I could not understand what do you mean by that. Most of the business of 8K Miles is in USA and therefore almost all the profit is generated in US subsidiary.

Indian company hold majority stake in US Subsidiary 63% according to latest annual report therefore exert full control over the subsidiary.

Also, Chairman & MD of company Mr. S Venkatachari holds around 54% in Indian company, therefore he hold majority of Indian company and therefore US subsidiary.

Under present situation I do not think minority shareholders have anything to worry as far as control of US subsidiary is concerned.

My suggestion based upon my learning from loosing money in some companies. Revenues, customers and net profit etc can be easily manipulated. One can not manipulate cash flow. Pl analyse it to check if profit is really getting converted to cash or is it just a book entry.

Mutual fund managers know a lot more than most of us. In my experience- do not touch a stock shunned by mutual funds.

Any IT service company which can not generate cash flow raises sirens to me as in last 10 years have seen odds of such companies creating long term value very low. List is endless and have lost money on some of them . So , kind of avoid such companies . Gave it a pass a year back.Also do not find anything special (except cloud growth where they are in last leg of commoditized service n as a vendor will get squeezed under competition ,also, not sure of repeatability of business as per operating model ) in their offering and see better quality of IT businesses available.Usually, if a company gives warning signs in 10 minutes of analysis based on investment framework , then I avoid pursuin further investment interest .However, as a part of academic exercise , would try to analyze the numbers in detail and put my perspective once have detailed clarity on financials and it’s relation to operations

Current level is sort of a first level support (High of 403 made in Oct 2014) but this point has been tested only once and so may not be a very strong support. I think 350 will be a strong support and there is a chance of a horizontal consolidation between this range of 350-400.

I would request investors to not rush in to buy near the support levels. Let the stock consolidate at these levels. When a stock falls like this, in most cases it will not take a sharp V shaped turn and start going up.

Even if it starts going up, it will test the previous low one more time (W pattern) and only if that low holds then we can be sure that the stock has bottomed out in the near term.

Of course this stock is not for the faint hearted!

Last 4 quarter numbers (Revenue, Expenses & Net Profit) for Mar-16 to Dec-16 are not the actual numbers reported by the company.

These are the projections that I had tried to do as on 13-April-2016 (check the date of the post) based on information available about the company at that point in time.

Cash flows aren’t that alarming as pointed by @Gaurav_Agarwal

Presuming the reduction in announced dividend spooking investors, will the change in auditors from GHG Associates (I don’t see any BSE listed firm audited by them) to Deloitte (Top 3 auditing firms) would have caused this fiasco. Since management would have planned based on previous accounting firms recommendation that newer firm is not comfortable with (i.e to take from parent company in short term)?

On frequent pledging, I think if share price heads south there will be more need for pledging which is obvious. As long as it is not to raise fresh funds (given that company has 80 Cr in cash. of course consolidated), is there something to worry?

Areas of concern:

CFO selling stake few months ago

Management could have communicated well. May be in upcoming presentation they would.

Growth isn’t organic No big investors in shareholding pattern except for mutual funds

Economic times today published an article titled heroes of bad times: Look deeper to pick these hidden gems on D-Street.

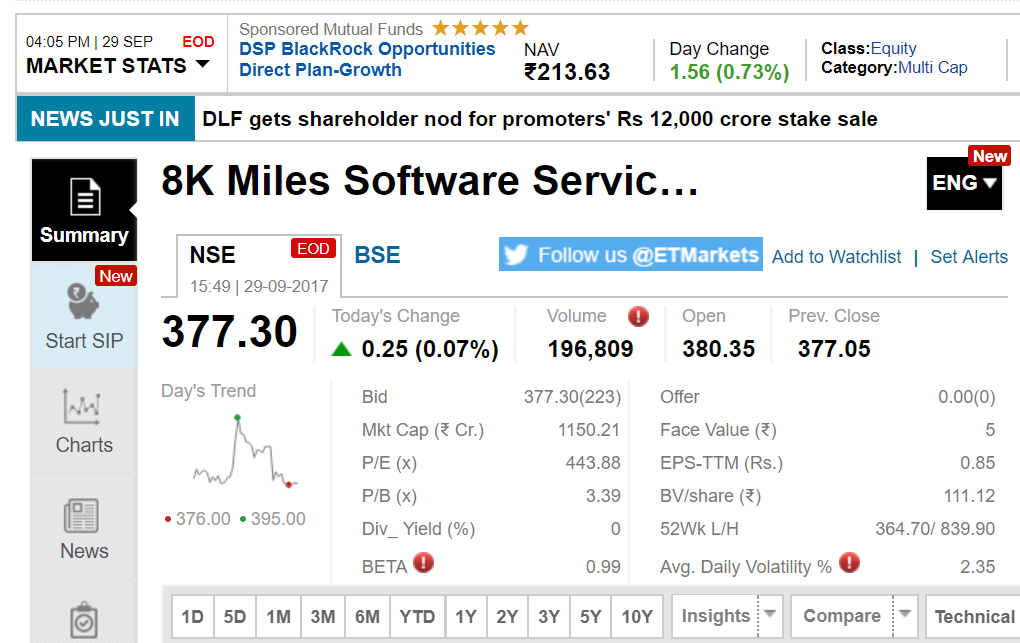

The article mentions Mr. Raamdeo Agarwal saying 8K Miles is trading at PE of 432 to FY17 earning. I think this misconception is prevalent in the market. People look at Standalone PE and leave the stock.

Surprisingly the stock is trading at consolidated PE of 11.x

The confusion could be ultimate reason for stock languishing at such discount.

Invested as of today. Views may completely biased. Thanks in advance for pointing any mistake.

Edited - 29/Sep/17 6:00 pm

The article has been edited by Economic Times, please see below screenshot of original article. Motilal Oswal has clarified as follows.

Quote

The journalist Mr Amit Mudgil has just taken the thought Good companies are good, because they do well in bad times from Mr Raamdeo Agrawal’s interview on ET Now. It is Mr Amit Mudgil, the journalist’s own choice & selection of companies to write based on Mr Agrawal’s thought. Amit has also mentioned in the story that he took this idea from Mr Agrawal’s interview on ET Now.

I have taken this clarification from Mr Mudgil. He himself has agreed that the companies mentioned are not from Mr Agrawal but are of his/their own research/choice.

This has been highlighted in the previous post. The wide difference in perspective is the data point taken to evaluate PE - whether standalone or consolidated earnings are taken to evaluate the PE X. Hope this clarifies.