@siddharthadhamankar

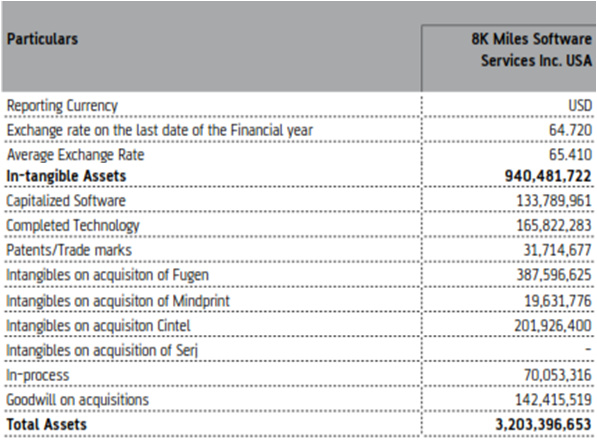

Are you talking about 8K Miles Software Services Inc, USA (henceforth 8K Miles US)? This was a new company that appears in FY 2010 statements. Page 40 of AR 2010 gives the details as 1000 shares for 100% holding bought by 8K India for a total consideration ₹ 45,220. This includes cash / non-cash etc. There is no mention of IPs acquired in the annual report against this purchase either in Director’s report or in account statements, or notes to accounts.

Ok, maybe. I have founded & owned start-ups in tech with US subsidiaries; done some deals and signed on audited accounts like the MD of 8K Miles India. That should count, I hope  .

.

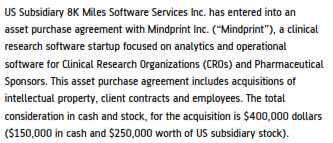

By Promoter you mean 8K Miles US? There is no such mention in the AR 2014 from where I made my original claim. Neither in Director’s Report / MDA nor in accounts as a transaction. Can you share your source?

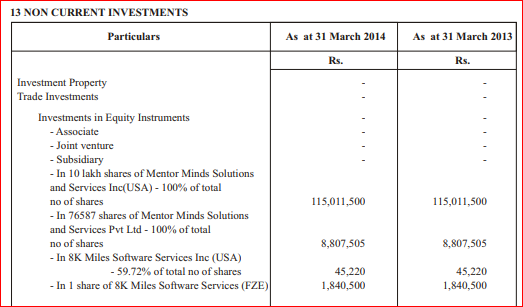

There is however something amiss about this part (dropping from 100% to 59.72%) in AR 2014 and I post the extract below.

Here you see that the ownership of 8K Miles US is shown as 59.72% in FY 14 and FY 13. The total number of shares in not mentioned!

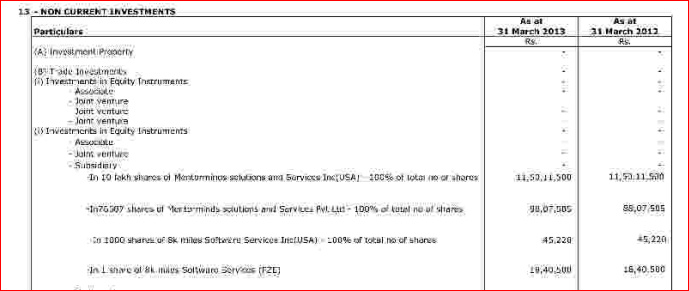

However in AR 2013 this is what was shown:

I.e. 1000 shares constituting 100% of 8K Miles US shares was held at March 31, 2013 as per AR 2013 and the same is shown as 59.72% at March 31, 2013 as per AR 2014! Both can’t be simultaneously true! Besides, number of shares is not mentioned in AR 2014. Neither I nor any self respecting auditor will risk, signing on such accounts…unless something is worth the risk for the signatories. (The above is difficult to read but I have reproduced the Annual Report exactly as is, sourced from 8K Miles India website.)

To re-confirm before I respond, you are talking 8K Miles US valuation, not 8K miles India, right?

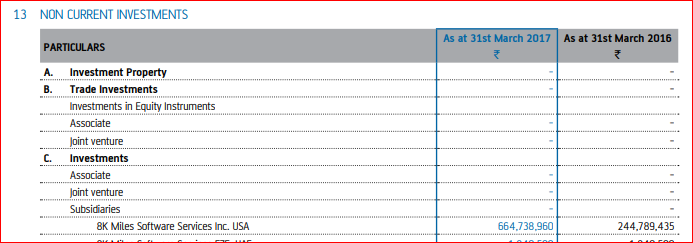

In AR 2017, 8K Miles India increases its stake in 8K Miles US by 1%, and the increase in cost of investments is Rs 42 crores (extract below). Thus 8K Miles India has valued 8K Miles US at Rs 4,200 crores or about $ 600 million (from $ 1000 just 3 years ago in FY 14) and that begs a WOW.

Sure. We are both doing conditional probabilities. Your P (A/B) probably is probability of a justifiable explanation (A) given what is shown is true and honest (B). My P(A/B) is an attempt at probability of true and honest representation (A) given certain ‘facts’ in the annual report (B). My P(A/B) is tending to the middle of the number line!

How can you be sure that what they file in the US is what they show here in the Annual Report?

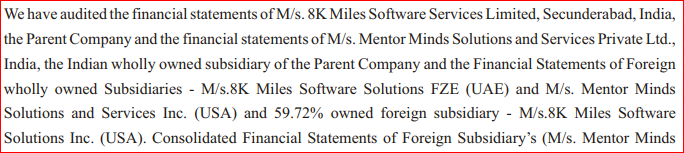

Just to add some more to the farce that is presented as the Annual Report, let me pull out another extract of the auditor’s report from AR 2014 (page 73).

It says that this auditor (GHG Associates) has audited 8K Miles US!!! An India domiciled audit firm auditing a US domiciled entity!

I suggest you read the enforcement actions of SEC that can be found here to know how many go to jail, on a weekly basis - SEC enforcement news

I suggest you read the enforcement actions of SEC that can be found here to know how many go to jail, on a weekly basis - SEC enforcement news

P.S: All information sourced from Annual Reports posted at this URL https://8kmiles.com/investors/annual-report/ as of 8:30 am IST, today 01 Aug 2018.