For any bank, it’s the strength of pre provision profits which matters the most. Yes Bank has had strong 25%+ CAGR from 3K to 7.7K crore in Pre provision profits in last 4 years and expected to continue having the same.

As for the elephant in the room, the looming NPAs and their underreporting. I expect Yes to have some quarters of extraordinary provisions to cover for these NPAs and comply with RBIs definition. This will mean erosion of capital as well in order to shore up which it’ll need to raise fresh capital from marquee investors.

The sooner it raises capital the better and the price at which that capital is raised will also affect the stock price.

In order to raise enough fresh capital, RK perhaps will need to send some strong signal to the market by maybe selecting a capable CEO well versed in the business of which I’m sure there is no dearth of both inside and outside the bank.

That CEO will have his hands full in the sense that he’ll need to convince investors for raising capital and start showing some tough love towards the stressed assets by making enough provisions for them ultimately preserving the BVPS.

Quantum of capital requirement will depend on the NPA figure declared by RBI in its audit.

For me YB becomes a great buy as soon as RK is out from the board and the mgmt team. I won’t look at price levels at that time except that it has to be below 2x P/B for me to buy. It will signal significant easing of uncertainty and probably a new beginning.

Divergence for 2016 was ~4000cr

For 2017, after 50% growth was ~6000cr

For 2018, assuming another 50% growth, let’s say it’s 9000cr.

On this 9000cr if they have a 60% pcr, provisioning requirement becomes 5400cr. Let’s say that they would have taken 1700cr provisions/write-offs on these assets even without qualifying these as NPAs. So additionally they would have to take (5400-1700=)3700cr provisions, which is about PBT (profits before tax) of 2 quarters.

Does anyone on the forum have or is able to find out data regarding institutional buying/selling that may have happened yesterday? I did my own digging but the sources didn’t seem too reliable.

Can we consider that UBS might have insider info or strong sense about denial of RK extension and seriousness of issues at YB ? When they given 170 as Target price most of the ppl thought it’s might be biased due to their fight with YB but now it’s seems that’s going to be possible.

Disc: Invested recently and looking forward to add more in view of 2-3 yrs term.

ICRA has reaffirmed the ratings on various borrowing programme of Yes Bank Limited (YBL); the outlook on long term ratings has been revised to stable from positive. ICRA hasreaffirmed rating of [ICRA]AA+ (pronounced ICRA double A plus) for the Rs. 2,530.60 crore Basel II compliant lower tier II bonds and the Rs. 7,030 crore infrastructure bonds and the ratingof [ICRA]AA (pronounced ICRA double A) for the Rs. 1,544.10 crore Basel II compliant upper tier II bonds and Rs. 461 crore Basel II complaint innovative perpetual tier I debt Instruments of the bank. In addition, ICRA also has reaffirmed the ratingof [ICRA]AA+ (hyb) (pronounced as ICRA double A plus hybrid) for the Rs. 10,900 crore Basel III Compliant Tier II Bonds and the rating of [ICRA]AA (hyb) (pronounced as ICRA double A hybrid) for the Rs. 10,800 crore Basel III compliant additional tier I bonds. ICRA also has reaffirmed rating of [ICRA]A1+ (pronounced ICRA A one plus) for the Rs. 20,000 crore certificate of deposit programme and the short term fixed deposits of the bank.

thanks a lot for the info. There isn’t any buy/sell data, however, on YB. Does that mean there was no institutional purchase/sale in it yesterday?

I can understand the lack of a purchase. People would want to wait for the price to stabilize and also for the outcome of the upcoming board meeting before they take a call on whether to purchase or not. However, the lack of a sale by institutions yet could be a little heartening.

Reading the replies in this thread, I remember an old teaching by an old investor long back.

He told when your own work is not good, every uncertainity you face in the market, you will look for a justifiable excuses.

Problem with yes bank holders is they have done no study of the bank accounts for last 10 years.

Now blaming on RBI, RK exit and all.

Exits come and goes, businesses stays. Study what the business is worth. Its hard earned money be very sure where one is putting.

Surprisingly , no funds name appearing in block/bulk deal…As per latest shareholding pattern around 20.50 crore shares with retail investors and total delivery 11 crore shares. Is retail shareholders sold in panic??

Yesterday was to be the board meeting. Does any investor friend has an update on that?

What all weak governance and weak compliance encompass will have to be seen. It looks pretty certain that stock price will see some more downside. Will it go down to levels of Rs 170?

Read about a recommendation after the fall on 21st with an upside of 65 - 70% by FY 21.

In Yes bank’s case,the RBI has reported a divergence in NPA for 2016 and 2017, however has the Yes bank changed their NPA or provisions? Does that mean that Yes bank is contesting with the NPA numbers reported by RBI?

Is there a transparency in the NPA numbers reported by RBI for Yes bank or other banks?

If RBI comes up with NPA divergence for HDFC bank ,may be after two years,who we all agree is the most transparent and loyal bank(take this with few spoons of salt) …should we believe that HDFC is also reporting incorrect numbers?

As long as the transparency of RBI is not clear , I believe retail investors are only playing a 'guessing game ’ and our ‘ownership bias’ plays enough role to hold the Yes bank

I have not thoroughly analysed if the performance of Yes bank has deteriorated after this ‘NPA divergence’ issue came into light last year . I know that the Market cap has surely come down,how about the other operating factors?.Can any of the seniors look into this?

I am a very newbie retail investor struggling to understand the honesty of reported numbers in various scripts.

For some strange reason, nobody in media & sell side is highlighting the impossibility for @yesbank to get an insider or outsider to succeed Rana as it requires both warring promoters to recommend the individual.

Hemindra Hazari added,

Andy Mukherjee @ andymukherjee70

Plus some inter-promoter agreement needed for executive directorship of Yes, @dugalira ? I saw @HemindraHazari ’s note on that. Feuding promoters could complicate that? https://twitter.com/dugalira/status/1042979668943499264 …

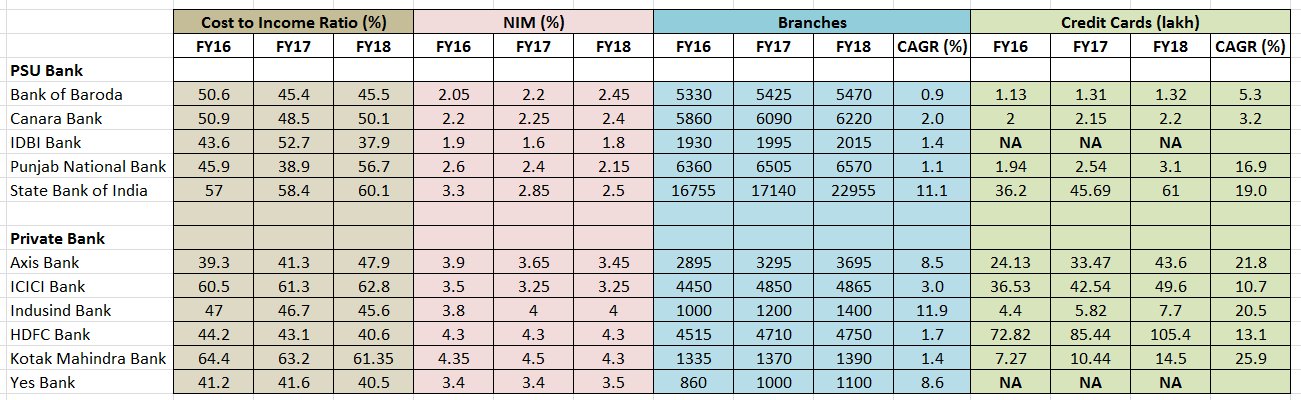

On all parameters Yes Bank has had a splendid run.

Wonder if it’s a case of over done panic.

An August 8 report of the RBI had noted Yes Bank’s performance was better that most private sector banks. The division had recommended re-appointment of Kapoor as MD & CEO for 3 years. Industry insiders believe it could be a case of vested interest that could have played a role in Rana Kapoor not getting an extension.

Could it be that there’s more to this saga than that meets the eye?

Secondly, wonder who sold the shares on Sep 21st. There’s no data on Bulk deals of any Fund house dumping the shares. Can we write to SEBI with a complaint on price manipulation ?

Hemindra Hazari @ HemindraHazari

Hemindra Hazari @ HemindraHazari