates of FY 23 earnings based on new capex and guidance of management?

stock is 40% down from highs over 1 year.

2 Likes

its 60% down now. definitely the raw material cost and hence margin is be one of reason. any experienced boarder to help in details?

technically the next support is around 150?? fundamentally we would not see any tailwind unless rm cost stablize or capex driven incremental revenue kicks in

2 Likes

Notes from AR - Aarti Drugs, FY 21-22-

- Established in 1984. A significant part of Aarti group specialising in APIs, Speciality chemicals, Intermediates and Formulations with Pinnacle Life Sciences as its fully owned subsidiary. Has state of the art manufacturing plants in HP, Maharashtra and Gujarat. Has a total of 12 manufacturing plants with an installed capacity of 49000 MT. Also has 02 R&D facilities - both in Maharashtra.

- Aarti drugs is the largest manufacturer of following drugs in the world -

Fluoroquinolones group like - Ciprofloxacin, Levofloxacin, Ofloxacin etc ( all anti biotics )

Tinidazole ( anti protozoals )

Celecoxib ( NSAID )

Nimesulide ( NSAID )

Metronidazole Benzoate ( anti biotic )

One of the Leading producer of Metformin

Ketoconazole ( anti fungal )

- Produces a total of 50+ APIs. 37% of revenues is from exports. Out of a total of 12 facilities, 10 are dedicated API facilities. Brownfield expansion of Tarapur Speciality Chemicals facility is complete and scale up batches have started from May 22. Production is likely to be scaled up by end FY 23

- Last 5 Yrs financials -

Sales - 1245, 1563, 1808, 2159, 2500 cr

EBITDA - 200, 210, 263, 442, 341 cr

EBITDA margins - 16 pc, 13.5 pc, 14.5 pc, 20 pc, 14 pc

PAT - 82, 90, 141, 280, 205 cr

Debt to equity - 1.19,0.89, 0.58, 0.38, 0.52

ROE - 16.3, 16.7, 20.6, 35.8, 21.1

Management agrees that China + 1 factor is playing out to their advantage in the API sector.

- Current Sales break down -

APIs - 80 pc

Formulations - 11 pc

Intermediates - 5 pc

Spl Chems - 4 pc - Capex spending for FY 21-22 stood at 152 cr. For this year, Capex plans are to the tune of 250-350 cr. For FY 21-22 API volumes increased 10 pc owing to strong growth in chronic therapies due fresh commissioning of anti-diabetic capacity and ongoing expansions. Speciality chemicals and Intermediates also grew by 28 pc each. Over next 5 yrs, company intends to spend 600 cr on Capex. This expansion will encompass backward integration for APIs and formulations to reduce costs. Product wise capex plan for next 5 yrs -

Anti - diabetics - Aim to be the largest Metformin player in the World. Aim to launch Gliptins to further strengthen this therapeutic category.

Fluoroquinolones - further 40 pc brownfield expansion for these anti-biotics.

Ant-Protozoals - Further consolidate leadership in Indian Mkt with existing tech and Chinese JV. Plans to further backward integrate and apply for PLI

Vitamins/ Anti-Inflammatory - Multi purpose facility under construction.

Cardiovascular - Aim to double the existing capacity.

Anti-fungal - Further consolidate world wide leadership.

Speciality Chemicals - Incremental expansion of multi purpose chloro-sulphonation line in existing block

Disc : invested, biased.

3 Likes

Metformin API is manufactured by Aarti, IOL & Granules. Ami organics is also into API manufacturing. In API manufacturing there is very little differentiation except each of them manufacturing different products where growth will take place depending on demand from final product. As a retail investor I look for what is unique among these players and I cannot find one. A China +1 strategy and import substitution by domestic players may offer some tailwind. Other than that I don’t see any exponential growth for these 4 API manufacturers. This is my view. Any other thought?

DISC: Not invested, actively monitoring API manufacturers

2 Likes

As per my assessment, Aarti drug does well only when Govt gives support in terms of import restriction for some of its drugs.

Almost all API makers in India depend upon China for KRM (key raw materials) and most pharmaceutical companies depend upon China for either API or Key raw material to a varied degree which none of these companies are transparent in declaring the import content.

So the fortune of our indian pharma co and API players depends upon the (1) Chinese companies who detect terms and also (2) Geo political situation.

Our Govt has recently started PLI schemes and it would take time to see the results. However we still have a long way to go to catch up with China in terms of Cost.

China has spent a lot of money in R&D, time and efforts in building a very good infrastructure for pharma/ API over the years to reach the Global leadership with a competitive edge which would be tough to replicate by any nation.

Discl: Booked profit and Exited all API , pharma except Divi and Gland.

This is not an investment advice. Please do your own assessment before investing

5 Likes

Are you guys still tracking this company? Today Stock is up 16% in this market, not able to find the reason behind it.

And also please suggest some source where anti dumping duty on any product can be tracked.

Thanks

1 Like

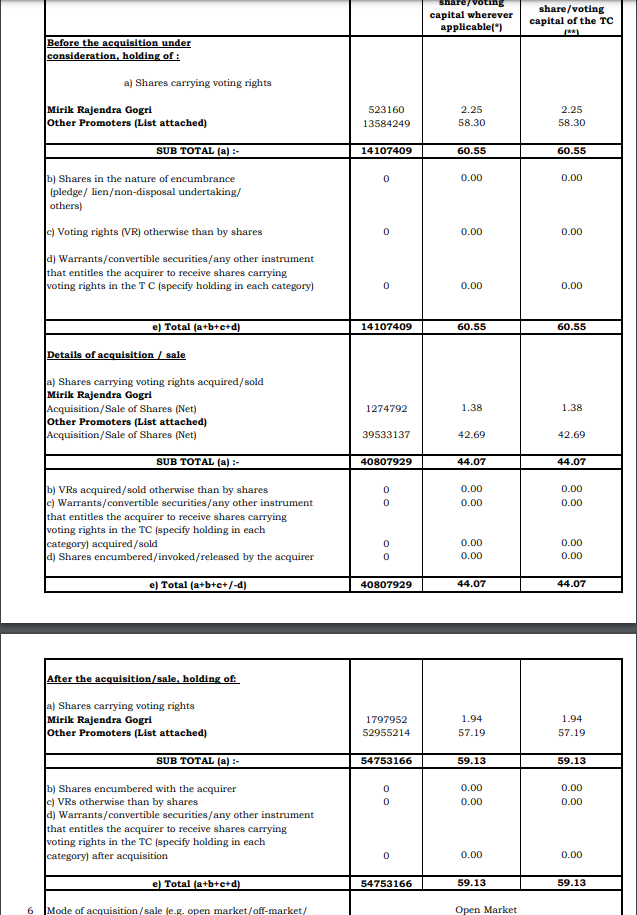

There was an insider action in the company, the disclose is attached below

In my judgement they have messed up the numbers in the disclosure. For example

Mr. Mirik Gogri hold 2.25% before action and the action he did was of 1.38% so finally he has acquired the shares he should hold 3.68% or if he has gifted/sold or any other way parted with the shares he should have 0.87% where in disclosure his final holding is shown as 1.94%.

The other case may be my understanding is wrong in which I will be obliged if any one takes time to correct me. Thanks in advance.

1 Like

Buyback Alert !!!

| Buyback Type: | Tender Offer |

|---|---|

| Buyback Record Date: | Aug 04 2023 |

| Buyback Offer Amount: | ₹ 59.85 Cr. |

| Date of Board Meeting approving the proposal: | Jul 21 2023 |

| Date of Public Announcement: | Jul 21 2023 |

| Buyback Offer Size: | 0.72% |

| Buyback Number of Shares: | 6,65,000 |

| Price Type: | Tender Offer |

| FV: | 10 |

| Buyback Price: | ₹ 900 Per Equity Share |

can someone share the details of the acceptance ratio of buy back which was done in 2021??

The acceptance ratio for the 2021 Aarti Drugs buyback was 33%. This means that for every 100 shares tendered for buyback, only 33 shares were accepted. The buyback price was ₹1,000 per share.

1 Like

AARTI Drugs Q1 FY24 Result Update:

Future Outlook:

- The company expects to achieve a topline growth of ~10% in FY24, primarily backed by volumes.

- It would target to achieve an EBITDA margin of ~14.5%-15% in FY24 and the same is expected to improve further in FY25 with the commissioning of additional capacities.

- Most of the API players reported a volume uptick, backed by improved demand and stable realisations. Keeping this in view, we expect demand for API to continue in the upcoming quarters easing supply chain bottlenecks. We believe that Aarti Drugs, being a leader in the domestic industry, is well-placed to capitalize on prevalent as well as future growth opportunities.

1 Like

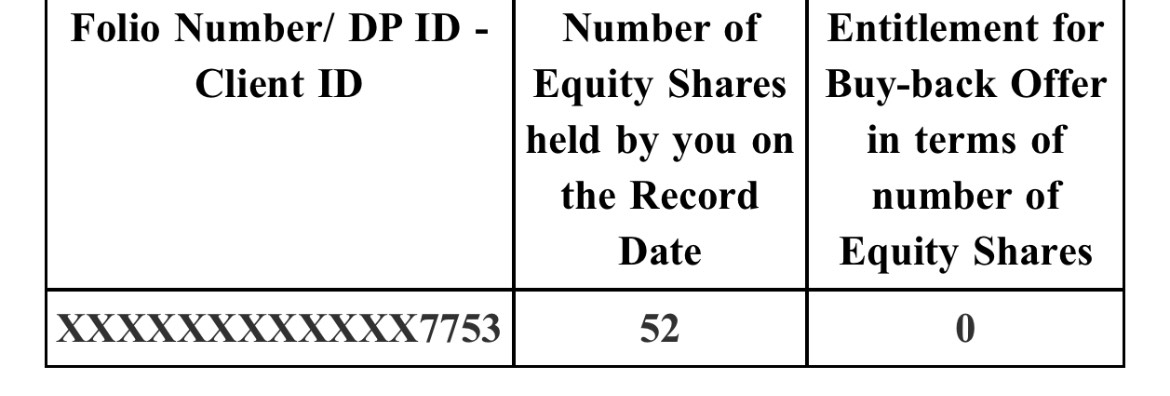

Hi ,

Today I received email from Aarti drugs and no shares are entitled for buyback. Is it a mistake or I would like to know the reason.

Please find below snapshot for your reference.

Any idea?? Is it the same for you??

Read this, - https://www.bseindia.com/xml-data/corpfiling/AttachLive/7eaad7c6-6d75-4d02-bd1a-b35948de8beb.pdf

Read point number 19.5

"Reserved category for Small Shareholders :- 2 Equity Shares out of every 157 Equity Shares held on the Record Date.* "

You fell short of some shares so there is no entitlement in your case. You can still submit your shares in the buyback but there is no guarantee that your shares will be accepted. Read point 19.7 to understand it better.

4 Likes