Can you please specify the source from where you obtained the above snapshot/calculations? In your snapshot, Net Profit (23.09 Cr) is not getting added up in any of the calculations (“starting from Op Profit from WC changes” till CFO)

Cash flow of 8kmiles was a mystery for many ! The numbers don’t add up in some sources. You can see people commenting on that topic quite often here .

I didn’t really understand the Capex for intangibles part of the query. However if you are talking about the acquisitions, most of the recent ones have been through internal accruals and partial debts .(Debts again which have been very quickly serviced)

The management doesn’t look unscrupulous as of now ( The new ones Suresh Venkatachari and team- The old promoters are big time fraudsters even banned by SEBI for dishonest practices like artificial price jacking). Just a gut feeling , i don’t know them yet but they have a decent background in past ventures

Disl: Invested ,made good profits, exited, trying to time the entry point again

This might be interesting. I recently chanced upon a thread on a popular US Visa forum - immihelp.com - where they are discussing genuine consultants who can help them move to the US by filing a H1B visa.

Interestingly, I came across the name 8k miles there

Even their head of HR was pitching to deposit money. I am really not sure how legal this is.

Quote Originally Posted by viv View Post

I too got a call from same company 8K-Miles for H1B sponsorship. They are asking for the deposit etc. I had a telephonic discussion with them and as usual its sounds all good.

They are stock listed company.

To me it all look good except the security deposit part.

[what i have learnt from reading several post on different website is that if anyone asking for security deposit that too before filing visa, then chances of getting money back is diificult if visa rejected/denied due to any reason] @srikanth - if possible u can share with me ur email/contact so that we can discuss further and comapre the info they share with us.

it would be great if anyone can share there experiences with them.

Hi Sri & Viv,

I too got a mail from 8k miles company last 2 weeks before. I talked with them and need to pay security deposit 2Lakhs to his account(8k miles a\c HDFC). He sent a\c details through mail. I asked about process and money return details, if i am not selected ( rejected or denied) they will refund full money they “told like” this and i conacted the local address(chennai) and asked few details about this H1B process.

Please let me know if you have anymore information about this company?.

Note: I searched all websites related H1B and it is looking good only… but i confused to go further…

Praveenballa: It is completely illegal to collect money from consultants for visa filing. Sooner or later they would be caught and end up paying huge fines.hope ppl did not forget INFY fiasco reg visa fines so soon:)

Hi All,

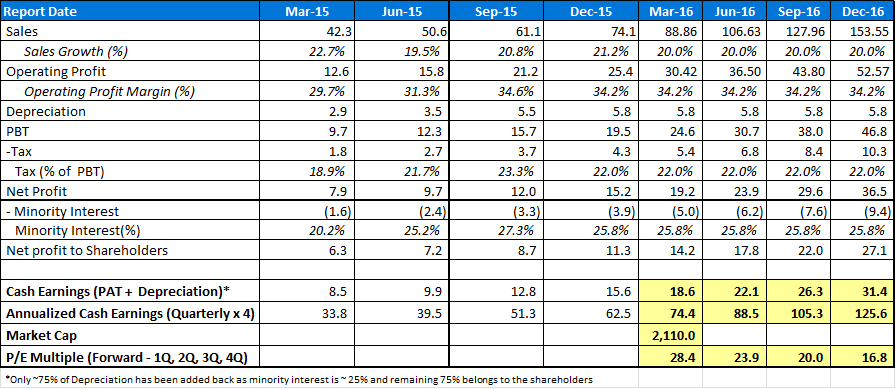

It seemed in the starting that 8K Miles is trading at insanely high PEs. So decided to do some projections and analysis and believe that it is fairly priced (and probably undervalued as well). Attaching the sanpshot of the same (source: screener, BSE). Mar-16 to Dec-16 are P&L projections assuming same growth rate and margin profile for the next 4 quarters. Would like to hear views from other members as well on the same.

Current Quarterly-PAT is Rs. 11 Cr which adjusted for Dep is Rs.15 Cr making the annualized Cash PAT = Rs. 62 Cr (Cash PAT is a better indicator for valuing software companies rather than accounting PAT)

This implies, with current Market Cap of Rs. 2,110 Cr, 8K Miles is trading at ~ 33 P/E multiple = 2110/62 (even if we assume the growth rate to be zero going forward)

Now, a high growth company will always appear overvalued if trailing or current earnings are used to evaluate P/E multiples. So taking a 1 year forward annualized Cash Earning multiple, 8K Miles seem to be trading at P/E of 16 X

Looking at it from a different view point, company will be trading at ~Rs. 3,800 Cr in an year

a) if company is able to sustain its current growth rate for the next 4 quarters (20% Q-o-Q) and

b) if current margins are maintained for the next 4 quarters, and

c) if valued at 30 P/E at that time

Now question is:

a) why 8K Miles will be able to maintain 20% Q-o-Q growth rate ? What if it doesn’t ?

- 8K Miles has demonstrated the same consistently in the past because of

i) Promoter (Suresh) has mentioned in interviews that they are now working on 3-5 year long projects with enterprises which can extend to a decade as well (managed services business model)

ii) They have cloud platforms/products (Identity Access Management, EzRx) which are more or less a recurring revenue model SAAS model - this is where they edge over other cloud companies (e.g. Cambridge Technology model) which are mainly into project/orderbook kind of business or, at best, managed services

- Product Expansion: It is expanding into financial services now for additional growth apart from its strong hold - pharma/healthcare

- Geographic Expansion: it is expanding now to Europe as well.

- Inorganic Expansion is an area that company has explored successfully in the past

Even if company slows down to 15% or 10% Q-o-Q growth in an year, there is very limited downside as per calculations.

b) Maintaining margins: Mr.Suresh Venkatachari (CEO) is confident of maintaining margins - in fact, in multiple interviews, he has explained as to why operating margins will increase going forward. 8K Miles is slowly moving into recurring/subscription/SAAS revenue stream (long tem) and moving away from orderbook/project based revenues. He expects the break-up to be 70% (subscription/long term revenue) : 30% (orderbook/short term revenue) in the near future. And hence, he mentions in the interview that profits will grow non-linearly because additional revenues will cause less than proportionate expenses going forward. This makes sense since their Cloud IAM, Cloud EzRx prducts seem to be successful (after their 2013 launch of Cloud IAM product, their quarterly revenue has not gone down even once which shows the strength)

Sharing one interview:

now the question remains, whether the market continues to apply current 30 x P/E on this stock in the next one-two year or not.

Most of the listed companies don’t even achieve the yearly growth which 8K Miles is achieving quarterly (20% Q-o-Q). There are probably not more than 20 companies out of a full universe of 5000+ listed companies which are achieving a Q-o-Q growth rate of 20%.

Further, There are very few high quality companies which can command an EBITDA margin of 35% and expect it to improve going forward.

Inorganic growth being supported by internal accrual is a huge testimony to the earnings quality

On a sensitivity analysis and conservative basis, even if revenue growth gets lower , margins remain constant and market doesn’t value it at a lower multiple than 30, downside seems to be pretty limited.

@peguy: found your analysis quite interesting. But I believe comparing Kellton (or any other IT stock) with 8K Miles on the basis of Price/Sales ratio is not useful. Reason being, Kellton’ s operating margins (not more than 15% so far) are far lower than 8K Miles (35%) and at the end, earnings is what matters in valuing stocks (apart from other factors, of course). Sales multiple analysis would have made more sense if business segment, margin profile and growth expectations of these two stocks were same.

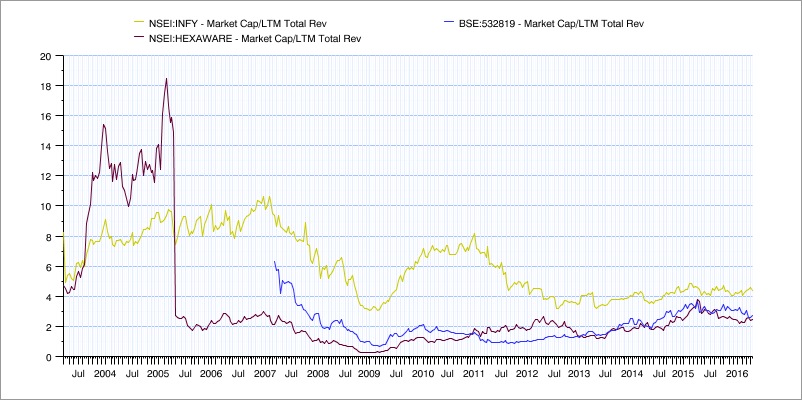

Fair point, ultimately any company needs to be valued on the basis of its earnings. However early stage companies and companies which are investing heavily in sales and marketing for future growth, do get valued on a revenue multiple basis. You would never value Mindtree or Hexaware on a revenue multiple, but these young companies (8k miles and Kellton) are valued for their growth and no their cash flow yield and hence the preference for looking at revenue multiples. There is too much noise in the cost data to compare 2 companies at this stage. If you looked at cost structure of Mindtree and Hexaware you will see a lot of stability unlike these companies.

Anyway, to your analysis in above post, I don’t disagree that there is a case where 8k miles could be a good investment, however it is a low probability case given fundamental issues in business models. Phrases that the management uses like SaaS, managed services etc contribute almost nothing to revenues today.

At current price, this stock needs absolutely everything to go perfectly (continued hyper growth, rising margins and a super high P/E multiple when you exit) for it to generate 20%+ returns for you. I don’t think that is a realistic case to bet on. I am pasting below the Mcap / trailing 12 month revenue chart of Hexaware, Mindtree and Infosys to underline the point on multiple compression as growth slows down.

It would be interesting to understand if they are into bodyshopping (Sending someone to US to work at clients place on any tech/project/program) or if these are guys are being asked to work for implementation of their own products/projects. Would you know?

Current Runrate looks like they will hit 100 cr NP this year (23.6 in current Q) - Post split market cap is around 2200 cr - Company growing at 100% YoY available at a PE of 22 is not believable…

Revenue grew by 19Cr between June and Sep quarters (122cr vs 103 cr).

Receivables has gone up to 118Cr - 90 Days receivables is more like the norm in IT industry and not a cause for concern. Employee costs are at 63 Cr for the Q - Current assets and cash seem adequate to cover the costs - Hence no need for debt and the balance sheet is looking clean.

What does the market know that I do not know? Why is it cheap?

[Disclosure : Invested - Might buy or sell more without further disclosures.]