Hi …Any views on Waaree energies . It is currently trading around rs 2000 in unlisted market ? is current valuation worth investing , considering it has almost 75% holding of Warree renewables ?

Would you know what are its sales, profits, debt levels? And are they converting profits to cash? Ravi Dharamshi did take a stake sometime ago in it.

1 Like

Very good article on WRTL by moneylife explaining multiple facets on why they command higher margins and lean WC among EPC players and how they are uniquely placed among private IPP players. They are also very cautious on valuation front like everyone.

Disclosure:Invested before the run up and holding nervously

10 Likes

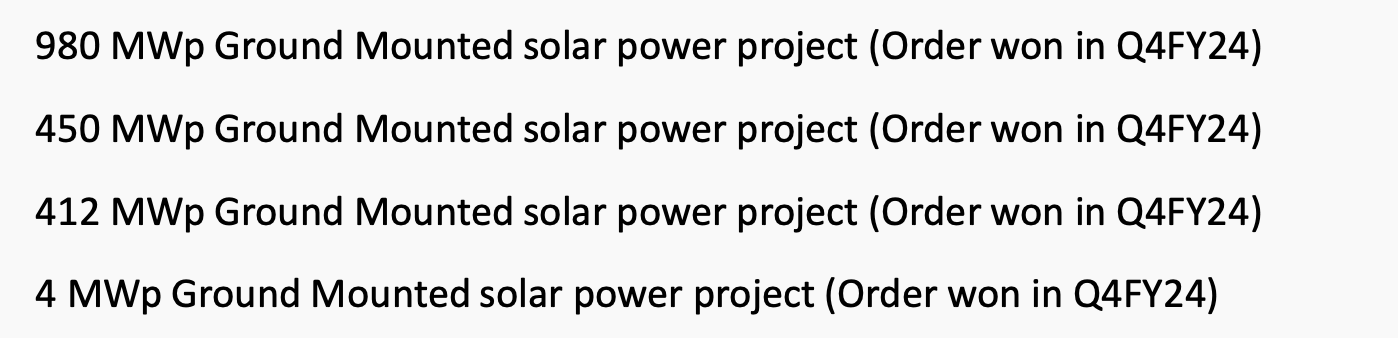

Waaree has come out with FY2024 results

Interestingly it has maintained EBITDA Margin.

Also Q4 was pivotal in terms of order wins

Completed Year with a solid Orderbook of 2.3 GW

Source: Investor presentation

4 Likes

Financial Highlights (as of March 31, 2024)

- Standalone Financial Results:

- Revenue from Operations: ₹27,054.19 lakhs for Q4 2024; ₹86,736.13 lakhs for FY 2024.

- Total Income: ₹27,294.07 lakhs for Q4 2024; ₹87,548.87 lakhs for FY 2024.

- Profit before Tax: ₹7,151.06 lakhs for Q4 2024; ₹20,029.00 lakhs for FY 2024.

- Net Profit: ₹5,278.74 lakhs for Q4 2024; ₹14,893.57 lakhs for FY 2024.

- Earnings per Share (Basic and Diluted): ₹5.07 for Q4 2024; ₹14.30 for FY 2024.

- Consolidated Financial Results:

- Revenue from Operations: ₹27,324.76 lakhs for Q4 2024; ₹87,643.86 lakhs for FY 2024.

- Total Income: ₹27,458.50 lakhs for Q4 2024; ₹87,988.53 lakhs for FY 2024.

- Profit before Tax: ₹7,154.37 lakhs for Q4 2024; ₹19,840.89 lakhs for FY 2024.

- Net Profit: ₹5,418.45 lakhs for Q4 2024; ₹14,804.08 lakhs for FY 2024.

- Earnings per Share (Basic and Diluted): ₹5.20 for Q4 2024; ₹14.22 for FY 2024.

Dividend Declaration

- The Board of Directors has recommended a dividend of ₹1.00 per equity share of ₹2.00 each for the financial year ended March 31, 2024.

Assets and Liabilities (as of March 31, 2024)

- Standalone Statement of Assets and Liabilities:

- Total Assets: ₹69,601.98 lakhs

- Total Equity: ₹25,935.54 lakhs

- Total Liabilities: ₹43,666.44 lakhs

- Consolidated Statement of Assets and Liabilities:

- Total Assets: ₹71,402.02 lakhs

- Total Equity: ₹23,202.88 lakhs

- Total Liabilities: ₹48,199.16 lakhs

Cash Flow Highlights (FY 2024)

- Standalone Cash Flow:

- Net Cash Inflow from Operating Activities: ₹11,753.13 lakhs

- Net Cash Outflow from Investing Activities: ₹11,527.69 lakhs

- Net Cash Inflow from Financing Activities: ₹422.96 lakhs

- Consolidated Cash Flow:

- Net Cash Inflow from Operating Activities: ₹12,679.56 lakhs

- Net Cash Outflow from Investing Activities: ₹11,398.02 lakhs

- Net Cash Outflow from Financing Activities: ₹648.03 lakhs

Key Announcements and Notes

- Amalgamation: Approval by NCLT for the amalgamation of Sangam Rooftop Solar Private Limited, Waaree PV Technologies Private Limited, and Waasang Solar Private Limited with Waaree Renewable Technologies Limited.

- ESOP Grants: Issuance of 97,910 options on 22-07-2022, 17,820 options on 28-03-2023, and 10,810 options on 26-10-2023 under the Company’s Employees Stock Option Plan (ESOP) 2022.

- Share Capital Changes: The company has allotted 73,095 equity shares during the year, increasing the paid-up equity share capital from 10,40,74,170 equity shares to 10,41,49,265 equity shares.

- Sub-Division of Shares: Approved sub-division of equity shares from a face value of ₹10 each to ₹2 each.

Disclosure: Invested

https://www.bseindia.com/xml-data/corpfiling/AttachHis/d9aabcc4-17dc-4c11-9952-a52d7bc68e6c.pdf

4 Likes

Hello.

I am posting here since no separate company thread and group company.

I have been told that Waaree Technology is building a 2GW BESS plant. Since it’s yet to start production, results are poor.

Where to find this info?

IMHO, It should reflect in CWIP.

Can anyone point me to right resource?

Thanks in advance.

2 Likes

2 Likes

order book 3,200 CR which is sitting on the books then there’s an pipeline of 13 gwatt that we are already discussing with our customers even combining these two and you know you put a conversion rate of 30 to 40% .

2 Likes

Hi,

I am tracking waaree from last 1 year, many times feels like to take a position for long term, Any views?

This stock is falling tremendously for the last few days. Can we assume that now this sector is out of flavour ?

Sector is not out of favour yet. Waaree Renewable price had run up to unsustainable levels, a correction was unavoidable. Company have healthy order book (3200 Cr) and is aiming to grow it’s revenue by three fold by Fy 25 according to CFO. ( https://www.financialexpress.com/business/industry-waaree-renewable-eyes-threefold-growth-in-fy25-3495071/)

1 Like

There are several truisms related to equity market that are universal in nature. One of them is “what goes up must come down and vice-versa”, all other things being equal. A variant of that is “what goes up harder must come down harder”, again all other things being equal.

In other words, whenever stock prices go out of sync with fundamentals and valuations, a correction (upward or downward) always happens.

Coming to Waaree Renewable. In one year earnings are only 3x while stock price is 13x. With all due respect company is not a unicorn and nothing they are doing is special or unique. So it beats me as to why a renewable business should get a P/E of 120 (that too after 40% correction).

2 Likes

According to the latest data from Mercom, India has 64.5 GW solar module manufacturing capacity at the end of 2023 whereas we exported 4.8 GW of modules in 2023 and India’s capacity addition was 7.5 GW.

Taken together we consumed 12.3 GW of modules whereas we have a capacity to produce 64.5 GW .

Are we looking at massive over-capacity in solar module manufacturing in India?

5 Likes

Even though budget has the tailwinds for the sector, management was gung ho about the sector and see orders till 2030 or so, any idea why the stock is correcting left and right? does street expect one more soft quarter?

1 Like

All will be clear once the results for the June quarter set in. Looks more of an operator play with lower circuit being hit as on 2pm. It is a sunshine sector no doubt but still its TTM PE 115.58 compared to 76.68 sector average. Watch this link below for a great reound up on the company

1 Like

Why this business should deserve P/S of 20+, P/E of 100+, P/B of 70+ ?

There is no moat, no differentiation, no sustainable competitive advantage.

There is growth in the sector, adoption of solar energy is increasing, more projects are getting installed, big and small, but that does not mean valuations can be sky high. In fact there is no reason why even the sector valuations should be rich, a sector PE of 70+ is way too high.

4 Likes

My view is that their capacity , ability to execute large projects , end to end integration within group and international presence should be differentiator

3 Likes

Predicting stock prices is always uncertain, which is why the market exists since we will have differing opinions. However, I believe the Solar EPC sector is becoming increasingly crowded, with lower entry barriers allowing new players to enter regularly, driven by favorable conditions and government support. Ultimately, the market share will shrink, and valuations will stabilize. Most of re-rating is already done, now dust has to settle.

Between i just happen to open their website (never invested / researched waaree so far), looks like they are super busy for sure. Someone needs to move to 2024 ![]()

5 Likes

Why inspite of delivering excellent results, stock is going down?