Bought some of HDFC Limited (1.5% of PF) yesterday. My first real large cap after ITC. And the reason is simple - I think the valuations have corrected to levels from where HDFC can meet my return threshold of 20% CAGR, and that too with minimum downside risk. In fact if it corrects more to 1800-1900 levels, I may add big to it, probably at the expense of Equitas Holdings.

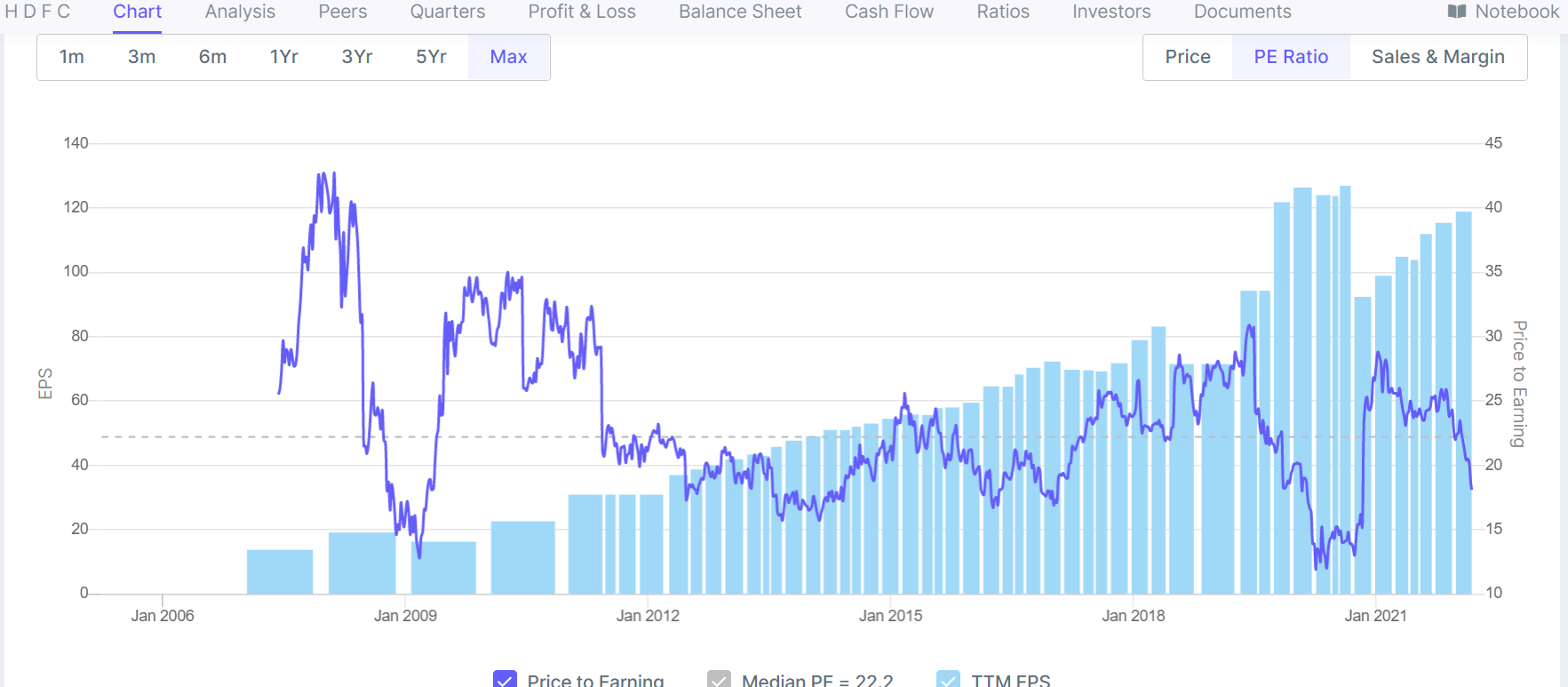

The two charts below gave me technical and valuation buy signals.

The first is the weekly chart of HDFC Ltd. Notice that over the last 15 years, it has not managed to stay below its 200 week simple moving average for long. And this makes sense - it is probably the perfect proxy to the India growth story. The second is its long term PE chart. Now of course PE is probably bot the best metric for HDFC, but I’m sure PB and other charts will follow similar patterns.

The valuation hits bottoms of around 16/17 times, and down to 13 times in peak uncertainty like the global financial crisis and covid. The reversion to mean (and well exceeding it) is rather swift too. I bought yesterday at 17.8 times and will buy more if it gets into the 16-17 times range. The mean PE is 22.2 times, and I will sell whenever it hits 24-25 times over the next three years. So essentially expecting a 40-50% gain from rerating, plus 10-15% per annum on earnings, netting to at least 2x in three years, with minimum permanent downside.

At the end of the day, HDFC is the best retail focused housing finance NBFC business in India, owns 25% in the best bank in India, has large stakes in the other listed HDFC group companies, several profitable unlisted entities and start-up investments, consistently growing and their moat getting stronger by the day, all at under 200 week DMA, sub 4 lakh crore mcap. On a risk adjusted basis, it looks like a no brainer, even for a higher return threshold investor like me.