Even in their parent company MF holding is less.

Wonder why?

Plus entire green energy space has relatively less MF holding.

Perhaps MF industry is skeptical about the hype of alternate energy and perhaps they assume lots of company post saturation in this field will bite the dust, just like many tech company in dotcom and may players in telecom .

Perhaps there are lots of players evolving in green energy and it’s hard to take a guess which ones will succeed and which one will falter.

To me the Mutual Funds not holding may not be such a negative factor. Afterall, an elephant or a whale takes time turning around.’ If your only reason for picking a stock is that an expert likes it, then what you really need is paid professional help.’

Peter Lynch

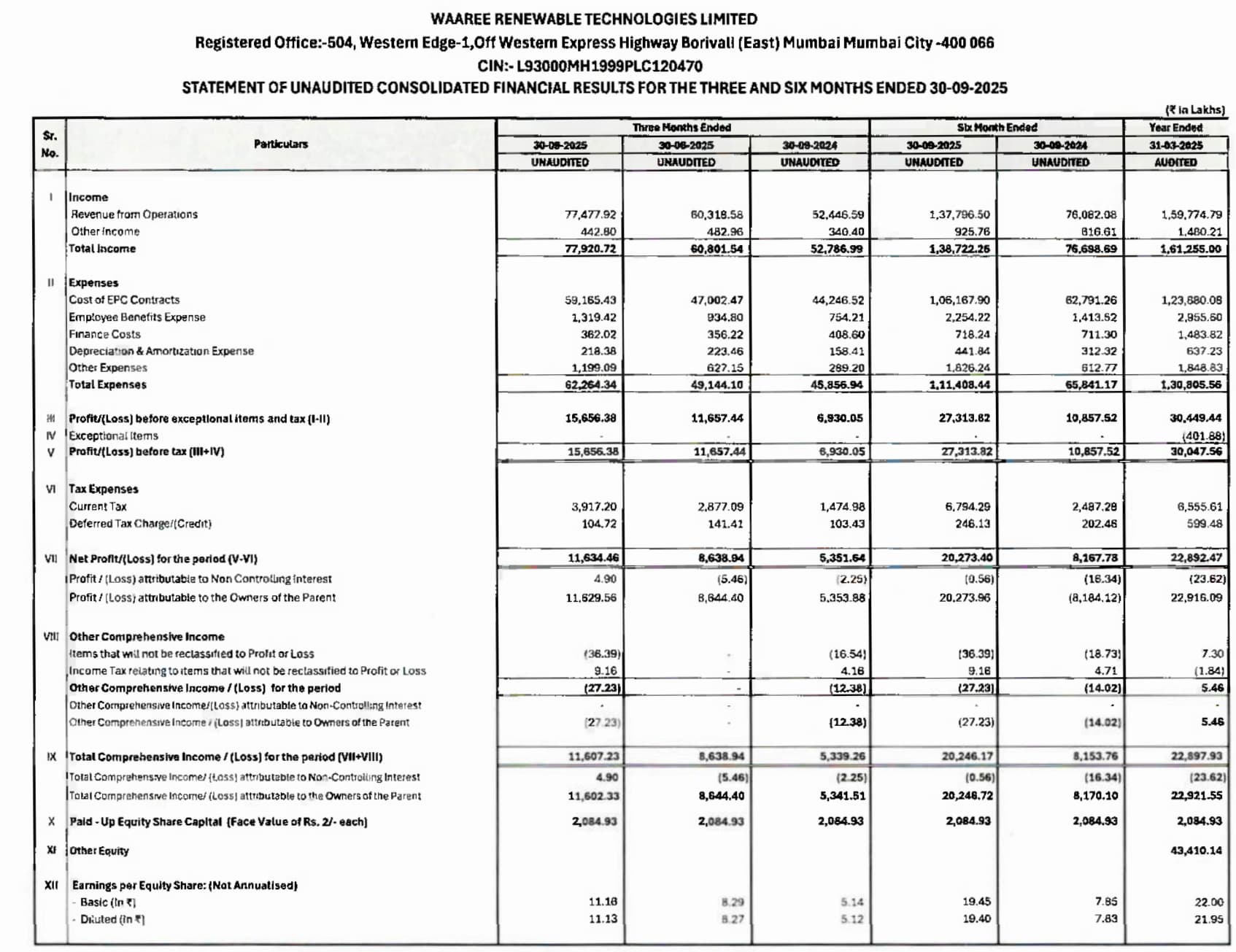

Both the Waarees have fallen a bit from their 52 week highs. Renewable has fallen 68.74% as of today. The stock’s PEG is .22, which, to me makes it awfully attractive.

The screener does not give PEG of Waaree Energies. However, this too has fallen 35.04.

The valuations in these stocks were sky-high, so selling by the MFs would seem to be justified.

Now, if they have fallen due to Trump’s policies or due to competition hemming them in, I would be really concerned.

MFs were not holding it anyway, so they didn’t sell anyway.

Valuations were uncomfortable at 2500-3000 odd levels. trading at 100 trailing PE.

Trump is a factor as he is not in favor of green energy in general especially in form of wind.

That is one factor that has damaged the mood in renewable energy stocks this being one of them.

However I believe this could be really attractive at current valuations, if they continue delivering kind of the growth the did in past few years.

Comparing it with adani green, I find valuation comfort here

But comparing with KPi green , I think that’s rather more attractively valued .

Since KPi greens last quarter wasn’t as bad as warrees , but koi has significant promoter stock pledged

I have a bookeeping question. As mentioned in Para 4 under Notes to A/c (Q4FY25 Result), the company capitalized and amount of Rs 11.63 cr paid as GST after receivng notece from the authority. Earlier they claimed this amount as ITC, but authority said they can’t claim it as ITC. Subsequently, the paid the amount as GST but instead of showing it in P&L account they capitialized it. Is not this a sign of fianacial shenanigans?

As per the explanation given in the results,

“In FY23 & FY24, they were executing solar power projects at multiple sites for their customers. However, due to the cancellation of the LOA from a customer, it was decided to use this asset for their own IPP asset portfolio. While executing solar projects, the ITC on purchase was availed. During February 2025, the GST investigation team visited the office premises. Basis the discussion with the GST authorities, the Company was informed that ITC in the above projects cannot be claimed as Input credit. Consequently, the company paid GST liability (capitalised during the year) for Rs. 11.12 cr along with applicable interest (shown as an exceptional item) of Rs. 4.02 cr. It is pertinent to note that as of the date of the meeting, the Company has not received any formal order from the GST Department for the above.”

The GST was originally claimed when the project was for a customer. When the asset became part of the company’s own operations, reversing the ITC and capitalizing the GST would be a correct approach.

Please feel free to correct if I’ve misunderstood or missed anything

Waaree ren awarded Letter of Award (LOA) for the execution of Engineering,

Procurement and Construction (EPC) works of solar power project including Operation and

Maintenance (O&M) of 94 MW AC/131.6 MW DC capacity. This project will be executed

under Mukhyamantri Saur Krushi Vahini Yojana-2.0 (MSKVY 2.0) (src: https://www.bseindia.com/xml-data/corpfiling/AttachLive/1adb6379-353e-4ef7-9e72-e49e931ff1b6.pdf ) . Order value approx INR 114.23 Cr. (Excl.

Taxes)

Thanks for your reply. I was thinking on the lines that under IND AS 16 (PPE), the cost of an item of PPE includes any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating which includes non-refundable taxes (like GST that can no longer be claimed as ITC)

In this case, since the asset is now part of the company’s IPP portfolio and not for sale, the GST paid becomes non-recoverable and is therefore capitalized as part of the cost of the asset. Had this project remained for a customer, the GST would have been recoverable as ITC, so it wouldn’t be capitalized, making the treatment consistent with IND AS 16

It does inflate profit initially (vs not expensing to P/L). However, over time, the cost will hit the P/L through depreciation.

It may not be a case of financial shenanigans. Nevertheless, please feel free to point out if I have misunderstood or missed anything

Waaree Energies announces major capex plan of expanding BESS from 3.5GWh to 20GWh & Electrolyser capacity from 300 MW to 10000 Mw for a total capex outlay of Rs 8,175 cr. Any idea will it get routed to RTL?