@Amit2saxena

Thanks for seeking my view. My view may be negatively biased due to my exit and investment in competitor ITC.

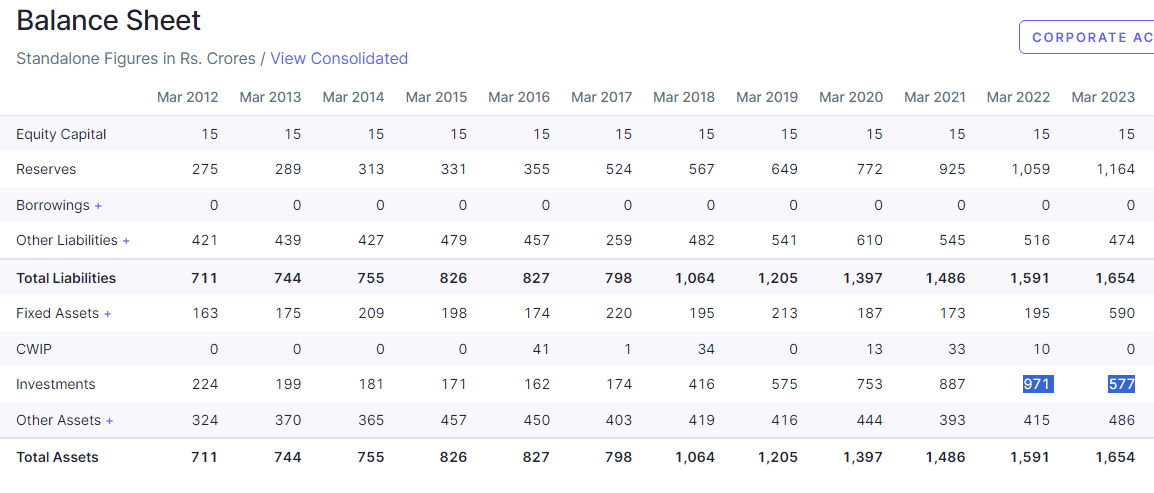

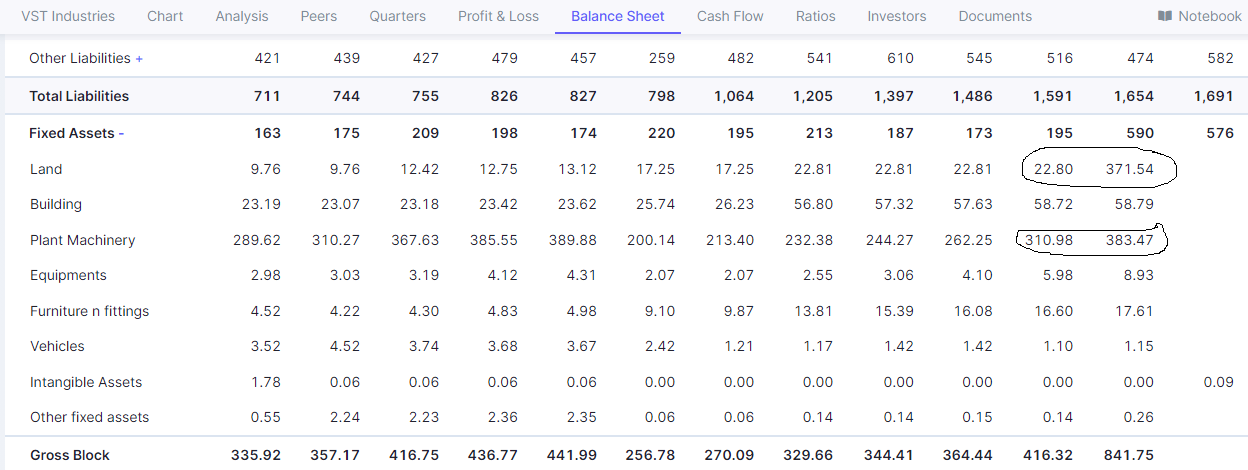

As correctly pointed out by you, the company spent around Rs 350 Cr for purchase of leasehold land. As per screener data Rs 350 Cr are utilised for purchase of land while around Rs 73 Cr is addition in Plant and Machinery which I assume normal mainteance and growth related expense.

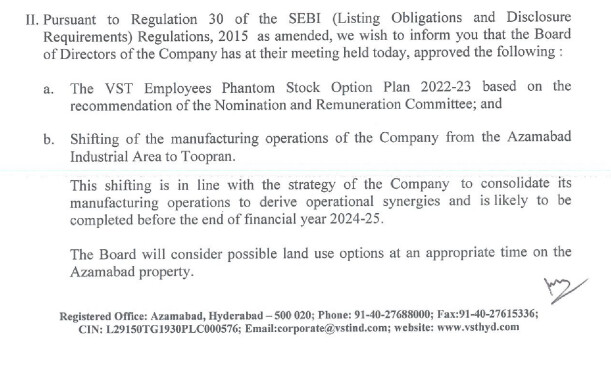

I also gone through Q2FY24 results which has following comments in the covering letter.

From this, it appear that company management intend to integrate its operations at one place and likely gain from synergy. Further, it is likely to release Azamabad property in Hyderabad, which may be encashed in future. Hence, to take a view only on purchase of land and infer that management is misallocating capital may not be correct in my limited understanding. One need to see action of management, specificially about land encashment/utilisation of Azambad in Hyderbad and how it share the benefit with the shareholders. In short term, such action would mean lower other income and hence lower dividend distribution, but in long term, it might be positive for the company.

Disclosure: I have exited from VST couple of years back and continue to remain invested in ITC. Hence, my view may be negatively biased. I have excellent track record in being wrong with my forecast. I am not SEBI registered advisor. I am suggesting any investment action in the company.

Why the company invest huge amount to purchase the lease when they already had the lease and also doing business from there.And what incremental revenue this land can generate for the company, any idea?

I am expecting that the market value of the land will be much higher. They can sell the land and move outside the city at a much cheaper cost. The return will be distributed as dividend

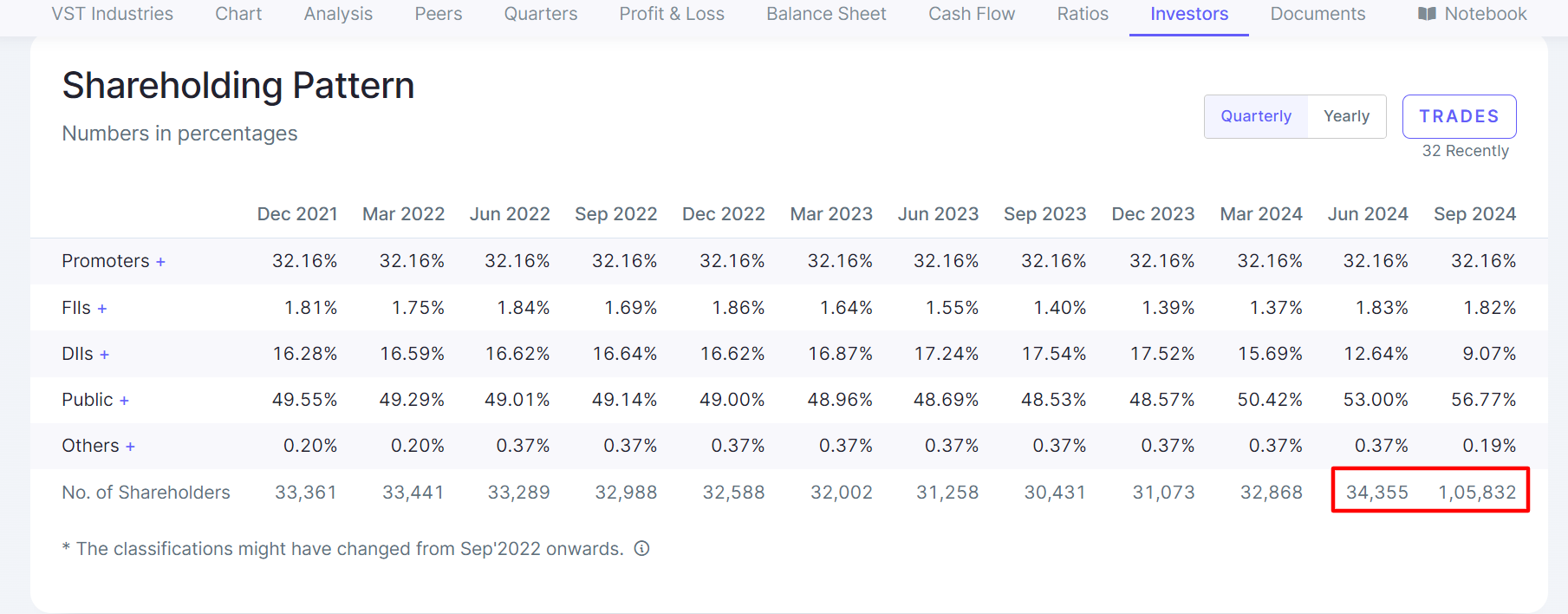

Looking at reduction of holding by both FIIs and DIIs compared to last quarter, the only assumption is more retailers have bought this stock in the last quarter. (3.77% increase)

@dd1474, request your view on what’s gone wrong with VST Industries, as you were invested in it for quite some time. Their profit has de-grown by 21% in past 12 months. It would need some meticulous planning and execution to mess up a business as simple and sticky as tobacco, that too without any adverse regulation.

Why doesn’t BAT do anything? Same for RKD.

I just can’t understand why there is no accountability for the deteriorating results. Request to help me understand the dynamics of why bad results don’t seem to be causing any kind of shake up in the company.

Thanks

Tobacco prices have gone up a lot due to crop failure globally. This reduced gross margins. This though means that prices will go down a lot in a year as more farmers plant tobacco.

Excluding other income Q3 PAT seems to be de-grown by 10%. Other than high tobacco prices is it something related to new operation facility maybe taking time to stabilise? Or something else if anyone have insight?

The audited financial results for Q4 of FY 2024-25 have been released. These results pertain to both the quarter and the financial year ended. Alongside the results, the company has recommended a final dividend of ₹10 per equity share, The dividend if approved will be paid within 30 days of the approval of the shareholders at the ensuing 94th Annual General Meeting.

Let’s move on to the financial highlights. The figures reported are in lakhs but will be discussed here in crores for better clarity.

Revenue from Operations: ₹454 crores, compared to ₹470.5 crores in the previous quarter and ₹476 crores in the same quarter last year. Revenue has declined both on a quarter-on-quarter (QoQ) and year-on-year (YoY) basis.

Other Income: ₹10 crores, reflecting a sharp YoY decline.

Total Income: ₹463.8 crores, down from ₹478.4 crores last quarter and ₹505 crores in the same period last year, indicating a downward trend both QoQ and YoY.

Expenses: ₹397 crores, lower than ₹413 crores in the previous quarter but higher than ₹390 crores last year. While expenses have decreased QoQ, they have increased YoY, even as income fell, leading to pressure on profitability.

Exceptional Items: In the previous quarter, the company had booked an exceptional gain of ₹100.5 crores. No such gains were recorded this quarter, which has further impacted profits. So while comparing the results of this quarter with previous quarter, we need to exclude this one time Exceptional gain from Operating Profit, Net Profit.

Operating Profit: ₹67 crores, down sharply from ₹165.6 crores last quarter and ₹115 crores last year.

Net Profit: ₹53 crores, compared to ₹136 crores in the previous quarter and ₹88 crores a year ago, showing a steep decline both sequentially and annually.

Earnings Per Share (EPS): ₹3.13, versus ₹8 in Q3 and ₹5.2 a year ago, again highlighting the deteriorating financial performance.

Overall, the quarterly results reflect a significant weakening in both revenue and profitability.

Full-Year Performance (FY 2024-25)

Revenue from Operations: ₹1,809 crores, down from ₹1,837.5 crores in FY 2023-24.

Other Income: ₹35 crores, showing a decline YoY.

Total Income: ₹1,844 crores, compared to ₹1,917 crores in the previous year, marking a consistent drop.

Expenses: ₹1,575 crores, rising from ₹1,522 crores last year. Higher expenses, coupled with lower income, have weighed on margins.

Operating Profit: ₹369.6 crores, lower than ₹394.7 crores last year.

Net Profit: ₹290 crores, down from ₹301.6 crores.

EPS: ₹17.1, compared to ₹17.7 last year.

Both quarterly and annual performance indicate a clear weakening in financial strength, adversely affecting investor sentiment.

Following the results announcement, the stock price crashed by 7.9%, closing at ₹304.4. Despite this sharp fall, the stock still delivered a 2.5% gain over the past five days and a 13.7% return over the past month.

Key Reasons for the Stock Crash:

Disappointing quarterly and annual results, with sharp declines in both revenue and profitability.

Broader market weakness and profit-booking activities by investors.

Given the poor performance and overall market conditions, there remains a possibility of further downside in the stock price.

Note: This is not an AI generated content. I’ve created all the content and before posting took AI’s help to improve the Vocabulary.