Frankly I do not think the hype around Jio is for Jio retail only, but also for the large subscriber base it can provide to the investor and the consumer data thereto, which is true for Vodafone also, smaller scale but still considerably large.

Secondly if the company is pushed into bankruptcy the acquirer shall have to run the company for itself which may not be its core competence, and with IBC suspended shall be a long tiring process, whereas an investor shall be investing in a company which has a capable management but in distress due to an unfavorable operating environment and sudden drastic change in competetive environment.

1 Like

That’s definitely a positive which I didn’t thought of. Moratorium of 6 months for the company at a time when revenue is not majorly affected is going to be a big relief for the company. And also prospect of addl loan owing to covid 19. The AGR overdue is still going to be an overhang. However, if some PE investor with more information on the promoter intent puts in money , it’s going to be a positive. The company generated an operating profit of 3400 crores in the last quarter which is more than 10% of the market cap even now ,after the stock has appreciated more than 100% in the past 1 week.

But no idea on how the company will address the huge payables in what keeping me away from the company.

As i mentioned earlier Voda will go further. VIL Shares were 873 crores in 2018/19, with the price of Rs.50 per share the markt cap was 43,650 cr. After rights of 2,000 cr Shares added. present equity is 2,873 cr. To reach past Market cap of (43,650, to this add rights with premium of Rs.25,000 cr) = 68,650 cr, Share price should quote Rs.24. Once it reaches 24 means VIL is valuing at two years back valuation. Because of Google and future trends it should add another Rs.20 to reach Rs.44 by next year. Market cap of VIL at Rs.68,650 would be flagship company of Birla. At present Market cap of his major companies are Grasim 41,234 cr, Hindalco 33,537 Cr, Ultratech 111,735 Cr, AB Capital 13,505 Cr and AB Fashion 10,738 Cr.

5 Likes

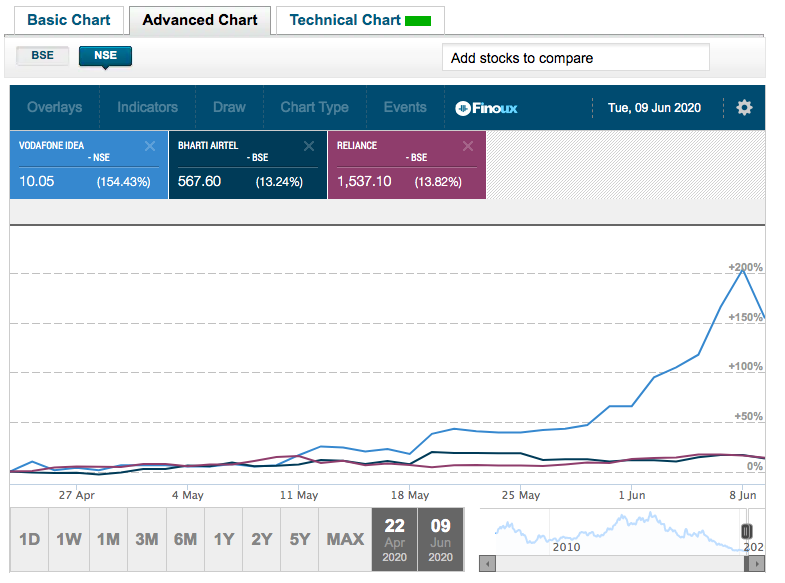

No smoke without fire?? That seems to be the conspiracy theory behind the recent buzz (read rumors) around VodaIdea and Bharti Airtel.

I refer to these articles:

Amazon in talks to invest $2 billion in Bharti Airtel: Sources

With Facebooks’ recent investment in Reliance’s Jio Platforms, global technology giants seem to be scurrying to find investible opportunities in the Indian telecom play. With competition in India restricted to just 3 players, the choice, is obviously one of the other 2 players (Airtel and Idea).

Now why the renewed, supernormal, interest in Idea? Remember that the stock move really started post the day FB investment was announced in Jio (April 22nd). Idea, which was quoting at ~ Rs.4 levels that day, scales a top of Rs.12 a couple of days back!!! While Airtel too showed renewed buying interest, Idea has been the max gainer in this period.

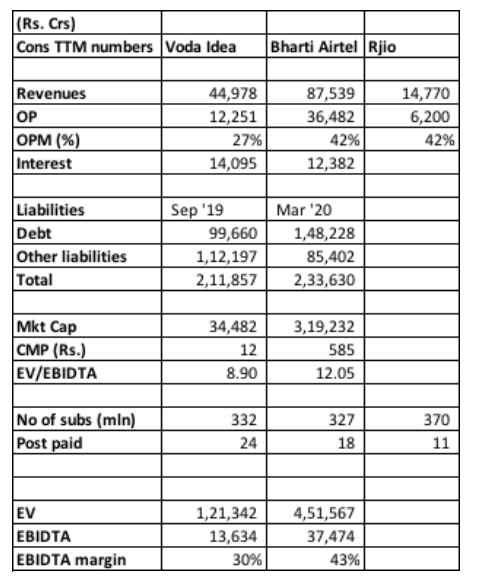

The table given below, possibly, tries to explain the logic behind this outperformance:

As seen from the table above, the basic argument for the increased interest in Idea seems to stem from the fact that: (a) With several metrics comparable to that of the other players, is such a steep discount to the market cap of the peers warranted? Even if one were to give Idea some discounting on account of lower profitability compared to peers, the discount should narrow (b) FB is already invested in Jio, and institutional holding is the lowest in Idea (@ 14%) as compared to Airtel (@36%).

P.S.: i am NOT fanning any rumor about Idea or Airtel in this note…i’m merely trying to break down the logic behind the recent buzz around the stocks.

Disclosure: I have a tiny allocation to Idea.

The numbers quoted in the table are from online sources…there may be some variations from the actuals… these are only indicative …

1 Like

Im not sure sir…as mentioned in my post, this is merely my inference and i could be totally wrong… this forum is meant to have content which provoke thoughts and discussions (based on logic). Besides, one other observation: When reports of Amazons interest started floating on social media on the 4th of June, Airtel clarified its stand on the 5th morning itself before the markets opened.

I’m NOT trying to accuse or point a finger at anyone here in specific…just speaking my mind aloud ![]()

Entire Sector is attracting Capital from all around the world. Capital Cycle Throery and Hope of getting a Investor on Board is driving the price. Vodaidea stands in the same place as of Yes Bank ofcourse for genuine capital erosion to sustain in the Market Place. Future business is good, need somebody to take burden of debt, as i understand.

1 Like

While the SC decision on June 11th was perceived negatively (as implied by the correction in the stock price that day), the silver lining is that the apex court didn’t completely thrash out the relief package. From what i read from the apex court’s dictat of asking the telcos to detail a roadmap on how they plan to pay the AGR dues, is their acceptance (to some level) of not letting India’s telco competition shrink to a duopoly. A more practical approach, even if not exactly as what was proposed by the DoT, could be on the cards.

A recent article in the BS also hints at the same:

15-yr period, to pay AGR dues, important for Idea survival - analysts

1 Like

Basically court has shown its willingness to accept a staggered payment plan. Only question mark is about time period and guarantees to be given. There will be some negotiations on that but Vodafone survival is no longer in doubt in my opinion. They even paid outstanding interest on their NCD’s over the weekend and FT investors are recieving the same.

1 Like

Maybe vodafone Idea should say, here is some stake for government or pledge shares to government until the repayment is done. Like done for lufthansa airline.

I also wonder, if the AGR dues are to be paid at 8% interest over a certain period and if they can borrow money at lower interest rate than that, then should it borrow money and repay the debt in one go?

Also, should it not explore option of borrowing money at 3-5% from its promoter, which can prove that everyone is interested in running company profitably ?

I am sure the management is considering all the options.

Let’s say if nothing works out, would lenders consider restructuring the whole thing like done in case of Yes bank, Suzlon, etc. If they don’t would lender along with government be the biggest loser here?

At least I think government would be the biggest loser as there would be job losses along with revenue/tax loss. Also in case of only 2 private players, the spectrum auction might not result in windfall gain (though might have same problem with only 3 players).

1 Like

One important point is that 8% interest is only on the principal amount, not on the penalties and AGR interest. Those have been frozen long back and are a much larger chunk of the amount. At least that is my reading, not 100% sure about it.

"As ET reported, the government’s formula includes freezing interest and penalty components as of October 24 — the date on which Supreme Court ruled in favour of the Centre’s calculation of AGR — and said the net present value will be “protected using the discount rate.”

1 Like

Hi,

The article explains how it will be difficult for idea to get out of the debt and AGR mess.

https://www.daijiworld.com/news/newsDisplay.aspx?newsID=721242

Thanks,

Deb

I also wonder, if the AGR dues are to be paid at 8% interest over a certain period and if they can borrow money at lower interest rate than that, then should it borrow money and repay the debt in one go?

Nobody is going to lend them money anymore.

Also, should it not explore option of borrowing money at 3-5% from its promoter, which can prove that everyone is interested in running company profitably?

Theoretically true but won’t happen. The amount too big. It will take away large chunk of money from the promoter group. Not sure if any other company of the promoter group is doing that well to cushion VIL’s losses.

Any idea about the results??

Hope the management will provide with the reasons for not giving results on scheduled date

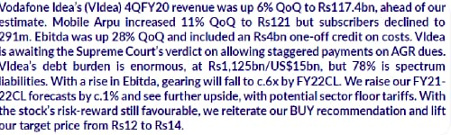

Revenues are up by 6% and ARPU is also now 121. But any idea what is the exceptional item(s) because of which net loss is up by so much for Q4FY20?

CLSA view on Voda Idea

Voda Idea Q4FY20 results (a sell side analyst review):

Vodafone Idea Q4FY20; Consolidated QoQ

- Revenue grew only 6% despite 30% tariff hike; revenue growth slowest in the industry

- Subscriber losses offset benefits of tariff hike; 4G subscriber addition still low

- EBITDA aided by one-off of Rs 400 crore; achieved 100% of merger benefits

- Core EBITDA still negative; Core EBITDA is reported adjusted for synergy benefits, one-offs IND AS-116

- Ended Q4 with net loss of Rs 11644 crore; partially due to exceptional loss of Rs 6100 crore

- FY20 net loss stood at Rs 73878 crore

- Cash flow stress evident; cash balance at an all-time low; net debt higher

- Dues worth Rs 27,121 crore up for repayment in FY21; amount is more than 3x the FY20 cash flow from operations

- Pledged its 11.15% stake in Indus Towers

- Capex dipped QoQ which means cash crunch hurting investment in network

- Ability to continue as a “going concern” depends on external factors – 20 years instalments to pay AGR dues and loan waivers.

Vodafone has managed to use Government money at low / 8 % interest , on dues for Spectrum 88,000 crores . Agr dues 50,000 crores Voda will get installment payment at low rates of interest . So effectively they use 1.40 lac crores of government money. no need to go to bank for loans.

Birla & Voda have managed smartly the onslaught of Jio last 3 years with the merger.

Voda q4 results should create following triggers during the year :

Tariff hike 25 percent to cover interest costs .

Stressed balance sheet to get agr relief for sure .

Fund raising :

Either another 50 percent rights issue in August promoters to bring in money.

Raise money against tower and Fibre assets .

New investor buy who can pay 15 /20 a share . Promoters will not give below 15 bucks as merger benefits will pay out this year .

Q4 Operations doing very good.

Q1 q2 should complete all rationalization and cost cuts .

This will bring up enterprise value . From q2 they will not lose customers .

From q2 they will not lose customers .

How can anyone predict this? What’s the justification/argument behind this rationale?