@Donald

A recent report by Nirmal Bang highlights a few points that I found useful :

They analysed for cos which have been out performers in Cement Space in last 10 years

- Shree Cement - 27% CAGR over 10 years

- Ultratech - 26% CAGR over 10 years

- JK Cement - 24% CAGR over 10 years

- Ramco Cement - 21% CAGR over 10 years

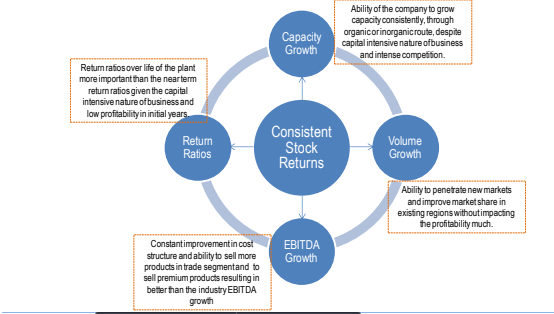

What the study claims is that consistent performers depicted following traits

Capacity

-

Cement being a capital intensive business, very few companies have been able to add capacities consistently without impacting the balance sheet.

-

While India has abundant reserves of limestone, key limestone bearing belts called clusters generally houses the majority of cement plants in the country. There are seven such clusters in India viz. Chanderiya (Rajasthan), Satna (Madhya Pradesh), Chandrapur (Maharashtra), Bilaspur (Chhattisgarh), Gulbarga (Karnataka), Yerraguntala (Andhra Pradesh) and Nalagonda (Andhra Pradesh). Despite the abundance of the mineral, key limestone bearing lands/mines are already being taken up by the incumbent players. Sourcing of new mines and erecting a cement plant on greenfield basis has become increasingly difficult and time

consuming -

Therefore companies which have historically done well have had the vision to identify

and develop new sites for cement plants and execute their capex plan well without compromising on Balance Sheet. -

Since higher capex leads to higher interest and depreciation cost, if the commissioning of the plant coincides with weak demand or pricing scenario, the payback period as well as profitability from the new operations gets delayed

Volume Growth

-

While building a cement plant comes with its own set of challenges, selling the manufactured cement in the market has its own obstacles

-

Cement demand in India has grown at a CAGR of ~6% over the past decade. This compared to growth in supply at a CAGR of 7.4% over the same period means supply has outstripped demand. Hence, achieving higher volume growth, we believe, is more challenging given the intense competition, especially in a new region where the company has to set up the entire distribution network from scratch.

The first two points indicate that Outperformers should have

(1) balance sheet strength to incur capex on a consistentbasis

(2) comfortable utilization levels which can support higher-than-industry volume growth - A well Oiled Sales Machinery

EBITDA Improvement

-

EBITDA is a function of volume as well as the cost structure and pricing in the markets it is operating based on the demand-supply scenario

-

There are multiple variables that affect EBITDA of a cement company. These are volume, pricing and costs.

-

Volume is a function of the ability of the company to push volume in the market profitably, costs are driven by efficiency and commodity prices.

-

Efficiency is driven by the company itself, adding capabilities to produce at lower cost. Long term Investment in Waste Heat Recovery, Wagon Tippler, Storage Areas etc

Ratios

-

Debt Equity Ratio becomes an important Ratio in Cement (just like in any Commodity Cos)

-

At a Debt of 1500 EBITDA/Ton, it becomes unsustainable to run a Cement Plant.