Yep. That’s what my analysis also showed. There are not much patents in anti drones as of now.

So according to company annual report for FY 22-23 page 26. They have applied for 130 patents and 50 have been granted. Since granting of patent takes time and their Anti-drone business is new there is a possibility that the patents for Anti-drone systems may be in application stage.

As per the search by @vikas_sinha 89 patents or patent applications are mentioned on the WIPO website. We will have to analyse those for Anti-drone systems and find out 41 missing patents or patent applications.

3 Likes

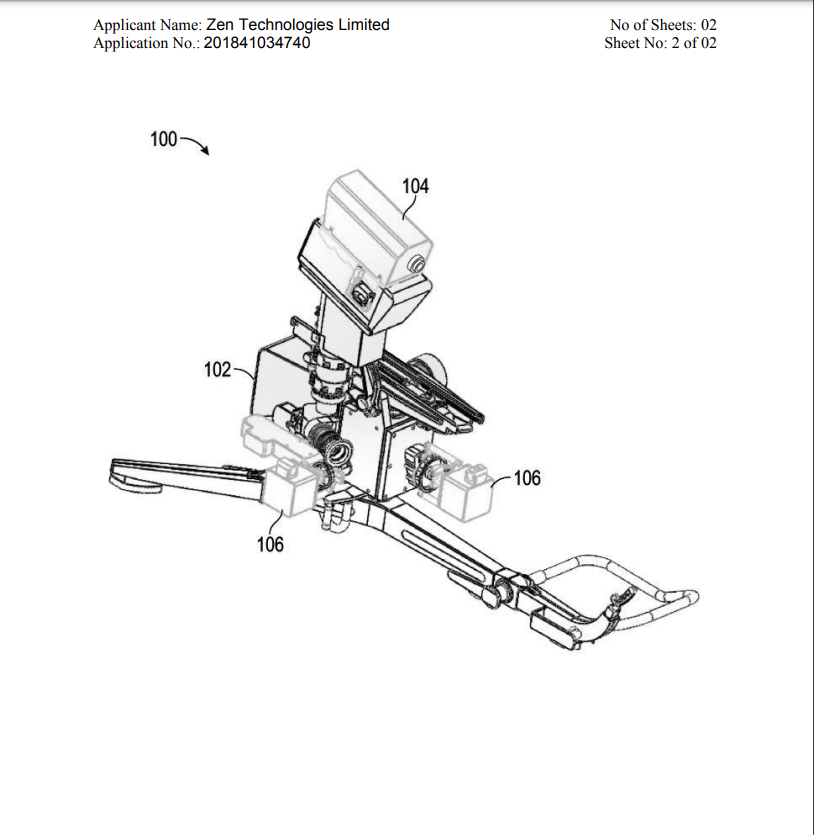

The patent/patent application - Retofit tracking system is not related to Anti-drone system. A drawing from Indian Patent reveals this.

Also I have analysed to the best of my ability all the 89 patents or patent application mentioned in the reply of @vikas_sinha No one is related to Anti-drone system.

Even after spending lot of time on Indian Patents online search and WIPO I could not find remaining 41 patent or patent applications.

This looks like a dead end. We have two options now -

-

To ask the management of company to respond to assertion that company doesn’t have many patent or patent application related to anti-drone systems.

-

To hire a Patent attorney to find remaining 41 patent or patent application and then we can analyse them.

Thanks

Gaurav Agarwal

All the information provided in this post are from open sources and I may be completely wrong.

8 Likes

I have asked the management for no of patients in anti drone sys as i was having conversations with them earlier via mail lets wait for there reply

Dis-Invested

9 Likes

The reply i got

Sir,

The details I can give at this point of time regarding patents are follows:

The Company has applied for over 150+ patents out of which over 60+ granted (this information is also available to the public).

As you are aware, for all specific Questions (for which I can’t comment), the right forum is Analyst/ Investor call. Please be informed.

6 Likes

So only option is to ask them on the IP for anti-drones in the concall .

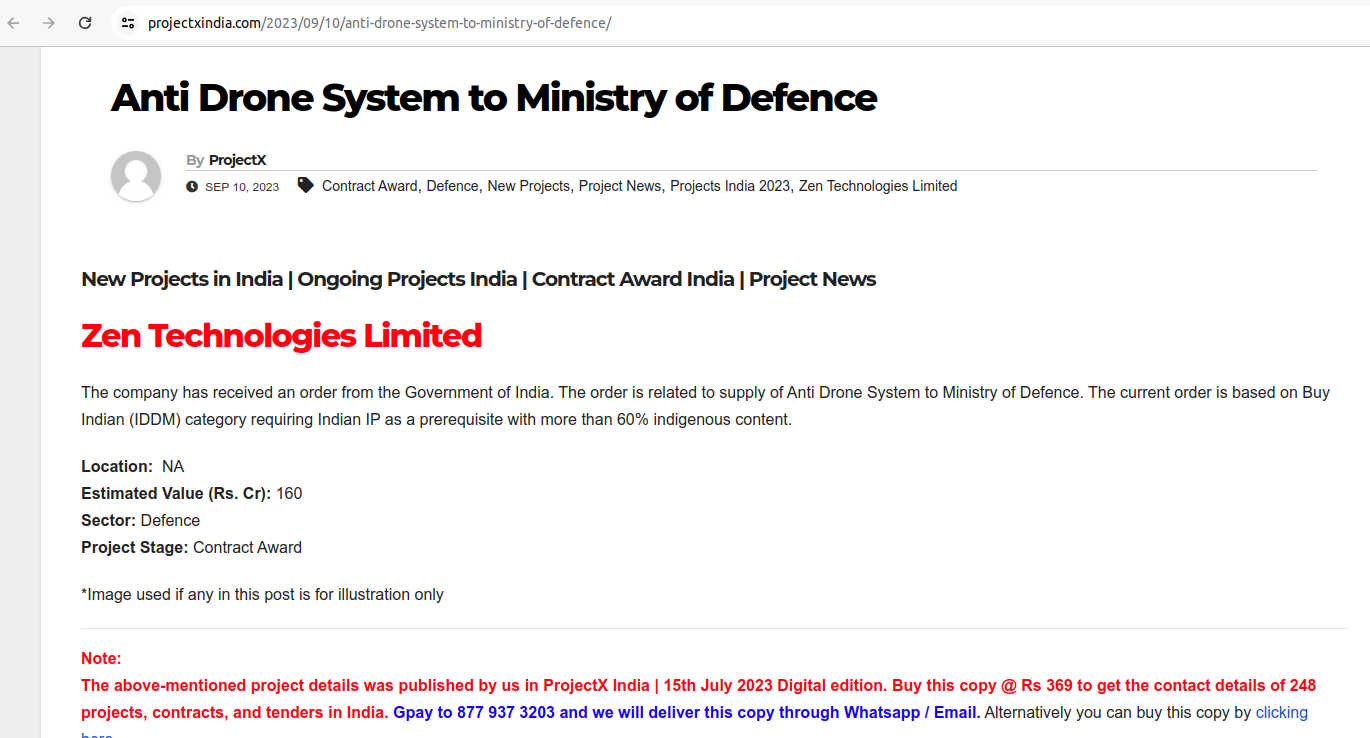

I have found this on the website of a magazine name ProjectX. The news item is dated it’s from 10/Sep/2023. This news item talks about 160cr Anti drone contract award to Zen technology. What is of interest of us in this? The interesting thing is the prerequisite for award is 60% of indigenous content and Indian IP.

So, Can we conclude that all the components and firmware(software) cann’t be imported?

4 Likes

In my opinion

1- zen entered in anti drone in 2018, I don’t think they have some kind of edge in this sector, but company is winning orders from export so there might be something we don’t know (surely will be asking this question to management in upcoming concall)

2- remember management itself clearly stated that they are no 1 in simulator but in anti drone they are 4-5th in world, thats why OPM is less, but they are optimistic for 50/50 shares of order in simulation and ADS

3-Will not see any major order win for next 2-3 months but expecting huge orders in FY2025 ( not disclosed about order they quoted) last concall they mentioned me that have quoted for 500cr orders in H2 and there win rate was around 80-90% but reflected in single order of 42cr no clarification given by management to me.

4- We need at least 1300-1500cr of orders in Q1&Q2 of FY2025 then only we will see their PE around 70-80 otherwise we might see PE de rating irrespective of 900Cr of sales in FY2025 which they are guiding

7 Likes

93cr order in simulation after long time

7 Likes

Finally new acquisition of Aituring Technology for 3.87cr

2 Likes

Sales not important it is important to see weather they have IP in ADS or not

1 Like

The products seem interesting and could add synergies to Zen technologies hopefully

An acquisition at 4 crores seems like ‘Heads I win Tails I don’t lose much’ approach

Let’s wait and monitor, how this pans out

6 Likes

The accusation was basically for camera system that is used in ADS.

3 Likes

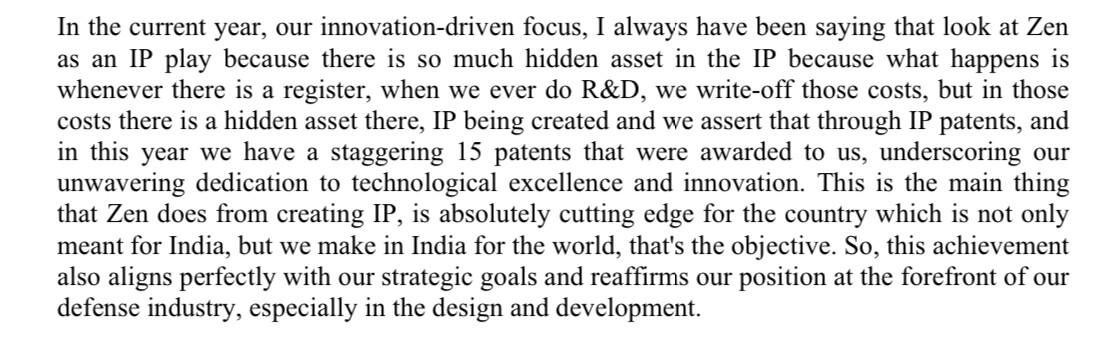

This is from the opening statement in Q3 call. Management has repeatedly stated that Zen is an IP play.

3 Likes

no doubt about that. It is indeed!!

Interview with CEO from 4 days ago, explained that acquired company was for anti drone vision systems. Also that payments are always received on time.

Disc: invested

3 Likes

![]() Key figures & highlights

Key figures & highlights

Secured 15 new patent grads in India (in FY24)

On track to achieve 450cr+ revenue for FY24

Aiming 900cr+ for FY25

EBITDA target of 35%

looking at opportunities to expand inorganically

passed a resolution to raise funds up to 1000cr

![]() Expecting a CAGR growth of 50% for the next three years (FY26 TO FY28)

Expecting a CAGR growth of 50% for the next three years (FY26 TO FY28) ![]()

![]() Long-term focus has been on achieving leadership in several key areas, including development, both live and virtual wave simulators, leadership position in anti-drone market.

Long-term focus has been on achieving leadership in several key areas, including development, both live and virtual wave simulators, leadership position in anti-drone market.

Read full Q3FY24 highlights: https://twitter.com/Bornwinner_VJ/status/1753311517712519502

1 Like

Promoter is very positive and so far, it seems to trend well. The only risk I can think of is the election. If Govt change, then these companies might face a big correction. There is no margin of safety at current level. If we believe their story will pan out, then its a good buy but definitely not a value buy based on where things stand as of now.