RBI will have to bear responsibility for ineffective supervision.In PMCs case they blamed the supervision conflict and wriggled out. In this case they cannot and surely there will be demand for a JPC to examine the role of RBI. Banks have internal audit,statutory audit,RBI audit,the audit committee,the credit committee,the BOD and yet a bank like Yes bank could go down putting the depositors money at risk.

Agree. Banking is just about TRUST. No trust = No value. Small Book value does not help when

trust is gone.

Yes RBI will be very prudent in handing over banking licenses. This is also means, that existing large 4 players will have little competition.

Infact this may impact psyche of depositors in smaller pvt banks negatively and CASA for them may remain elusive.

Share price will go down to zero and bank will be taken over by one or multiple PSU banks jointly for a token price of Rs.1 (not Rs.1 per share!). This is the most likely scenario. This is what happened to Global Trust Bank which got entangled in the Ketan Parekh scam in early 2000s and went bust.

What happened to story that foreign has put in condition that they will invest only if some of the state owned banked invest in it .

Isn’t that logical considering the Fact that It’s critical to retain CASA .

And without casa how do they eventually run the bank even if they invest capital ?

What would have happened if yes bank had defaulted on some intrest payment on their BOND ( saw this one CNBC ) which is due Today/tomorrow ?

Why RBI has put in all these restrictions only until 3rd April and not indefinitely ?

I am not able to properly connect these dots.

Will it be reconstruction of bank or amalgamation ?

For me the question is why RBI has put this limit on withdrawl. If state run bank is taking stake, there should not be any worry of exodus of depositors. It looks like something else might be cooking. Now it will create exodus of depositors till the plan is revealed by RBI.

Disclosure – No shareholding. No buy - sell in more than one year.

SBI & LIC are taking over 49% stake. Not able to understand what would happen to rest 51% stake and the share holders?

Besides pricing relaxations, Yes Bank’s potential investors are seeking specific assurance to safeguard their investment. Yes Bank’s Potential Investors Lay Down A Tough Condition: Exclusive

Try connecting both these … possible ?

Disc …Invested and biased

Can someone tell how this transaction will help SBI bank. Even if they get yesbank at 0 cost. Still yesbank has 3 lk crore of debts. What will happen to that. Doesn’t it mean for Zero Rs SBI is purchasing 3lk crore of debt. One can argue yesbank has same amount of asset. But when yesbank is not able to raise even 2 k crore based on these assets then one can do an intelligent guess the worthiness of this asset. Doesn’t it mean SBI is putting very big amount of good money (public money) to huge risk.

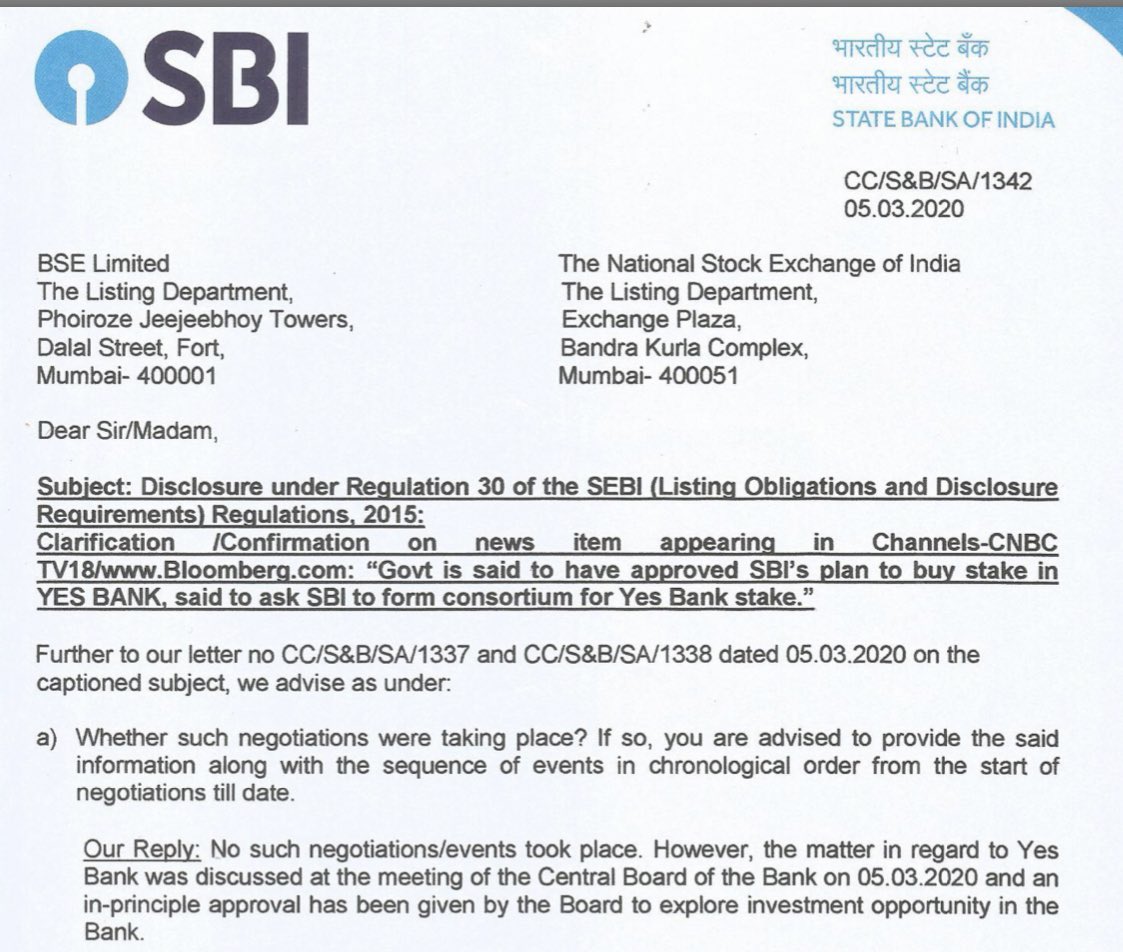

Yes bank has clarified that it has received no communication from any authorities and is continuing to try to raise capital.

Board has already been dissolved by RBI. What management says is of little consequence now. We need to focus on what RBI and SBI says.

1 Like

I completely understand that the board has been superseded by RBI. But this also makes me wonder, do they not understand their own position? And why would the RBI not communicate their decision to the yes bank board/management?

Do you still trust crew of the plane which crashed it in first place? Government organizations work differently. They will not be communicating informally. Everything will be a deliberated formal order.

Here it is. Came in late last evening

https://www.rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=49477

1 Like

It will not help SBI. It may even hurt SBI. SBI is PSU. It doesn’t make decisions based on what will help or hurt it.

The end game for Yes Bank seems near. The signs were ominous for a long time. How many investors questioned how the bank was growing so rapidly and what was this large “fee income”? It was said that Yes bank was the lender of last resort!. If a company did not get loan from any other bank, they could approach Yes bank and get the loan at the right “fee”.

Easy to lend, but unable to recover? But who cares? As long as the share price went up every one was happy.

Now that the bank has unravelled, how will the story play out? Would recommend all interested investors to dig out from internet and read what happened to Global Trust Bank, a high flying private bank which went bust with huge NPAs and was amalgamated into Oriental Bank of Commerce, a PSU bank in 2004.

Denouement as follows.

Depositors - money back guarantee

Promoters - bailed out early

Shareholders - Zilch

Tax payers - grin and bear it.

RBI & Govt - Rinse and repeat

A deja vu moment. It is so easy to forget history and ignore basic questions, when we are caught up in this game of investing!

8 Likes

As per their Q2, Net advances, 2.24 lakh crore. Networth 27.7k cr.

I understand that bond holders and share holders are preferred to the rest. But lets assume depositors will get everything. (Which I think will be the case).

So if they report 27.7k loss, it will make equity 0. Thats a net NPA of 12% which I guess the new buyer will be comfortable with. (As per Q2, net NPA is 4.35%). Doesn’t look that bad. Am I missing something? Or is it that actual npa would be much higher?

Disc: Never held it and no interest. But just out of curiosity.

It might help SBI in the following scenario.

Let’s assume SBI picks approx 255 cr. shares with investment of INR 2550 cr… Existing share capital gets marked down to 2550 crores with SBI holding 50 pc and existing shareholders holding 50 pc. (Will be actually 49-51, but I am using 50-50 to simplify the math.

After SBI/RBI has seen the books and we all know how bad the book reallllllly is, The book gets the vetting of SBI/ RBI. In case the hole is huge, valuation per share is below the Rs. 10 mark and SBI has bought a bad apple. If the hole is manageable, you can ascribe a fair value to the bank. Remember the 210 billion cash/money on call and 108 bil AT1 write off. These become the cushion in determining the size of the gap/ more money needed.

Once this step is done and since SBI is on the board you can have JCF/someone else come in. Refer link. Now if it’s an okay book JCF may have to pay a higher value compared to Rs.10 for the cleaned book. SBI gets diluted (till 26 pc) but the actual per share value goes way above Rs.10. After that they can choose to make an OFS or continue to hold post 3 years.

Do not try to play with either SBI/yes bank with this. There are lots of variables and things we don’t know. To begin, instant scheme is a draft scheme. Tomorrow RBI may choose to completely write down existing equity.

It has ended very bad for me. I had 3300 shares@140. Yesterday sold it @14.5. Lost 445K. This was very good amount for me. Learned a lesson by paying a very high tuition fee.

- Promotors are most important.

- Never hope against hope.

- Never average down.

6 Likes

This is what I had said to all the boarders on this thread on 28th Oct’17 when the price was still above 300 Rs a share. Hate to see the losses of so many investors and even bond-holders but I think if there is a way to learn from it and not repeat the mistakes - it would be a worthwhile journey going forward and these losses would be easily compensated for.

18 Likes

You are missing the most important lesson. Hiding things from stakeholders and regulators is a strict no-no. Eat the loss and get out the moment you see that happening.

I fully agree with this opinion. I too delayed coming out of it and infact bought more on dip thinking that it will catch up with money coming in. Finally sold @rs 37/- and suffered a huge loss. The lessons learnt are:

1.Buy only exceptionally reputed promotor’s companies

2.don’t listen to so called experts on CNBC tv 18.Most of them HV a vested interest.

3.If you come across any news on suspected fraud etc/auditors adverse comments, director resigning, downgrade etc, sell off and book loss/profit whatever.

6 Likes