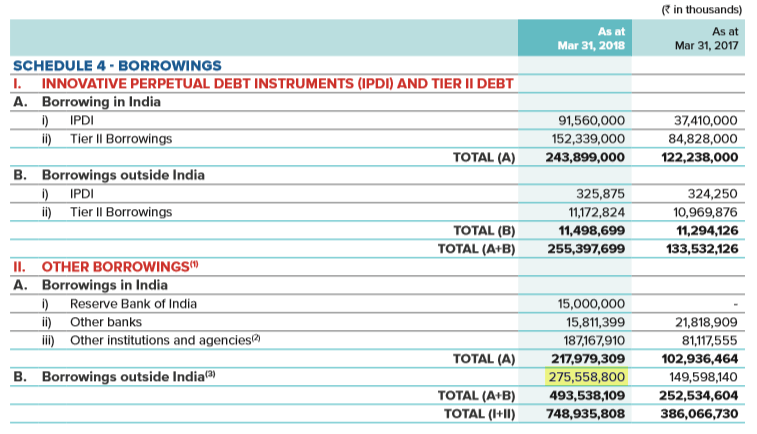

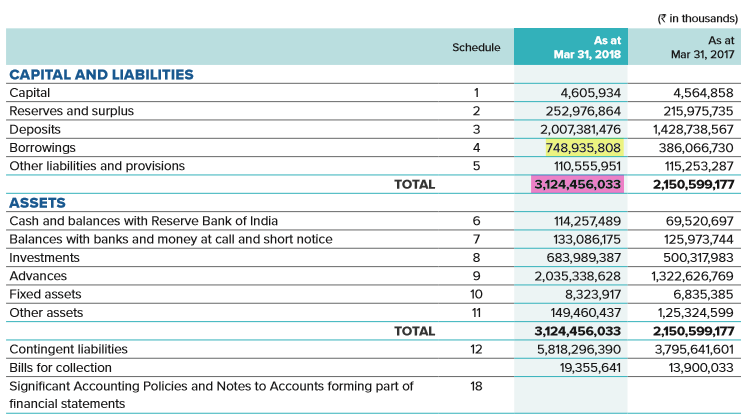

Yes Bank has borrowings outside India of INR 275 mil out of a total borrowing of INR 749 mil and a total balance sheet size of 3124 mil.

Source Annual report 2017-18

Source Annual report 2017-18

Foreign borrowings are a sizable part of total borrowings but only about 8% of balance sheet size. A debt downgrade will cause borrowing costs to rise but banks in India generally mark their loans in such a way that they can pass on some of the borrowing costs to their borrowers.

There will be a moderation in growth, but I don’t expect the balance sheet size will reduce. cost of deposits are not likely to go up going by the experience of other banks. PSU banks with huge NPAs haven’t seen any increase in their deposit costs. These continue to get deposits at competitive rates.

Promoters are working on settling their disputes and I think they will come to some kind of agreement in the next 2-3 months (may be even before the next board meeting) so that they can agree on a new MD and get RBI approval. Once the new person takes charge we will know if there are any bad loans in the closet. Market may be worried about that.

To me Yes Bank is what Mohnish Pabrai calls high uncertainty low risk case. However, market generally equates uncertainty with risk so it is pricing high risk scenario.