Company has sent a note to exchanges mentioning that they will be publishing “Standalone” results on 30th May. While the “Consolidated” results will be out only by 22nd June.

This is a bit upsetting … personally. I dont like it when companies dont publish their results on time. Maybe we need to live with these things when it comes to small cap companies.

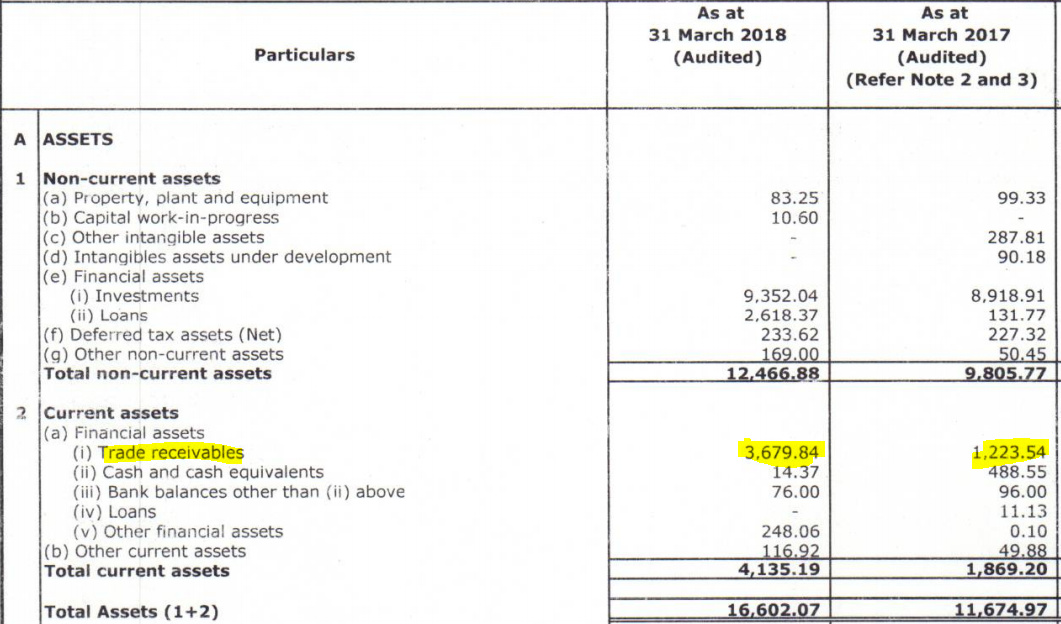

Though these are standalone no. only but their is again a v high increase in trade receivables (YOY) as compared to revenue. Can we see the same trend in consolidated no.s also ? Such a high receivables raise questions on sales authenticity and growth.

I am not making any allegation. I am doubtful if the sales are genuine. Check the balance sheet and P&L statement of yesterday. Receivables have increased thrice YOY but sales are not even doubled, That means forget collecting old receivables , even more revenue is not collected this year. Now quiet possible that sales are genuine and they may receive cash flows in future but increasing receivables at such a high rates is alarming.

The auditors for 8k only audit the standalone business. The problem I have had with 8k was the overseas subsidiary which have a bulk of the business. The Indian auditor can quite easily wash their hands off if there is any trouble in the future.

Disc: I couldn’t believe 8k miles’s numbers one bit and so I have avoided it in the past.

I couldn’t believe the topline growth. Standalone business is clocking 40 Cr topline while consolidated is doing 800 Cr levels. Sales Growth last 3 yrs is a staggering 130% CAGR. I find it quite unbelievable having worked in this sector. This sector (cloud migration) doesn’t get repeat businesses and there isn’t much customer stickiness. You have to start all over again and Customer acquisition costs are quite high and margins have dropped drastically in recent years with automation tools. None of these reflect in 8k miles numbers as they continue to post 34% OPM. This is very, very hard for me to believe, along with the sales growth.

Then there is problem with cash-flow. Why isn’t the company throwing out cash? It is FCF negative for last 5 yrs. Why isn’t it paying higher dividends?

As for “Digital” segment - This is just marketing speak for a set of services (Salesforce, digital marketing, supply-chain management, web apis etc.) we have been offering for many years before this term came into existence. Infosys and TCS have very much been doing all these for well over a decade. I cringe every time I hear the term “Digital” in the media. I guess its their way of saying that they are somehow transforming themselves when in reality this change is slow and steady and has been happening for many years but has just got a fancy moniker to feed the media and analysts.

I 100% agree with what you said about dividend. They should be paying more dividend if they are generating so much cash. But then companies that are in growth mode don’t pay dividends.

Though, difference between standalone and consolidate revenue should not be surprising as lot of their revenue growth also came from their acquisitions.

High growth can be accounted in part to these acquisitions.

While most of the allegations cannot be substantiated unless the auditors raise a red flag, what upset me the most of them not publishing the consolidated results on time. They gave “moving to the new accounting standard” as a reason but I am not qualified enough analyze if moving to the new standard warrants the delay.

I agree. I also read in the above posts, on top of the cloud migration, promoters are doing some totally irrelevant work in media and movies! I do not see a reason to diversify and spend effort on something totally irrelevant if the underlying business is as lucrative and strong as the numbers suggest.

I found this company at 379 last year and placed a small bet. The management came out with lot of analyst calls after that the price reached new highs.

After looking at how the story is unraveling with - Vakrangee, Manpasand, PC Jewellers; I can sadly admit that the similarities are uncanny.

@naruto

Can you please elaborate on the similarities that you see with Vakrangee, Manpasand, PCJewellers. Would be good for everyone to be aware of the same. Thanks.

Phenomenal QoQ growth (this is the parallel I drew with companies earlier) with US subsidiaries contributing majority of the revenue

The contribution from US subsidiaries cannot be verified v. thoroughly by auditors

Growing Trade receivables pointed out in thread earlier YoY 970.97 -> 1223.54 -> 3679.84 L

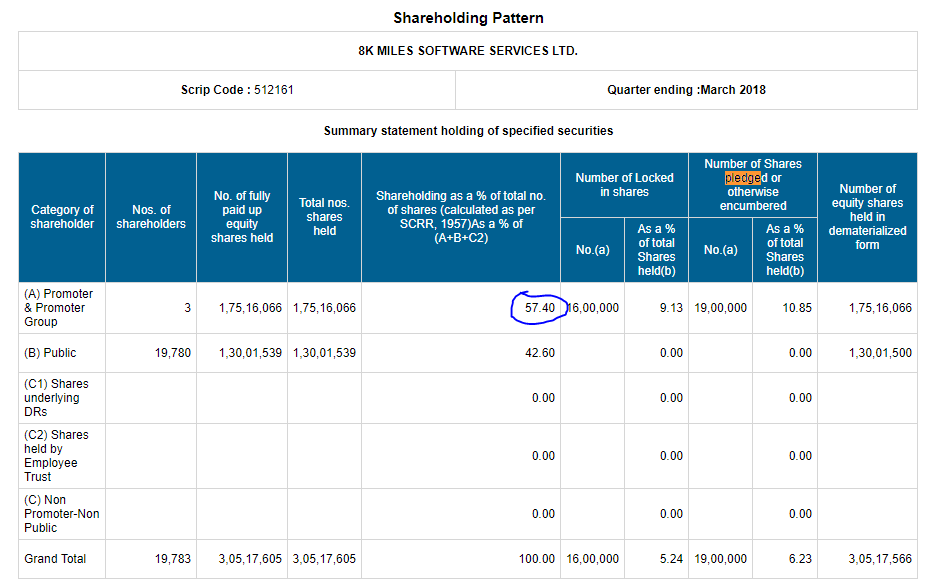

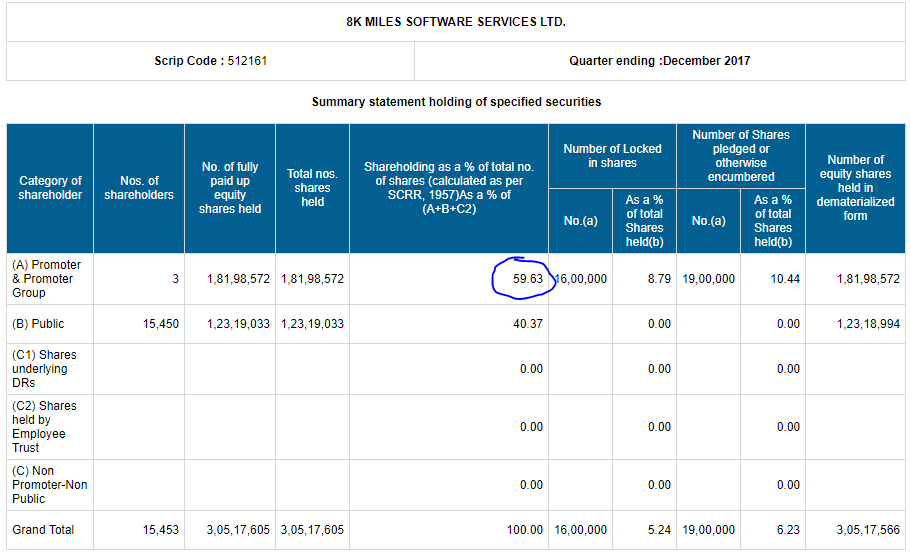

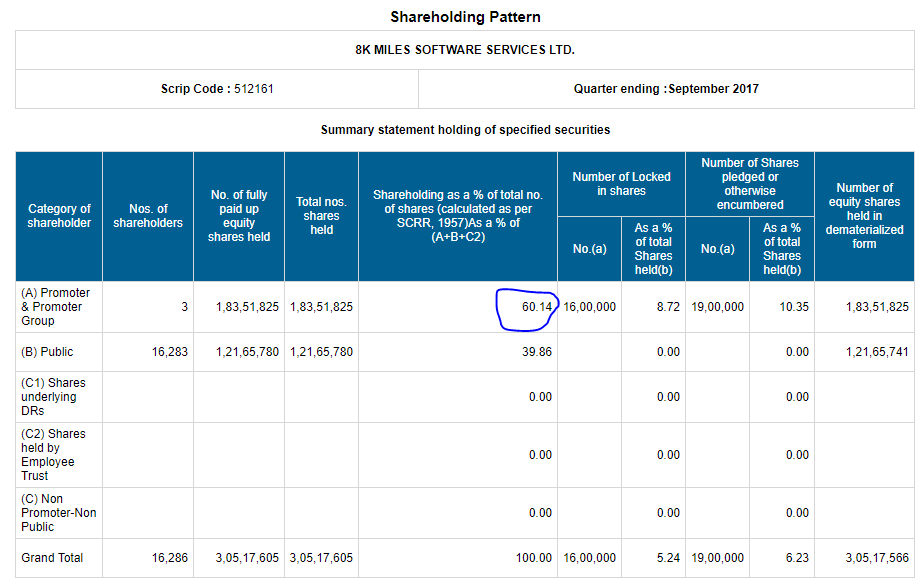

Promoter selling - Ramani and MV Bhaskar. For a company with phenomenal growth like this, If I am the promoter and have an insider view of how the company is growing YoY, I would stay invested in it.

In Standalone FY17-18, In the Annual period ending Mar-18, “Other expenses” are ~50% of Total Expenses. For a IT company, beyond “Employee Costs”, what can cause such an expense?

Finance costs are ~50% of Employee benefits. IT companies typically don’t take debt and acquire

Not filing consolidated results and standalone at the same time (even after 2 months of period).

Passing on the benefit of business growth to investors like paying a dividend would create confidence.