Yes bank has highest exposure to reliance cap debt, probably going to be junk. In coming quarters ADAG group alone will bring lot of pain to financial sector.

ZEE is also in line for YES Bank.

So

Zee, yes, dhfl, adag.

But yes bank is on sticky wicket.

It would be a surprise if they do not post another spectacular quarter like current one. It can be either q1 or q2 but it looks imminent

I see more pain or consolidation at lower levels for few months for Yes Bank. Management commentary is not encouraging. I see whole FY 19-20 is a cleaning up year for yes bank

Does anybody know how Moody’s arrived at the 8% stressed loan book figure?

Given the Essel and ADAG exposures, plus some smaller miscellaneous accounts, the stressed asset book is Rs.10,000Cr, which is what management had said. Where did Moody’s come up with another ~Rs.10,000?

A mysterious company with no operational business and fixed asset of 49 crore has provided corporate guarantee on behalf of a private defense firm to Yes and IDBI Bank for 1400+ crore.

2 Likes

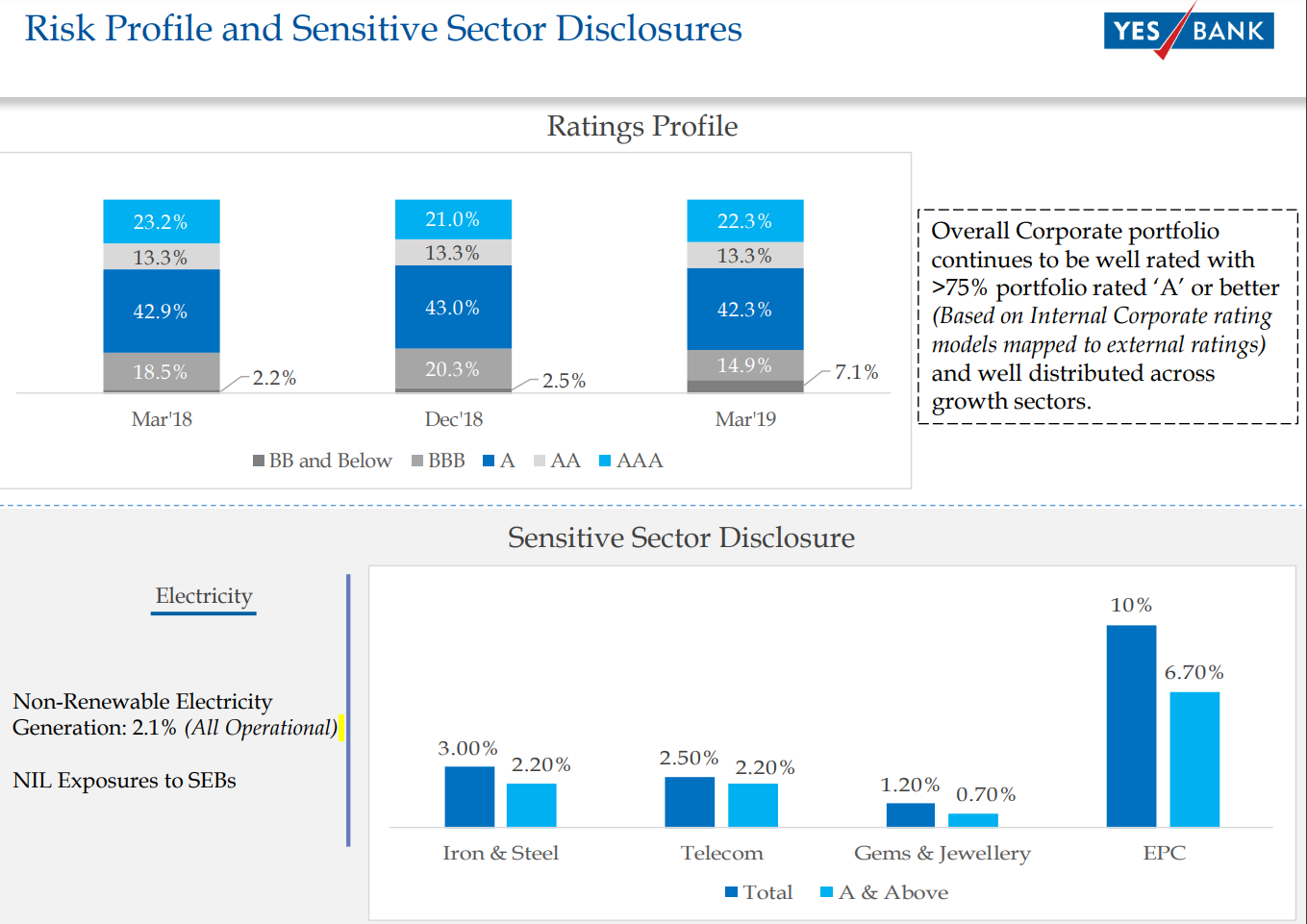

Yes Bank assets which are rated below A as per earnings conference call sectorwise :

NBFC : 0.87%

Housing Finance : 0.42%

Commercial Real Estate : 0.27%

EPC : 3.3%

Iron and Steel : 0.1%

Telecom : 0.25%

Gems : 0.48%

Total : 5.7%

Exposure to companies which have defaulted or near default :

ILFS : 2650 cr

R COM : 800 cr

Reliance Cap : 3340 cr

Jet Airways : 552 cr

Rel Naval : 485 cr

Essel group : 3300 cr

The data above are in public domain, I might have missed some as well,Yes bank total exposure to stressed sector is 35%, so Moody’s 8% stressed loan estimation seems ok.

Apart from above Yes bank has exposure to ADAG group other companies, DHFL, Indiabulls Group, and Sudhir Valia-promoted entities Fortune Financial Services India Ltd and Suraksha ARC which RBI was inspecting last year and could lead to worsening crisis.

11 Likes

Valuation is not an exact science. Its somewhat relative to what other companies in the sector are doing and how they are valued. So I will try to compare with Yes Bank, a PSU bank - Bank of Baroda. Both Yes and Bob has an MCap of around 40,000 crores at yesterday’s closing.I looked at Arihant Capitals latest report on Yes bank and Prabhudas Liladhar’s January report for BoB and the numbers below are from these reports. Other brokerages may have different numbers.

For FY21, this is what these brokerages are saying:

Metric Yes Bob

ABV 133 163

PAT(in Cr.) 3200 7066

NIM 2.9 2.9

GNPA(%) 3.5 7.2

NNPA(%) 2.0 2.2

PCR(%) 42.86 71.3

RoA(%) 0.9 NA

RoE(%) 9.3 NA

RoAA(%) NA 0.75

RoAE(%) NA 14.47

CASA(%) NA 36%

C/I ratio 47.2 45.5

I am not sure if these parameters are sufficient to draw a conclusion. After all there is a subjective part to all this.

First of all these are BoB standalone numbers and its getting merged with Dena and Vijaya Bank soon.

Secondly, there is the culture issue - an efficient private player versus a laid back PSU.

Finally, Yes also has a lead in technology, Credit cards etc over BoB.

However, BoB also has some great advantage.

First and foremost being their CASA which is similar to what Yes has but BoB only pays 4% on it where as Yes pays 7%.

Secondly, BoB’s worst seems to be behind us and their NPAs should fall now whereas for Yes NPAs are expected to peak in next 4-6 quarters.

Finally, BoB trades at 0.7 times its FY21 ABV while Yes trades at 1.4 times.

So my question is, on what basis does Yes deserve to trade at twice the valuation of a BoB? If one is taking a 10 year view, this may be justified but there is no way this can be justified over the next 2-3 year period. Even is Yes does everything right, I still would expect this valuation gap to close over the next 2 years.

Sorry for the formatting. Could not fix it in edit.

2 Likes

Its surprising to see a comparison of private and PSU bank, you are comparing apple to oranges and justifying as well. Problem is culture not parameters. Anything with government control will never find higher valuation. If things were so certain in stock market than you will never make money. Yes Bank has discounted IL&FS in full. Jet provisioning completed. ADAG pending for 800 cr, Zee loans will be paid once Dish TV deal will be completed with Singtel. Reliance Capital default is a very remote possiblity. Al in all 1200 from so called stress book is NPA. With ROA at 1%, still profit will be in range of 4000 cr for FY20 with GNPA and NNPA ratio to improve further.

3 Likes

It took 3-5 years for private bank like ICICI, Axis to clean up their books. So if not similar at least 1-2 years pain will be there.Yes Bank new management themselves have come forward and said 6% of their assets are rated below A. They have put 10,000 crore in watch list. Moody’s expects 8% stressed loan. Axis Bank actual slippage came 1.2 times the original guidance, so improvement of GNPA isn’t near.

Regarding Reliance Capital they have net 11 crore in cash,they need 2 billion dollars to save reliance capital. They were successful to monetize only 1/3rd to what they had planned for last year,now the only hope for them is Nippon buying out Rcap in Reliance Nippon Life Asset Management, and with this deep in crisis wont get good valuation. So likelihood of Rcap turning bad is very high With $252 million of debt falling due by June.

Yes Bank had been very aggressive in lending to corporate in past which was clearly visible in the growth and the profit, but as in financial sector profits are front loaded, now is the time for NPA.

3 Likes

1 Like

This author looks like paid by some brokerage house to write all negative. One example. Next year projected provisioning is 3500 cr, 750 cr/quarter, NII is 2500 cr/ quarter. Even Yes will provide 1000 cr/q profit or book value should be raising by close to 12 rupees, he is deducting and recalculating BV to 95, very low level of knowledge and baised.

2 Likes

Do you really understand the brokerage biz drivers? Do you think brokerages make money by giving sell calls? Their biggest interest is in persistent buy calls so that you remain hooked for double brokerages (buy and sell). Once you are out of stock, you no longer follow them that’s why they have more buy calls than sell calls any given point of time. When they give sell calls, one needs to think deeply since it signals that analysts have run out of excuses to give buy/hold calls. You are free to ridicule them but do it with fact and logic.

BTW capitalmind is not a brokerage as far as I understand.

7 Likes

ICRA downgrades yes bank and reliance Cap, next 6 months are crucial for financial sector as per Uday Kotak.

1 Like

Although its NOT related to yes bank, but as many posts have mentioned about reliance capital getting bankrupt. I understand that based on numbers its quite possible and specially given the current state of ADAG companies. Do we see possible ways of its revival (Mukesh can help, which he did once)? If Reliance Capital goes bad way, I am interested in understanding its impact on services / brokerage services provided by Reliance Securities (Reliancesmartmoney.com).

RCOM went bad way & customers had option/forced to move to other service provider, In this case brokerage services of RCAP (Reliance Securities) will be in question.

i) How does it impact retail DEMAT account holders

ii) Will customers be forced to move away (its tougher than changing mobile operator)

iii) Is there any risk to long term holdings

P.S. : Admins, please feel free to move / remove to correct thread, as it will help broader VPiers having demat with RCAP.

1 Like

There are threads for Reliance capital and ADAG group both. You need to post your queries there.

Yes Bank has approx 13000 crore exposure to ADAG group.The 10,000 crore watch list (which includes part of ADAG group, Omkar group and Essel group) is in addition to 7882.6 crore Gross Bad Loan identified so far.

A big difference between ICICI and Yes bank is quality of subsidiaries and quality of retail customer profile . This helped it to raise capital through IPO route and finance itself through tough times

When RK was @ helm he was smart at story telling and presenting figures so he could raise capital @ high equity prices resulting in lower dilutions .

Now the management has declared huge NPA and lowered share price , now if wants to raise capital say through QIP etc it will lead to higher dilutions like it happened with many PSU banks . That is not good for share price in long run .

5 Likes

Basic Nature remain same. Rana or Post Rana