Columnist says it will merged with some other bank going forward and that’s the intention of RBI to board an ex governor

2 Likes

Although the example I will be quoting might not have direct relation with the yes bank and the phase through which it is going. I had strong conviction in ipca labs couple of years back and the company was delivering good growth and results. But then suddenly it had usfda woes and the price crashed. I assumed that it was a good opportunity to buy ipca as they will soon come out of usfda woes and then the business will return back to normalcy. But the same didn’t happen for quite a long time. The stock price as expected underperformed and stayed like that for quite long.

Lesson learnt : we should not jump to conclusions and should have a detailed strategy for any stock idea.

2. We need to be aware of opportunity cost and why it is a important aspect.

3. A good way is to wait for initial green shoots to emerge and then get into a troubled name. This might entail missing on initial gains , but is a more sound strategy.

Regards

Divyansh

11 Likes

One thought process that always helps is to remember that the market is mostly right, most of the times. So if one believes one is getting something at a bargain, one has to ask oneself

- Whether it is really a bargain, and its always safe to assume that the market knows more than one does.

- If the answer is yes, it is a bargain, then the harder question is WHY.

If this sounds like Efficient market Hypothesis, the key is the emphasis on “mostly”. There are times when market is inefficient in either direction, but it is mostly efficient. The second aspect of inefficiency is the time horizon, but these are points for a different discussion.

I would agree with your proposed course of action, stay put and wait it out and the reasons are:

- Selling now is guaranteed loss. Assuming you have a loss of 30-35%, then you need a stock with a guaranteed gain of 50% to make good your original investment. Do you have any guaranteed stock? If yes, please let me know too

- Buying now carries the risk that there could be more cockroaches in the sink crawling out one per week. We don’t know the extent of bad hidden in the books.

- Staying put. Banking is not in a structural decline, so there is no sector risk you carry. The company specific risk has materialized. What next? There are physical, economic and human assets owned by the bank that are enormous and difficult to replace or build again from ground zero. Maybe the current valuation is at a discount or premium to the underlying assets, but if you strike out option 1 and 2 above, this seems the only one left.

The above is my learning from the Satyam scam back in the day ![]()

20 Likes

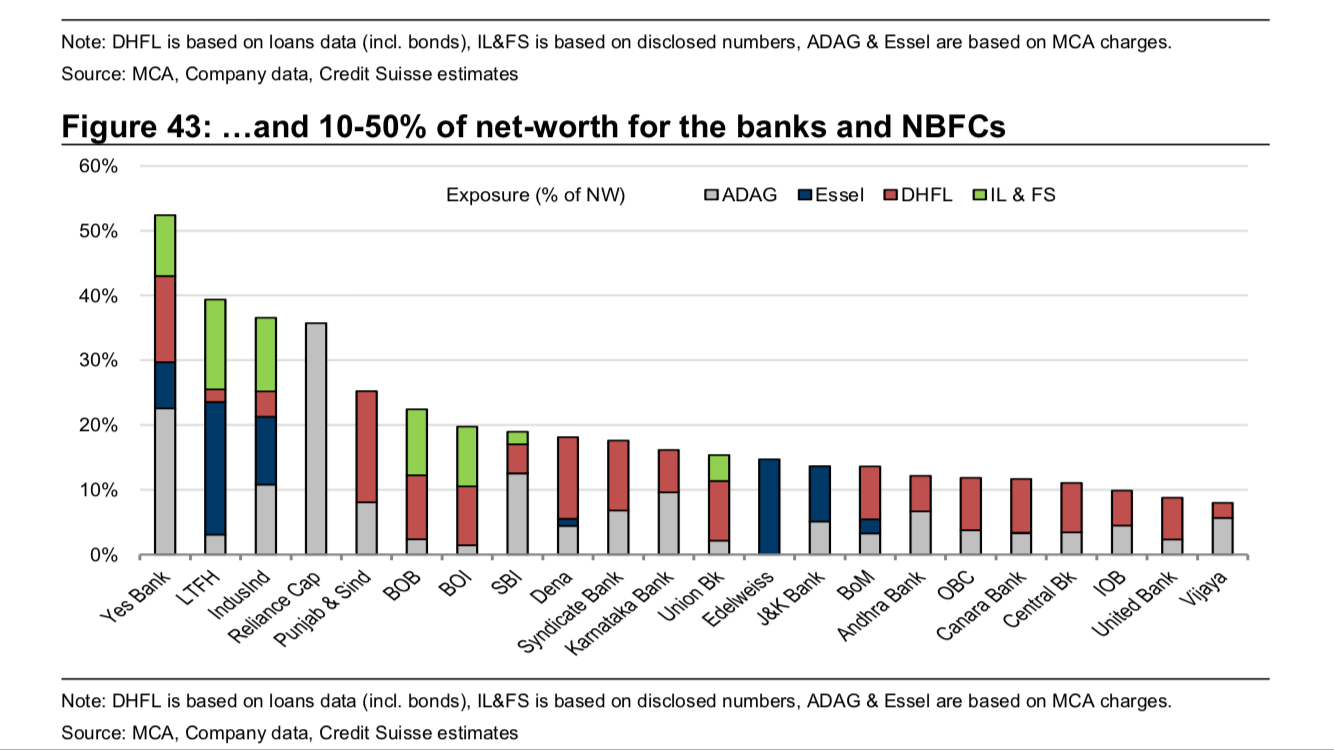

The attached graph shows how deep in trouble Yes Bank is. Exposure to just four stressed groups is more than 50% of its net worth. For these groups it’s not a matter of if they will default, rather when they will default.

If we add jet Airways and others, I think Yes Bank probably already is a lost cause at the moment.

17 Likes

Here is the full report for your perusal. Stunning to see the storied private banks like Yes and IndusInd at the head of this list as well as fancied stories like Edelweiss.

3 Likes

capital raising should be a lot earlier than July/Sep - Mr. Ravneet Gill

Thank you for sharing.

I think, having read the report from cover to cover, except credits & caveats, this is the most important chart. And like you say Jet is not yet and we don’t know what else (just read that Aircel lenders agreed for a 99% haircut) will get added. When a borrower appears to be going bad to the outside world, he is already beyond redemption.

Shouldn’t one move to better banks like RBL

WAIT N SEE for a few quarters

How turnaround to happen

Diffsoft and others, What could be the loss given defaults for DHFL, reliance home finance, reliance commercial finance and reliance capital versus the provisioning cover for exposure to these cos.?

1 Like

While the bankrupt operator may have narrowly escaped liquidation, its financial creditors may recover 15-20% of loans they extended to Aircel, among the lowest in major insolvency cases so far. “Lenders can recover 15-20% of their investments, which is a sweet deal in the given circumstances,” said a person aware of the development. “The asset reconstruction company will take the business as a going concern and run the smaller businesses like bulk SMS and enterprise. The rest of the assets will be sold and that money too will go to the lenders. The recovery will take 12-36 months.”

20% recovery is there … News highlights 99% haircut is just way of over exaggerating

1 Like

I don’t know how RBL bank is different to Yes Bank or axis bank. Also RBL has low return on equity and is currently at very expensive valuation compared to other private banks. On the other hand SFB have a differential model which is retail and unbanked focussed.

The Business Standard report did not carry that, and if you can provide me a link…would be helpful to update my knowledge.

I have no idea, and if I may, I would assume that

- 50% of these exposures would be unrecoverable

- If management has provided specific provisioning against these exposures, then 50% of exposure minus such provisions for each of these groups, added up would be the total additional provisions that may be taken as the ‘loss given default’ for internal value calculations

- If specific provisioning is not given, then I would prorate the provisioning to these exposures and do step 2 above.

This approach is very conservative, and may well be questioned.

To be clear I do not own Yes Bank.

Thanks…Hoping that Asset sale (in case of reliance capital), securitization (for HFCs) may help in resolution and that final loss of outstanding loan amount is much less than 50%.

You did see 6 years down the line. Applause

4 Likes

@vicky_7900

In case of government banks they are asked to take hair cut because in future in need of capital it’s Government of India who brings it in

Private banks is a different affair all together. I think private banks will not take 50% loss. They will find some way out of this to minimise the losses.

And more over ADAG group will not be left without paying, it has to pay or its assets will be sold.

IDFC Bank has sold more than Rs 2,400 crore of stressed assets to Edelweiss Asset Reconstruction Company for Rs 622.6 crore, a loss of 75% on the exposure

Read more at:

//economictimes.indiatimes.com/articleshow/66438515.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

The net book value of the pool of 12 accounts for IDFC Bank was Rs 683 crore as it had made a provisioning of Rs 1,652 crore. The transaction that was completed in August led the bank to make a fresh provision of Rs 62 crore,