Hi

Q. What is the conclusion we are trying to make?

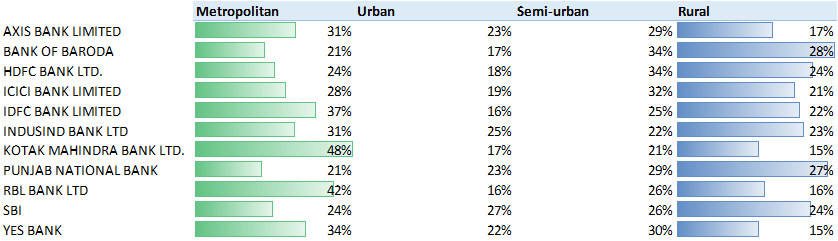

So do all the other banks. 6 out of the 11 mentioned above have more branches in Metros. RBI classifies branches into 4 types based on population - Metro, Urban, Semi-Urban and Rural. This includes the relatively ‘loved’ KMBL, IndusI & RBL.

So do all the banks. Have a look at the average balances across population groups below. Not just coprorates but key salary accounts.

Q. They are doing reasonably well on what terms? Have a look at the table below.

HDFC has 7% lower Semi urban branches from national average and a 15% lower than the Rural average.

KMBL is 14% more than YBL in metro and same in Rural.

I had earlier this year shared some inputs on this topic in @Yogesh_s 's thread on Indian Banking.

All relevant data points below. Some are slightly old as DBIE doesnt have live data.

No bank is doing social service by opening branches in Rural India. It is a mandate of how branches are to be opened by RBI. All banks including the haloed ones use loopholes in selecting locations. Lets not get into that part as it is a grey area.

My other point is lets make statements with data backing else we can put a disclosure that this is my ‘hunch’ or ‘guesstimate’. Cheers.

Rgds

Deepak