Of the total, Zydus Wellness acquired 67.86% shares in Heinz India at a considerable amount of Rs3,167.36cr, while 32.14% acquired by Zydus Wellness—Sikkim at an amount of Rs1,500cr.

To give a culturally-rooted option to sugar-loving Indians, Zydus Wellness, part of the Ahmedabad based pharma major Cadilla Healthcare (makers of Sugar Free, EverYuth, Nutralite) launched a product which looks, feels and tastes like sugar. Two years and many clinical tests later, Sugarlite launched in the Indian market as ‘a first-ever product of its kind’. Made with Stevia, a natural plant, Sugarlite claims to cut calorie intake by 50% without comprising on sweetness.

From a brand architecture point of view, the company has deliberately kept Sugarlite as a separate brand in its portfolio rather than co-habiting it with legacy brand Sugar Free. Sugarlite is the company’s play to grab a larger pie in the Rs 2500 crore branded sugar market.

Packaging is hilarious. It looks like a Dettol handwash pouch. ![]()

7 Likes

Came across this article on the acquisition. Integration might be a big issue going ahead mainly cultural it seems. Zydus as a company seems to be getting/increasing their market cap in the consumer wellness segment. Need to see how the integration helps them to acquire more market share.

Article Link - Zydus-Heinz Acquisition Deal: Will it add more sugar to Zydus?

1 Like

Nice article!. Thanks.

I believe that the large distribution network of Complan and Glocon-D will be helpful to distribute SugerLite, which they plan to keep next to Sugar in stores. Also I can see in my local stores that the availability of Everyuth is less, except in Malls, which should improve also.

What about Compan? Is this available abroad also? Who sells them? Heinz or GSK?

The following made me interested!

I am from Eastern part of India where these malt-based beverages are very much in demand but I think for the whole of India these kind of ready-to-drink units will be perfect. Amul already has similar products which IMO is very much popular.

Another article

https://www.business-standard.com/article/companies/riding-on-heinz-zydus-wellness-eyes-rs-4-500-crore-turnover-in-5-years-119060500884_1.html

3 Likes

Zydus reported net loss today. I see that they have converted noveltech and tech to fully-owned subsidiaries. Any idea what’s the reason?

Disc: invested

Anybody attended concall? i could not find in researchbyte or stockadda

I have attended the concall and few important Key takeaways

-

One off item for H1 is around 33 cr which impacted the profit . One off in Q2 is 7 crore towards consultancy charges for integration

-

Synergy benefit approx. Rs. 40 crore to accrue in next 2 years

-

Income Tax rate will be Zero

-

Gross margin -56 percent and for whole year to be around 60 percent . Impacted-1 percent on account of RM cost and 2-3 percent product mix

-

Seasonal nature of biz and sales & profit best in Q1 and Q4 . Main reason is significant dip in sales of Gulcon-D and NYcil in Q2

-

All product categories growing and market leaders except Complan. Complan market share 5-6 percent only … focus is to increase the market share of Complan

-

Advertisement cost 18 percent in H1 and expected to 15 percent for the whole year

-

Growth in sale 9 percent excluding byproduct

I hope it helps

4 Likes

I have a query to the Vp 's here those invested in the company that if one want to participate in the growth of the company isn’t it good that one can be invested through Cadila Health care , as this is the parent of the company and have more diversification products

Regards

1 Like

THere is always holding Company discount… It’s just like BBTC and Britannia… you can do the maths and see yourself…

3 Likes

You may use Stock Edge to retrieve the transcript.

Q3 Concall Notes

Edelweiss

Nippon India MF

Centrum

Sherkhan

Spark Capital

Chartered Capital

India Nivesh

Quarter was challenging because of milk, palm oil price increase

-

Scaled up go to market, reduce cost to serve

-

Supply chain, Help reduce logistic cost through optimization and fright lane consolidation 65 to 23 CMS for company

-

ERP SAP S4 HANA, fastest implementation.

Income 3327M 128% YoY EBITDA 327M -13% YoY PBT -55M -112% YoY Net Profit 42M -89.3% YoY

Highlights of Operations:

-

Surefree, TVC, Medical marketing program,

-

Everyouth, eCommerce exclusive products, TV campaign for peel off

-

Neutrlite, Good volume recovery,

-

Complan, Increasing media weight

Growth Market Share Sugarfree 8.9% 94.6% (1st) Facial Scrub 9.1% 32.4% (1st) Peel off 15.3% 80.9% (1st) Prickly Heat 9.9% 34.5% (250 bps increase) (1st) Glucon-D 11.9% 59% MFD(Complan) 9.2% 5.5%

Q&A

Edelweiss

Q. Complan, historically category have had high margin? How r u doing?

Maintain prices, seeing recovery. if inflation persist will take call after 1-2 quarter

Q. Low Unit Pack(LUP) strategy?

For MFD category, Low margin on LUP, so staying away of LUP

Q. Synergy in Chemist channel?

Seeing 20-30% increase in direct distribution, by just integration,

Over next couple of quarter we will expand that. Chemist will be certainly + point.

Q. Growth slowed down for eCommerce ?

Bullish on eCommerce ,

For Complan we have strategy, we believe good upside on this.

For Everyouth, we have 6-7% sale from eCommerce. Micellar Cleanser, will help us.

We have couple of product to launch in next 3-4 quarter.

In top 2 player in Facewash in Flipkart Billion dollar sale

Q. Personal care slowdown?

There is always gap between what we see and what Nielsen reports.

Yes there is slowdown

Nippon India MF

Q. Quarter-wise breakup

Calender Q1+Q2 = 60% of revenue, 90% of EBITA

1 off cost 44Cr for 9M will not be repeated.

Q. A&P cost have come off on QoQ basis. How are we taking it forward?

Plan to maintain A:S at 15%

In Q3 no spend on brands like Glucon-D and Nycil, which have much lower sells, Thus mix (ratio) is changed. Because commodity is under pressure, we have taken this call. Annual Guidance of 15%.

Centrum

Q. What is Complan penetration?

Will discuss brand level details on separate call

Q. Sugarfree volume growth around 8.9%

Price increase on 9 months: taken 4% of price increase since 2015

Q. 3.7L outlet coverage plan, what is current level?

2.3-2.5L. WIll reach 5L in 2021

Sherkhan

Q. Wont reach 20% margin in FY20, what can we expect in FY21?

17-18% for FY 21.

Q. Revenue growth & operating growth?

Mid single digit for overall portfolio

Spark Capital

Q. Update on new variants of Complan?

Not launched yet

Q. Distribution, Employee cost, supply chain consolidation

Completed sales integration

Integrated Coverage as outlet

Employee cost consolidation done

65% cold chain, consolidation.

40Cr of synergy benefits, substantial portion will happen on next 4-10 weeks

Q. What r u surprised of after 1 year of merger ?

No surprise, other than Complan. But on track for what to do on brands

Surprise is commodity pricing

Chartered Capital

Q. Cash flow?

Should be 140-150Cr for the year.

Q. How will debt be repaid?

Believe operating cost will be enough for debt repayment

Centrum

Q. Cap utilization of new plant?

No capex needed on Aligarh & Sitarganj plants. It is sufficient

75-85% utilization of Aligarh plant.

Q. International plan?

Clearly defined markets, Middle east, Africa, Southeast Asia.

Already Sugarlite, Neutrlite, Everyouth sale started in some of the market.

Complan in New Zealand, Taiwan, Nigeria, Middle East, and couple of other.

Next 3-4 Quarters 3-4% of our business will come from International business

Goal of 100Cr+ business 2-3 year.

India Nivesh PMS

Q. 44Cr one off cost in first 9 months, & 33Cr in first 6 months.

11Cr in this quarter. Hopefully won’t be any further.

Q. Plan into get into winter product to mitigate seasonality?

Yes. Nycill, Glocondi, looking opportunity beyond summer.

Take 3 years, before we able to balance out overall revenue, but we do have plan, to extend current brands.

Q. Input cost? Is it going to continue?

External factor, Ban on oil procurement from Malaysia, by Government of India produces spike in oil. It will stabilize in next 2 quarter. It is temporary and not long term. Banned SMP (Skimmed Milk Powder) import by India, led to increase price in milk and SMP. Will wait and watch 1-2 Quarter. After that in 3-4 Quarters, will absorb it by price increase.

Q. Extended winter, will have any impact?

Yes. but it will balance out in summer quarter.

4 Likes

what is the tenure of 1500 NCD on the balance sheet?

Company raised funds through Redeemable Non-Convertible Debentures in 3 (three) tranches, namely Tranche 1, Tranche 2 and Tranche 3, of the face value of ₹10 Lakhs each, for ₹500 Crores in each tranche, aggregating to ₹1,500 Crores, having maturity periods of 3 years, 4 years and 5 years respectively.

Issuance Date: 16-Jan-2019

Followign are maturity dates:

| ISIN | Maturity date |

|---|---|

| INE768C07017 | 14-Jan-2022 |

| INE768C07025 | 16-Jan-2023 |

| INE768C07033 | 16-Jan-2024 |

1 Like

Stock tales by ICICI Direct

http://content.icicidirect.com/mailimages/IDirect_ZydusWellness_StockTales_Dec19.pdf

Q4FY20 Results Update

Disc: Invested through Cadila Healthcare

What will Happen if a company does not have enough funds to redeem the NCDs on the said date? will there be an extension? a look at the B/S of the company as of date does not show enough liquid asset which they may need to honour 500 crores in 2022. Any idea how this is done generally? thanks

Hi,

Results are out and considering the pandemic situation,the results are good.

For the first quarter ended June 30, 2020, Zydus Wellness Ltd. reported consolidated revenue from operations of Rs. 537.4 crores. Earnings before Interest, Depreciation and Tax (EBIDTA) of Rs. 122.3 crores was up by 0.3% on a y-o-y basis. PBT after exceptional items, was up by 4.1% to 83.1 crores.Net profit for the quarter was up by 10.9% at Rs. 89.2 crores from Rs. 80.4 crores in the corresponding quarter of the previous year.

Results can be viewed in the below link.

They are keeping the innovation track continued with customer connect.

Quoting from the results

During the quarter, Zydus Wellness launched several innovative products. Foraying into the toddler health food drink segment, the Company launched Complan Nutrigro which packs in nutrition with a 50:50 proportion of whey & casein. The product is being promoted through doctors. The Company also launched Nutralite Choco Spread in two flavours through the e-commerce platform. As an extension to its Glucon D brand, the Company’s new offering Glucon-D Immuno volts is ready for the market. The tasty energy bites, fortified with Vitamin C, Vitamin D, zinc and glucose, boost immunity. Complan in a convenient 75 gms satchet is also ready for launch.

Coping with the pandemic, the Company continues to be agile in its responses and execution of its plans. Stepping up the marketing initiatives for its marquee brands, Zydus Wellness has been harnessing the power of digital communications and social media to reach out to its customers. Sugar Free was promoted using the #StayHomeStayFit challenge.

Thanks,

Deb

2 Likes

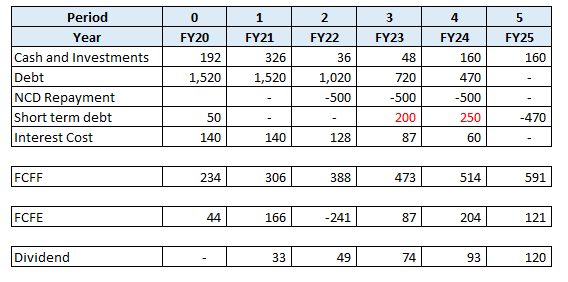

In FY20, Zydus generated the FCFF of 234 crores. And considering interest payment of 140 crores and borrowings repayment of 50 crores, FCFE was around 44 crores.

In FY21, they should generate FCFF of nearly 300-320 crores approximately (as per my estimate), and considering 140 crores interest payment, FCFE should be around 160-180 crores and for FY22 (9 months), FCFE should be nearly 100-120 crores approximately.

As of 31st March 2020, they had 82 crores cash and bank balances and 110 crores in the overnight fund.

Hence, they should be comfortably able to repay debt in FY22. But for FY23 and FY24, they might need to take short term debt to repay NCDs. And again repay the short term debt in the subsequent year. Or they may not distribute dividends for a few years. Also, consider the fact that I have taken a very conservative estimate for the growth in FCFF.

But the conclusion is that they have a fairly good liquidity position.

2 Likes

Hi Ahmed,

I am trying to learn the financial statements and was going through the Annual Report of the company Zydus Wellness and also invested in the company.

I have some questions regarding your analysis.Questions are naive ones but I am finding it difficult to understand. So please help.

If possible kindly clarify my doubts.

So regarding the above calculation of Free Cash Flow to Firm (=234 crore) ,I see 260 crores as the operating cash flow and “Purchase of property, plant and equipment and other intangible assets” as 24 crores.So is the FCFF differences of operating cash flow and purchase of fixed asset cost?

I understood that Free Cash Flow to Equity(FCFE) = FCFF - (Interest Cost + Short Term Borrowings).

What is the free cash flow for the company?Is it the figure “Net (decrease)/ increase in cash and cash equivalents”?which is -84 crore.

Would you mind sharing your thought process regarding the above calculation?

And also the “Cash and investments” for the year 2021 you have assumed the figure is 326.Please let me know also the calculation for the same.

Thanks,

Debadutta

-

Free cash flow to firm (FCFF) = CFO - Net Purchase of PPE = 259 - 25 = 234 crores approx. Basically, FCFF is the amount left with the business to honour interest and debt payments. And subsequently, distribute cash to shareholders.

-

You are correct on FCFE (after paying interest cost and debt repayments).

-

Net increase/decrease in cash and cash equivalents is neither the free cash flow for the company nor for the shareholders. Because it deducts the non-operating investments and dividends.

-

Cash and Investment in FY21 = Opening Cash and Inv (FY20) + FCFE (FY21) - Dividends

Thanks and Regards,

Ahmed Madha

1 Like

Zydus wellness

Annual report analysis

FY20 was the first year after the consolidation of acquired Heinz business. However, the year was also not normalised given disruption

at the end of the year due to Covid related disruption. The loss of sales in March was to the tune of | 100 crore. The impact on sales was much more than other FMCG companies considering Q4 & Q1 account for more than two-third of sales on a normalised basis. Moreover, ZWl also incurred | 40 crore acquisition related expense during the year

The company has taken four major initiatives to leverage scale benefits post acquisition. (1) It is re-organising its employee structure to reduce

redundancies and faster decision making, (2) The company aims to double the direct distribution network and rationalise distributors from 1500 to 800, which would increase its product penetration & simultaneously reduce the cost to serve, (3) It is implementing CFA

consolidation through warehousing optimisation, which would reduce the logistic cost, going forward, (4) The company has implemented integration SAP S4 HANA

The company implemented Project Udaan to integrate two separate sales organisation. With acquisition synergies, the company was able optimise its cost. It is infrastructure ready to drive direct distribution

The glucose powder category grew 9.8% while the company has a market share of 59%. We believe the category is ~| 800 crore. Malt food

drinks (MFD) category witnessed growth of 7.7% with the company holding a market share of 5.4%. We believe the category size is | 7000

crore. The company holds a market share of 94% in artificial sweeter category with sugar-free brand. We believe category size is ~| 370 crore

Within skin care category, ZWL has market share of 77.9% in peel off segment (that is estimated to be ~| 80 crore), 32.5% market share in scrub segment (that is estimated to be ~| 280 crore). In Prickly heat powder category, Nycil is leader with 34.4% market share. The category is growing at 8.3%. The category is estimated to be ~| 850 crore

Nutralite is largely a HORECA brand, which has been severely impacted by Covid related disruptions. However, the company has launched new variants to drive ‘at home’ consumption. The brand contributes ~3% to sales, which would not significantly impact overall sales

The company launched Nycil sanitisers in March-April 2020. ZWL re-launched Sugarfree green with new formulation and new packaging. It also re-launched Sugarlite with better formulation to address the question of taste. ZWL has launched a new campaign to drive growth

ZWL entered new markets of New-Zealand & Kenya. The company also launched ‘Complan’ in Middle East countries. It will be managing all its

international operations through its new 100% subsidiary ‘Zydus Wellness International DMCC’

The company spends ~13% of its sales as advertisement & promotions. This gives it manoeuvring power to reduce spends at a disruptive times.We believe Covid related disruptions would not impact earnings

significantly. On the other hand, trends related to health & wellness would benefit Sugar Free & Complan grow faster

The company has accelerated its efforts to digitise operations through scaling up e-commerce sales & digital marketing initiatives. The sales of FMCG Industry on e-commerce are expected to reach US$ 4 billion (which would be 5% of overall sales compared to 2% currently)

5 Likes