Ok. Since I am feeling a little bit for those who are even mildly suffering right now during the drop in mid and small cap prices, Here is a post with examples from the book “The Intelligent Investor” on what to do as explained by the legendary Benjamin Graham. I am just pasting small parts of it here so you can be introduced to the book that made Warren Buffett a billionaire. I am sure if you told someone, can you read 500 pages and it can make you a millionaire at least, they would read it right? What about you?

First, I barely know anything and I am truly a novice at this game. But sharing what I read cannot hurt, and may even help so why not. Here it is.

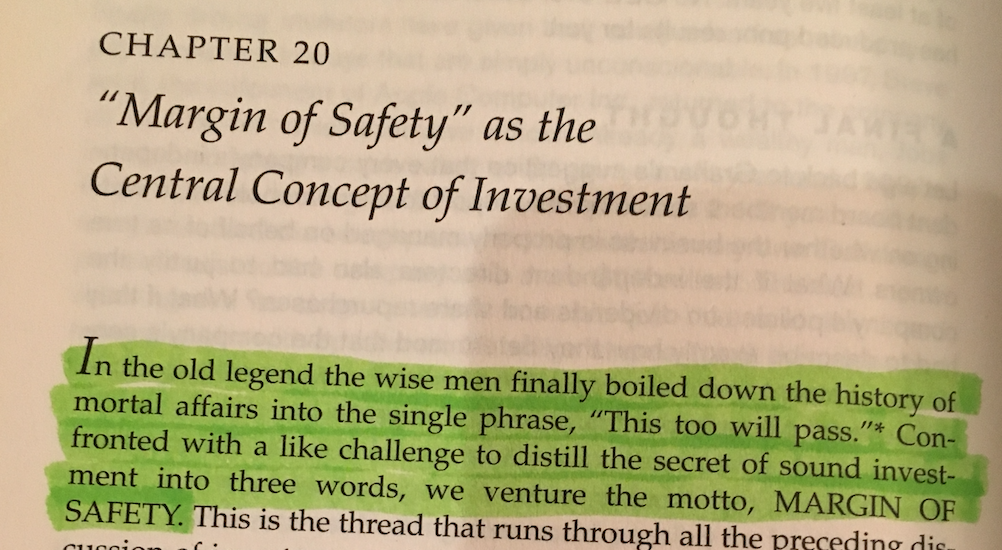

Lesson 1

My interpretation: Do not buy or pay for growth. A certain amount of growth should be an essence of a business anyway. Buy it with a margin of safety.

Lesson 2

My interpretation: If your margin of safety is large enough, you do not even need to predict the future course of the business, you can be rest assured that you may not lose much if business does not grow as expected.

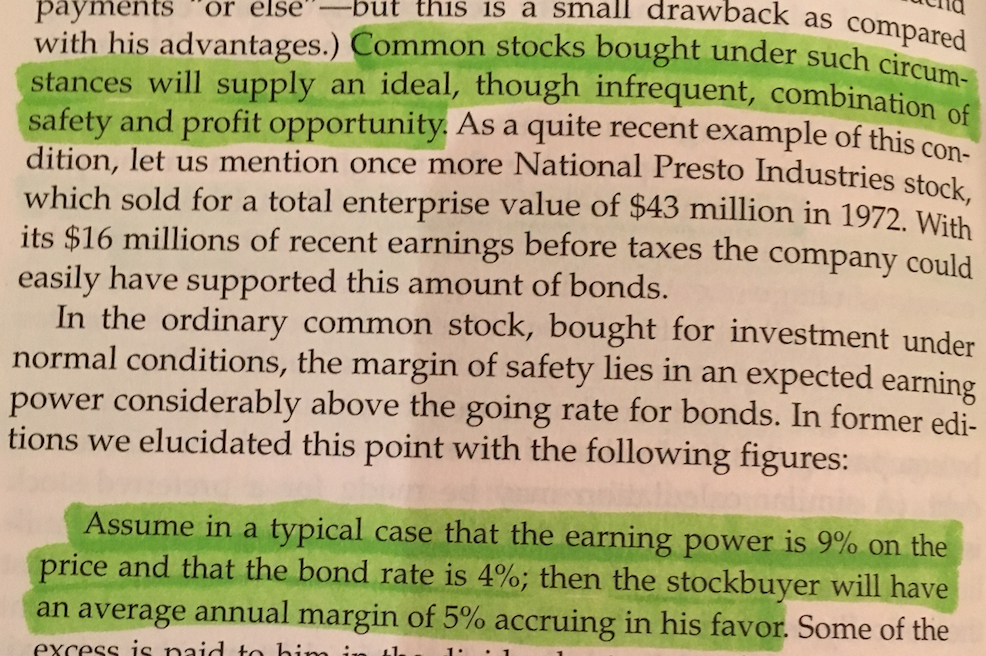

Lesson 3

My interpretation: To buy under the concept of margin of safety, we will have to wait for infrequent times when these opportunities present themselves, but the results from these operations of patience and action when presented with such opportunities should provide ideal results.

Lesson 4

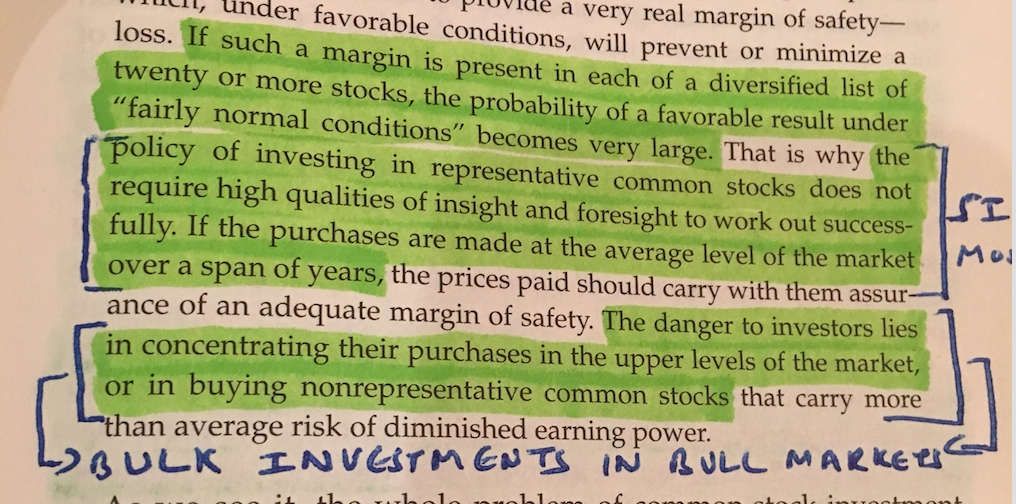

My interpretation: Here Benjamin is saying, if you have identified the difference between a good company and a not so good company… good being for example HDFC Bank, HUL, ITC, Nestle and the likes, simply equal amount weighted SIP into them for a number of years, and security analysis then does not require deep study nor deep insight into companies.

The danger in in either a. buying in large quantities (bulk investments) even good companies when stock markets are relatively high, or buying easily replaceable small cap businesses in bull markets which all seem to have a moat when a bull is running.

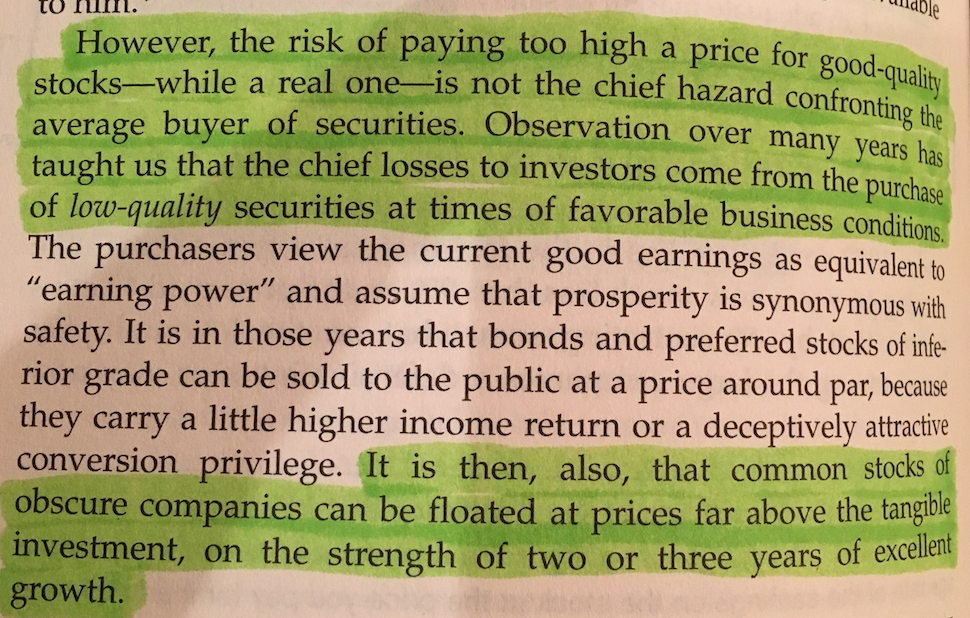

Lesson 5

My interpretation: Don’t project bright futures and don’t buy into small enterprises especially in bull markets. You might have pain but escape after a spanking for a few years in established and large businesses, but if you are in low quality securities in a bull market, you may not recover.

Lesson 6

Continued… next page

My interpretation: Basically here, Graham does give credence to growth investing as a strategy but even then insists on a margin of safety for small enterprises, for example a company growing at 50% and available at 5 PE. If the company falters, you may not lose much.

Lesson 7

My interpretation: The same small enterprise which may have been bid up like crazy in a bull market and then crashes in price may be a good investment at a moderate 5 odd PE if still growing at 40-50%.

Lesson 8

Continued… next page

My interpretation: To sum it up, Graham says clearly, how he finds it amazing that even business people who would not pay such valuations in their private business affairs get caught up and pay high valuations in the stock market. He says, treat each investment as if you are investing in a business.

The second and more positive page explains that when these low prices do come around, then be courageous and not fearful and let me be clear, don’t decide by looking at the stock price  Like right now. What has fallen 40 percent can fall another 40% dudes… and missuses.

Like right now. What has fallen 40 percent can fall another 40% dudes… and missuses.

In short, last year no one would have bothered with this book. My point for highlighting some points here is: Please spend the 300 or 400 Rupees to buy this book. Read it and try to understand it. Even if a small player, you are probably playing with lacs. Take some time off and read this book. Stock markets will not run away and then come back to invest. We all want to make money, very few want to put in the work required for it. There are great ways in the book with which to identify bargain stocks. You will not believe it, but there are some such large caps even now in the Indian stock market. This book if fully read, will make valuations for you much easier; since you need only an approximation of value and not a precise number, you can, and will do better.

Let your investment fundamentals not be that liquidity will come via sip’s so stocks will go up. That does not end well.