The notification - Yes Bank Limited Reconstruction Scheme, 2020

218653.pdf (849.3 KB)

1 Like

Thank you. But what happens to existing investors? Also any idea on how to apply for the new shares for 10 rupees?

One also need to look assets in light of IBC code. With strong banks coming on board or as shareholders, odds of recovering back partial money from defaulted borrowers improves, leading to an improvement in networth.

Disclaimer: No interest in turnaround plays, structural growth stories are preferred more.

What is most surprising is that a commercial bank with lot of oversight from the famed RBI does frauds of this proportions. You cant just trust the books the auditors are producing, RBI is validating. If books cant be trusted signed by auditors and validated by RBI then the faith in stock markets itself goes down considerably and so in the capitalism.

2 Likes

What can the RBI possibly do if it finds fraud? It did review Yes Bank’s books back in 2015 and 2016 (as part of asset quality review - AQR) and it did its part post which the bank reported divergences in both years. This was a fair enough warning because the divergences if I remember right were pretty huge. The bank simply wasn’t learning from mistakes and warnings (it had an incentive not to, so why would it) which was why RBI insisted that Rana Kapoor go, back in 2018. Even then there was enough chance for shareholders to exit but how many did?

The trouble with RBI going all out and declaring the bad news in the frontpages (like a CAG would) is that it would cause absolute panic and make rectifiable bad news to certifiable bad news which is certainly not its mandate. I very much pity the RBI because they get the stick from everyone whether they do their job or not. Just see the number of people that left the RBI or from Economic Advisory positions in the last few years. It shows how crippled the RBI is, as an organisation in terms of enforcing its mandate.

So the next time you see similar hints from RBI, you know what to do. Don’t wait for them to hold up the sell sign.

23 Likes

Looking forward, it would be interesting to get some views on why a depositor run will stop when the moratorium will be lifted on Wednesday? 1. Customers now will place a higher emphasis on safety of principal than the absolute returns. With the moratorium experience, it might be the case that depositors might move to other banks. 2. 11K crores of equity raised is still a small portion of the entire book for YES Bank now that the networth is largely written down this quarter. Why would anyone still keep a deposit in Yes Bank post this episode?

Balaji

Not bragging for my above post some time ago . Just wanted to reiterate above msg by Phreak on RBI giving investors, enough warning signs. Time and again, I keep hearing what has RBI been doing during this whole saga etc. In my opinion, they have been done a commendable job. Some of the investors acted upon the warning signs and exited the counter. Every time there is such a failure, same old learning’s will be realised by some new set of investors. Interestingly, we will find some valid reasons to rationalise our actions which later prove to be futile.

3 Likes

I think you have reconciled with the fact that RBI has done enough but I think regulator job is to act on the information available and act in time rather than giving tell tales signs to investors and depositors that all is not well. (What do you expect a retried depositor in yes bank to do keep checking RBI circulars that all is well with bank. Should I do that with SBI also, check if the loans given are proper or check factories that they are utilising the money properly?)

What happened in 2008 in US financial crisis is repeating here and RBI has accepted that instead of acting on information (they have turned blind eye to internals), bailout using public money is the solution and have acted based on this premise which is exactly what is happening. ILFS guy, DHFL guy is not even in Jail and I am sure Yes bank guys will come out clean with flying colors (because of growth slow down) and that too this is repeat of 2008.

The broader point I want to make is that if there is not even basic level of trust in a system it is better to stay away.

4 Likes

Why retail investors are buying at more than 20

when other banks are able to buy at 10 ?

Will Yes bank correct to 10?

Why govt did not allow retail participation at 10?

1 Like

The real worth of yes bank is zero or negative, but SBI and few other banks have come forward invest and keep it alive to restore the public trust in banking system and also because they can revive the bank to it’s positive networth with better recovery in 3-5 years.with that background, it’s not advisable to bring in retail investors at this stage as there are still many odds in this story

4 Likes

Writeoff of AT1 Bond has far reaching impact but government wants to handle current issue not bothered about long term impact…

What far reaching/long term impact?

Like others said, RBI has raised enough red flags for an investor. The only one and the most important one that mattered to me was - Rana Kapoor’s writ run large, and there was no checks and balances as in institution. Yes Bank failed to function as a collective institution and I headed for an exit and did not bother investing after that.

Most Indian companies are poorly run. Head for exits when you see signs and symptoms of that. RBI will not spoon-feed one.

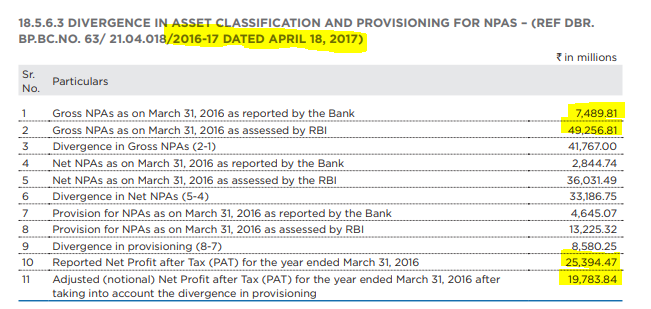

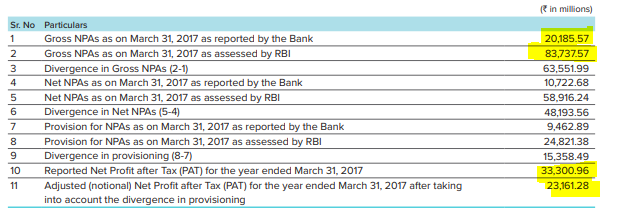

Humongous indeed. Retail investors had enough time as derating didn’t start despite such Divergence being reported.

4 Likes

so YES became YES from being almost NO… but will it survive to remain YES for long term investors… do read this report

1 Like

Hi. Do anyone know how we can check the name of AT-1 bondholders?