Industry is projected to grow that doesn’t mean every tom dick and harry will grow … They bought 5 companies in last 3-4 years to show that kind of growth , The guy is saying to reach $1 billion target they will acquire $500 Million company and easily reach there … Thats the kind of thinking i would like to avoid .

These guys are not tech savvy they are just bunch of MBAs think they are smart enough to make Money from Money rather than Innovation .

The products they are talking about , do you know how many companies have built that already ? do you know they are not the only boys in town ? if your answer is yes then i would give 100 PE to stock but the fact its trading at 11 PE is because its not something unique they are doing.

I would still say its a value buy , but seeing management i would not like to buy it at any bargain. They already played so much with books by acquiring companies after companeis and showing false growth.

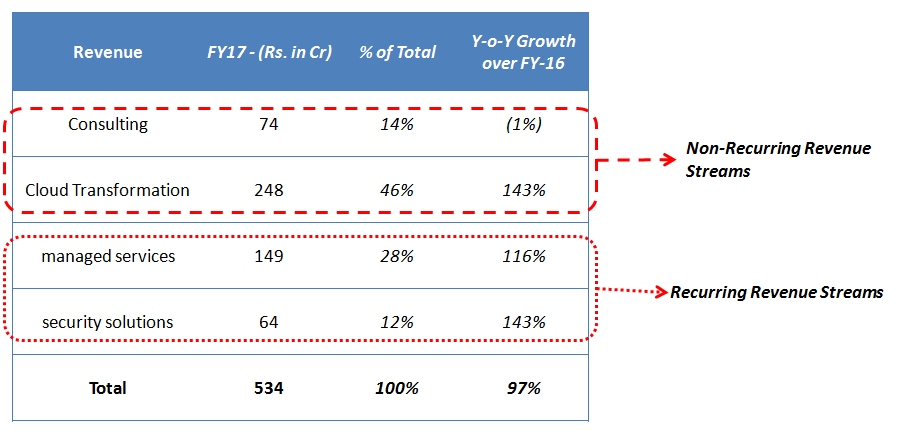

Wonderful … If you could give breakup of revenue for all four bullets will help everybody. How much is one time and how much recurring ?

This is something i never researched because i never thought about investing due to certain qualitative things i never liked about the company.

Cool Dhruva…

Markets are all about contrarion opinions. You can have an opinion against

this company and many will have their opinion against the companies you

own. Your opinions should be based on facts…When you say their books are

cooked, you need to give facts and data…They have now appointed a big 4

as auditors…What do you want the company to do to prove to you, an

individual, that their books are not cooked. I guess the best answer from

the Co was by appointing a big 4 as their auditor…

Here you go. Since their FY-2017 reporting has improved a lot over the last year, below is the segment-wise Revenue break-up, share in overall revenue and % growth in each revenue stream from their AR-2017.

Over a period of time, clients which are undergoing “Cloud Transformation” will move into the “Managed Services” and “Security Solutions” bucket (which is basically recurring in nature).

PWC was the auditor of Satyam, enron had a big four Auditor too and as many other chor’s in the history… Point is that it doesn’t prove anything.

Secondly i am not saying something illegal going on as in Accounting there is huge scope to bloat up P&L legally , specially things get tricky when you are acquiring like nuts.

@Dhruva1705: Can you please help us with the source of your understanding that "these are bunch of MBAs. As per my understanding, MD Suresh has been a hard-core technology guy for most part of his career before turning entrepreneurial. Below is his back-ground:

"For Suresh, a 1988 graduate in electronics and instrumentation engineering from Annamalai University in Tamil Nadu, an academic background and work experience in technology proved instrumental in spotting the potential of the cloud. Suresh started his career as a software engineer with Systime Software in Chennai, before shifting to Singapore in 1990 to work as a software project manager for Singapore Airlines. In November the following year, he began a five-year stint with Deutsche Bank in Singapore, developing the German bank’s electronic banking software (a precursor to today’s internet banking).

"

Source: Blue Sky Thinking: 8K Miles Is Riding The Cloud - Forbes India

I always try to read what employees think of the company and management on Glassdoor. Employee reviews can sometimes be biased or even fake, so please apply caution when drawing any interpretations. I try to look for patterns and one thing emerging in this case is salaries are not always paid on time.

Hi @Dhruva1705 ,

This is an “Honorary Doctorate” degree and does not render them as a bunch of MBAs by any means. Honorary Doctorate degrees are awarded to highly accomplished individuals without them actually undergoing any sort of coursework required for PhD etc.

Honestly, this gives far more substance to his profile/credentials (actually, thanks for highlighting this). You should actually google who all have gotten honorary degrees historically.

I am not sure if the phrase “These guys are not tech savvy they are just bunch of MBAs” is the right one for an Ex-Head of Electronic Banking of Deutsche Bank Singapore with an Honorary Doctorate.

Also, just to summarize brief profile of MD Suresh Venkatachari:

Engineering from Anna University (one of the top notch engineering institutes in India)

He rose to become Head-Electronic Banking at Deutsche Bank Singapore

Started his first entrepreneurial venture with his previous employer Deutsche Bank being his first customer (says a lot about him)

Opened India operations with equal partnership with HDFC bank (I wonder how many companies have actually been able to get into a partnership with HDFC bank historically)

Four ventures listed, sold or exited historically

Gets a Honorary Doctorate degree (most probably for his distinguished contribution in Entrepreneurship and Business)

In summary, the guy seems to be with a good pedigree.

Didn’t they revised the dividend from Rs 7 to Rs 1 earlier ? Anyways MBL infra was paying dividends too …

You should study how easy its to pay dividends with negative cash flow as long as you can raise money through diluting Equity or Debt.

As a consultant who has worked on recent cloud migration (AWS) for a big client, I would like to add 2 cents.

Cloud migration is not a straightforward - create the Virtual Machines/spin the services and blip the switch - process.

One needs an experienced team which can support the transition, troubleshoot and give suggestions on how to plan automatic scaling.

While AWS, Azure, Google offer the support, they don’t do the migration for clients. Clients would still need someone to do the migration.

Coming to 8K Miles, the company is working on converting its one time engagements to recurring revenues by providing bots and services. Integration of acquisitions in IT helps in cross-selling and building a strong base in health care vertical where they want to position themselves strongly.

Hi @Gaurav_Agarwal:

This is terrific data. Is it your proprietary data compilation by going through historical reports ? If not, can you please help with the source.

Also, one way to look at past acquisitions is that these have been value accretive (other than Fugen Solutions which was mainly acquired for Identity Access Management technology/patent and was not expected to directly contribute to revenue). Also, “EBITDA addition to 8k” would have been probably a better metric to compare value accretion by previous acquisitions instead of Revenue - not sure if that is available some where.

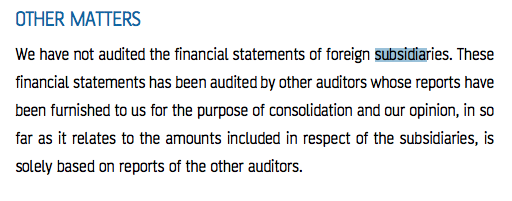

This is more a generic question about auditing of subsidiaries. For a company like 8k miles whose standalone revenue is just 7% of total turnover, the auditor GHG Associates and now Deloitte Haskins are auditing only the small part of the company and the rest is either unaudited or audited by other nameless entities. Isn’t this a big gap in general of how foreign subsidiaries are currently handled?

The statement clearly mentions that financial statements has been audited by other auditors whose reports have been furnished to us.

It means

Foreign subsidiaries have been audited.

Audit report has been furnished to auditors of Indian company.

I think this is standard practice and I have seen this kind of statements for many companies. I can did that out, if you would like to know the source.

I have complied this from the sources on the web. The data is freely available, I think Ebida will be difficult to come by but we can try.