This is absolutely right. I second it. I’ve seen same behaviour in case of MGL (invested) when one of the promoters sold recently because of its own reasons.

More important than anything else is how investors behave during times of crises. People who jump ship at the first instance of a problem/crisis will never make any substantial returns. As Buffett says, be greedy when others are fearful. Fear is what i see here on the forum. Yes, banks, either public or private, are beaten down due to lots of issues - NPA underreporting, evergreening of loans, leadership instability, corruption allegations and more. But this is what happens when a lending cycle turns. People find out all the loans they made during boom period are not going to be paid back because businesses are not earning. They then resort to all these unethical practices to save their heads which now the regulator is attempting to correct to good effect. Doesn’t mean the whole institution is a fraud or is irredeemable right?

Financial institutions in the US should be an eg. These institutions participated in unethical transactions related to housing mortgages. Even credit rating agencies had a role to play.

But did Goldman Sachs die after 2008? Or any other institution apart from Lehman and Bear? They had to pay fines, do less business because of more regulation but the biggies survived. Many are bigger than their former selves. And they’re again well to do with the US economy firing on all cylinders.

I look at crisis as an opportunity. Such events happen with the most ethical, most efficient of organisations but then things change, times change, people change, laws change and things start to take a turn for the positive. I remember a dialogue in a Keanu Reeves movie : “It is only at the precipice that people change.”

Tough times afflict every company, every industry and these times test investor patience and conviction. And it is only those investors who know how to make good use of rare opportunities who make above market returns.

I think there are enough tailwinds for the sector and Yes Bank is a well placed institution to make good use of those tailwinds. In my opinion, these times of crises are temporary as the issues with the bank are resolvable and promoters have a significant skin in the game to let the institution suffer and eventually die.

While looking at yes bank, one would need to be honest in asking what the crisis is?

Rana kapoor exiting in 2019 jan?

If one feel that is an issue, why? Banks do get new heads. So this is not an issue.

Now to NPA, banks by very nature of its business, they lend many X to their asset. So the value or moat of the business remains in quality lending, where the lent out money can be recovered.

A small default can erode the asset on books drasticaly.

If any1 who read last few year annual report and auditors report, they could easily figure out, which company have they lent to and how much is exposure to many bankrupt companies.

Its not just reliance Naval, but few others.

They have failed to classify such accounts properly to NPA. Also one would check various accounts under restructure loans. See the status of such companies, whats their status?

Being a corporate lender has its own pro and con.

Guessing how big the elephant in the room is vague.

Or thinking it is jus a cockroach and market has discounted it is also vague.

Let the devil be out, see the market response to it and decide.

Eventualy trust ur hardwork, study it, than just guessing and self comforting with all is well.

Lehman had the most exposure to mortgage backed toxic assets out of the bunch. It’s CEO was a highly disliked & arrogant one I read in reports at the time, so nobody wanted to work out a solution with him (in contrast to RK who is widely respected across the industry, even NDA ministers visit his house). US govt had to set an eg, In India, if any bank should be allowed to fail it should be banks like PNB or a dozen other PSBs.

RBI is already setting an eg. in India by declaring divergences, making banks acknowledge bad loans sooner, ousting bank CEOs, govt merging bad banks with good ones & more concrete steps. These are going to help resolve current issues as well as make sure they don’t happen again.

And even if RBI found out divergences in Yes Banks NPAs, they were later upgraded to standard accounts or sold to ARCs right?

Money control view Investors will have many more questions till the dust settles. In the interim, the stock is expected to remain volatile with a downward bias. Investors should exercise caution and shouldn’t bottom fish in a haste till clarity emerges on the quality of its books.

yeah…awesome panic moments…

i have a simple logic…BVPS for the previous year was 111.85

If we reduce 8.7% of it as NPA. it becomes 102.11

Assigning a PBV of 2.5 will give us a price of 255

This figure of 8.7% was calculated earlier when there were news of power sector companies going bankrupt…

Bought 80 shares at 254

yeah …morning star is showing leverage as 12…however lets talk even simply…

The total book value of yes bank stands at 23790 cr

Washing of book value by 8.7% will mean a reduction of 2069.77 cr…

Are we actually looking at a reduction of 2069 cr from book value…

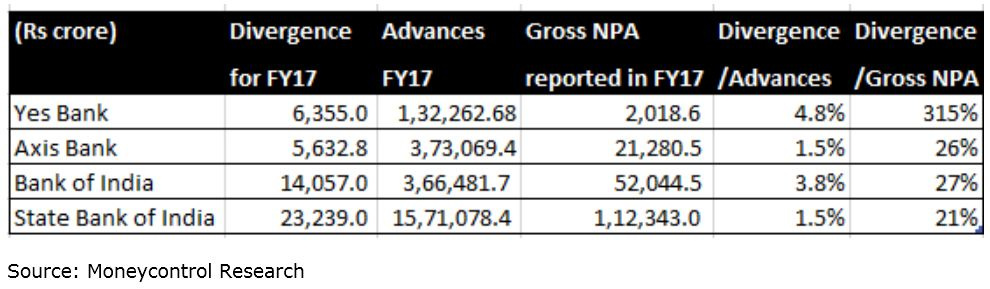

Divergence for fy 17 was 6335 cr…

what does that mean…can there be a washout of 6335 cr from its books…that will be 26% reduction in book value…

im not well versed with the calculations…but we need to calculate the worst possible scenario here

It’s 10X leverage so if NPA 10% which can get zero recovery in that case technically it will be close to bankcrupty situation.

Plo note that it’s a what if scenario only.

%age of NPA is to be calculated on Loan Book not Book value. Loan book as per this presentation made on 29-08-2018 is Rs 203500 cr. 8% of this will be Rs 16300 cr about…

Which means the net book value will be about Rs 7500 cr.

it means, if i want to justify a price of 255 at PBV of 2.5, the capacity of the bank to absorb addl NPA remains onlt upto 2000 cr which is approx 1% of total BV…

Thanx a ton for enlightening me Varun…i have exited my position without any damage…

I hope you took into consideration that calculations were based on 8% NPA without recovery before making your own decision.

I also think it is better to wait and watch. I have some shares currently looking at a huge loss. Not adding as of now. Will wait for the outcome of the board meeting on 25th.

IMHO, Yes Bank’s biggest strength is its recovery mechanism, which I am not too sure the RBI takes into consideration too much. Let’s see how this pans out. I’ll give Yes Bank a year as usual.