why the message is flagged?

Accident / reputation damage is an inherent risk in this business. However, June-end incident could have been handled well by the management in a proactive way. I meant the press handling part.

Wonderla Holidays AR 2019 notes

Annual report this year was a good read. Management giving credit of good performance to employees is always a good thing to read. Good initiatives taken during the year to increase repeat customers. Rationalising the marketing expense by focusing more on online and digital advertisement. Company doing a lot of little things right like Loyalty Programmes, Focus on F&B vertical, new resort planned in Hyderabad. This year growth in Profits was mainly due to reduced expenditure but there is a limit to which the expenses can be brought down. Going forward growth has to come from visitor growth. This year Kerela numbers were down by 14% due to floods, this should reverse this year and this alone should bring 4-5% sales in growth and higher growth in profits. Company had good cashflows of approx Rs. 90 cr. and without any major capex balance sheet looks quite strong.

Key Points

- 3 amusement parks. 1 three star leisure resort. 162 rides. 15 restaurants. 84 luxury rooms. 4 banquet halls.

- No. of Visitors (no. in lakh) Total: 25.23 ( in fy18: 24.87)

Bengaluru: 10.57

Kochi: 7.57

Hyderabad: 7.09 - The turnover of the Company increased to

29,165.70 Lakhs compared to27,834.06 Lakhs in 2017-18.The net profit after tax is5,541.41 Lakhs (3,850.39 Lakhs in 2017-18) and earnings per share is9.81 compared to6.81 in 2017-18. The Company is debt-free at the end of the year, except for working capital finance of ` 98.66 Lakhs. - The overall revenues grew in FY19 backed by a growth in footfalls and substantial contribution from our non-ticket business avenues. We have seen higher margins this year which were driven by cost efficiency measures across all locations and personnel.

- Footfalls in Bangalore and Hyderabad park grew by 10%, whereas Kochi recorded a fall of 14%.

- Compared to previous year, 9% growth in Non ticket revenue was recorded which is driven by 21% growth in F&B and 4% growth in sale of products.

- Revenue from Resort has grown by 6% to

1,155 Lakhs as compared to1,087 Lakhs in FY2018. -

Chennai Project - As reported last year, your Company along with other Industry members, has been following up with the Government of Tamil Nadu to remove the local levy of 10% on admission fees to the Park. Although the Government had agreed to issue a notification in this regard, we are still waiting for their formal decision on the same. This has held up investment of

350 Crores in our Chennai project. Once the local levy is withdrawn, we expect to complete the project within two years. As you are already aware, our next destination is Chennai and we have already bought 64 acres of land and invested close to105 Crores till now in the new project. - We have also shifted from a franchise based model to an ownership model for our restaurants. This has further helped us to improve operational efficiency and exercise better control on our F&B range.

Further, we have started moving towards a centralized procurement process for our F&B division to bring in economies of scale and reduce the procurement cost - Operational Review 2018-19 was a very challenging year for us as we dealt with unfavourable weather conditions and State-specific issues including strikes, elections and virus outbreak. However, despite these challenges, we were able to increase our footfall and revenues. This could be achieved through several initiatives taken by the Company to enhance market penetration, improve operational efficiencies, leverage technology and deliver a better experience to the customers.

- A cashless wallet based payment system has been implemented in Bangalore and is running under pilot in Kochi.

- Online ticket booking platform and strategic alliance with the leading online portals has generated 33% increase in online booking.

- A resort similar to the one in Bangalore is being planned in Hyderabad. In the meanwhile, we will look forward for meaningful partnerships with star hotels in Kochi and other future park locations for enlarging our offer for ‘Stay & Play’.

- We have also introduced Wonder Pass, a loyalty program, which gives deep discounts to loyal customers. With this initiative, we expect to increase our repeat customer base significantly. Our WonderPass loyalty programme received tremendous response with 31,000 passes issued in total since its launch in September. As it has a 2-year validity, we anticipate an improvement in the turn-around time on repeat visits.

- Reduction in expenses was mainly on account of

Reduction in Rates & Taxes to Rs. 5.36 cr. from Rs. 17.21 cr. yoy.

Reduction in Employee Cost to Rs. 38.10 cr. from Rs. 41.61 cr. yoy. - As part of transition to IndAS accounting and compliance, the Company had revalued the freehold land across all the parks to the extent of ` 304 crores net of applicable deferred tax.

- In August 2018, Kerala suffered its worst monsoon in more than a century which resulted in one of the worst floods in recent history. The damage wreaked by the calamity is estimated around $2.7 billion. Fortunately, our park did not sustain any material damage.

- According to Indian Association of Amusement Parks and Industries, “The Indian amusement and theme park industry is expected to grow at a CAGR of more than 25% with the annual revenue of at least ₹6250 crore ($884million) by 2022”

Regards

Harshit Goel

Biggest risk in this business is such incidents (this is not in Wonderla)

Yes maintenance and regular testing are definite needs for such rides in parks. Have seen in some of the parks in Singapore / US, where they actually stall the queue (even if it is peak season / peak hour) to do the test rides. Also they use multiple cars / carriers for the roller coaster rides and keep alternating or changing them after a few rides for maintenance. Safety is paramount in such scenarios. Not sure if the Indian parks follow these measures strictly - especially during peak hours (if revenue takes precedence). Probably it should also be mandated that some faq section is available for various safety measures undertaken for better disclosure and providing confidence to the general public.

Some measures as given in Wonderla AR (Risk Management Initiatives), though they don’t talk about intermittent checks during a day -

4. All rides are subjected to daily pre-opening check as per a comprehensive checklist.

5. There is a detailed monthly check of all rides.

6. There is a detailed shutdown and overall maintenance of all rides periodically. All critical parts of the rides are periodically subjected to a non-destructive test (NDT).

7. Authorised external agencies like T.U.V Germany are engaged to periodically check our rides and ensure compliance with the safety protocol.

why is wonderla falling continuously from 300 odd levels till recently to 247 today , could somebody confirm? any specific news?

an over hyped stock with high valuations is normalizing that is all.

Hi Venkatesh,

Please help me to find out how to calculate the valuation for this company.There are some peers like Nicco park and Adlabs,but comparing the fundamentals it seems wonderla is decently valued with good potential.

Thanks,

Deb

Company was overvalued . Plus new risks like lack of water in Bangalore , lack of water in Chennai , accident risk etc are emerging

I considered this as an opportunity to add this as it was in my watch list. Now PE, PB wise cheapest since listing

Disc: 1.5% of PF at average cost of 267 and looking go add more if corrects more.

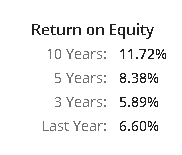

Company RoE is not even equal to cost of equity. Why should this trade at more than book value? March 2019 networth is Rs819crs. The stock looks expensive trading at a market cap of Rs1404crs. Its a tough business which is obvious from low RoEs of the business. If it had a moat RoE would have been higher.

In next Conf-Call ask management about total number of rides they have (currently 160+) and total TUV approved rides, based on my experience with certification agency like TUV, there might be a chance of around 50%-60% rides (or even less) are complying to TUV requirements.

Disc: No Holding.

Valid Point. But if chennai park starts which has been delayed a lot would increase the ROE.

RoE looks depressed due to IndAS adjustment. Land Bank is recorded at fair value thus Equity is inflated leading to lower RoE numbers. Moreover in the last 2 yrs the empty land for Chennai Plant is understating the RoE and RoCE. Otherwise its roe and roces are best in industry

That argument does not make sense from a valuation perspective. If IndAS has inflated networth which deflates RoE, it has also inflated book value when you value using P/BV. So you get benefit of inflated book in pbv valuation

Secondly industry leading RoE is not a valid argument to justify an expensive valuation. It is possible that entire industry needs to trade lower if RoEs are so low.

Has company already done capex on Chennai. How much have they špent till date.

total 350 cr capex for chennai as stated by management

Refer to Harshit’s post which has captured this info. just few replies back.