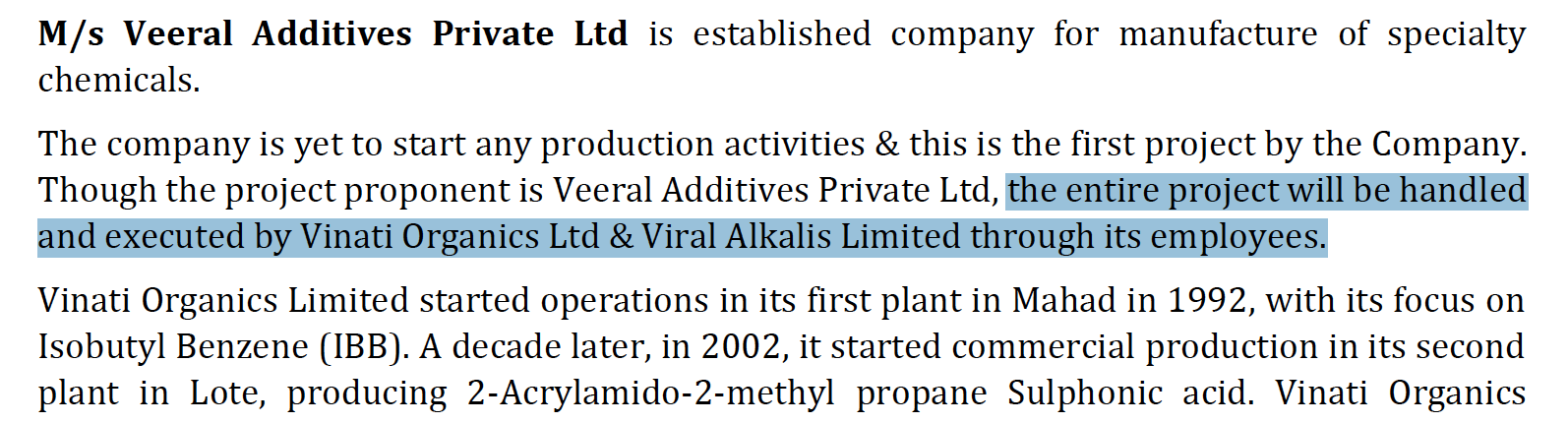

Some more finer points on amalgamation and antioxidants (AO) landscape:

VAPL is into the business of manufacturing Antioxidants (AO’s) - AO 1010, AO 1076, AO 168.

India has a demand of 10000 MT for these AO’s and the global demand is around 300000

MT. VAPL has a capacity of 24000 MT per anum.

The acquisition of VAPL is a forward integration for VOL as Butyl Phenols will be the key raw

materials to manufacture these AO’s. After the acquisition, VOL will be largest and the only

integrated manufacturer of these AO’s in India.

This acquisition will allow VOL to add a new revenue stream of specialty chemicals which

have good growth potential both globally as well as domestically. The growth is driven by

increased consumption of various plastics like LDPE, LLDPE and PP etc.

VAPL has the potential to clock Rs. 500 crores in revenue (Rs. 300 crores incremental

revenue) for VOL.

What’s VP friends view on amalgamation with veeral additives?

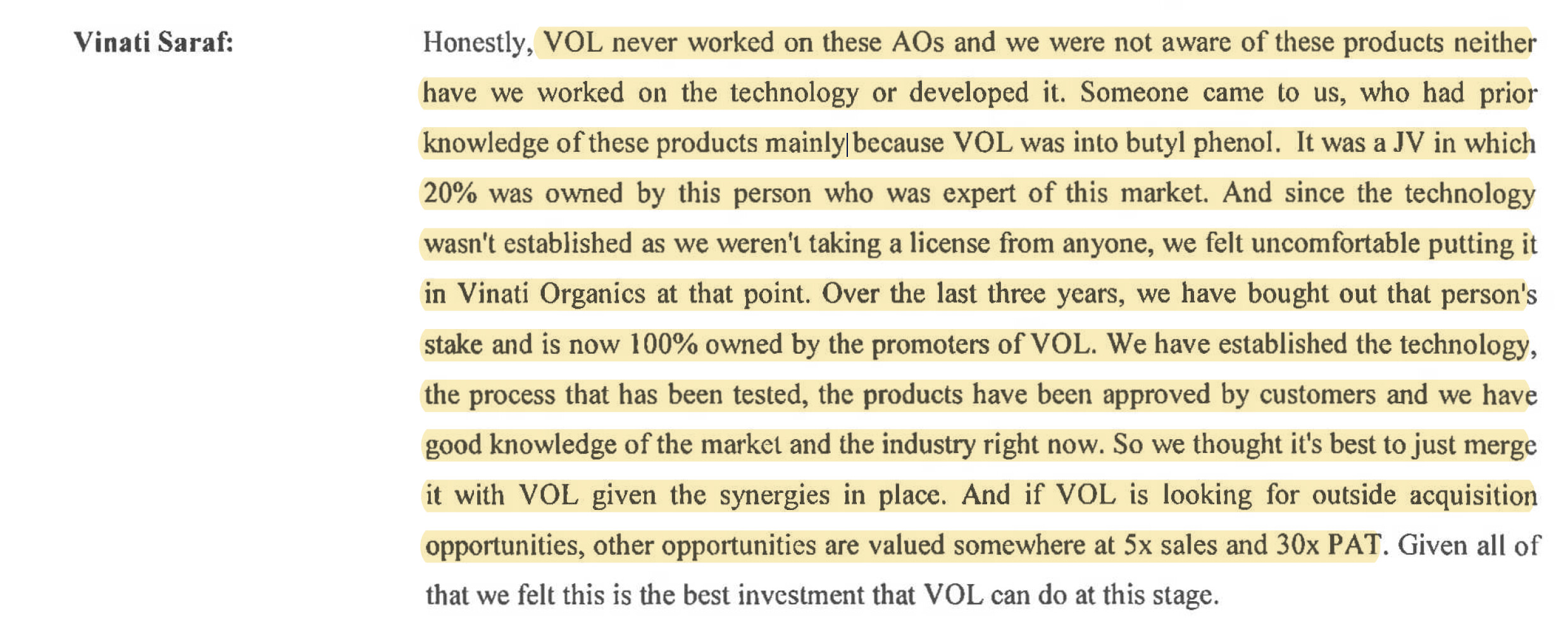

https://www.youtube.com/watch?v=8KumlI5gJUg&t=496s - in interview CEO she says veeral organics has zero revenue while veeral additives has (she use the word as revenue potential) 300 to 500 cr.

In BSE note page 8 it shows veeral additives revenue is NIL.

Management interview (link) and the press release (link) clarifies the whole Veeral Additives potential merger. Key points below

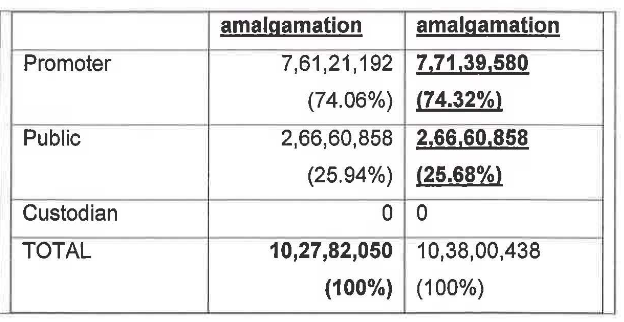

Veeral Additives will manufacture anti-oxidants (AO 1010, AO 1076, AO 168) which is a forward integration as it uses butyl phenols as raw material; Half of the produced butyl phenols will be used for making anti-oxidants

Veeral plant capacity: 24’000 MTPA. Indian demand for AO ~ 10’000 MTPA (mostly imported), global demand for AO ~ 300’000 MTPA. This will make Vinati the only integrated anti-oxidant plant in India

Earlier, company was expecting revenue potential from butyl phenols of ~500 cr. at full potential, it will reduce to 250-300 cr. with rest going to make anti-oxidants. Revenue potential of Veeral additives is 300-500 cr. So overall revenue potential is now 250-300 + 300-500 ~ 550-800 cr. i.e. increased by 50-300 cr. (maximum potential increase is ~300 cr.)

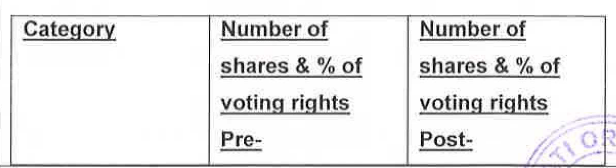

Equity for Veeral is valued at ~125 cr. (net asset ~ 43 cr. P/B ~ 2.9x), no cash outgo but promoters of Veeral will get shares of Vinati organics. If merger goes through, promoter holding will go up from 74.06% to 74.32%

Timeline for merger approval will be 8-10 months. Expect plant to fully ramp up in 6-8 months post approval. Plant and machinery is already ready and only requires few additional machinery

Veeral additives is mostly owned by Vinati’s father and it will related party transaction

Currently producing 3 out of 4 butyl phenols

Increase in staff cost is because of ramp up of butyl phenol plant; buy phenol from Deepak nitrite. Phenol accounts for 50% raw material, other important raw material is isobutylene which Vinati Organics manufactures on their own

ATBS is now back to pre-covid level from January 2021, starting the new capacity in February to meet pent up demand

Guidance: FY21 revenue down by 10-15%, FY22 growth of 20% and FY23 growth of 20%. Expect 1500-1600 cr. revenue in FY23

Instead of creating asset separately and then merging it with the parent company will lead to a proabable goodwill acquisition of ~82 cr. (125 cr. - 43 cr. of net asset), not the cleanest way to build assets.

Earlier, company was expecting revenue potential from butyl phenols of ~500 cr. at full potential, it will reduce to 250-300 cr. with rest going to make anti-oxidants. Revenue potential of Veeral additives is 300-500 cr. So overall revenue potential is now 250-300 + 300-500 ~ 550-800 cr. i.e. increased by 50-300 cr. (maximum potential increase is ~300 cr.)

It means operating margin of ~35% from phenol business!

Is this forward integration (Antioxidants) separate from earlier announced 150Cr? if yes, than all of Phenol capacity will get used in-house. If not, this way of obfuscation by management is not required.

ATBS is now back to pre-covid level from January 2021, starting the new capacity in February to meet pent up demand

Guidance: FY21 revenue down by 10-15%, FY22 growth of 20% and FY23 growth of 20%. Expect 1500-1600 cr. revenue in FY23

With the ATBS back to pre-covid level and they are starting new capacity, should not we see growth in Q4 vs Q4 FY20 to a level of Q419? and it covers the gap to a large extent?

I think she has been quite inconsistent the way she gives guidance on sales. FY23 will be up by just 50%? how it relates to earlier guidance of doubling of revenue in 3-4 years.

Veeral additives is mostly owned by Vinati’s father and it will related party transaction

That conversation got cut in this interview, I think he is not the only owner of Veeral. Things will get more clear when they come for EGM.

If you see document submitted for the environment clearance, whole story is around Vinati. All this is without any related party transaction of project execution nature in Vinati’ books! Yes we need to ask them / understand what’ the need of building capacity like this! (though the scale of this transactions is very minuscule to worry much).

Considering following constraints booked profit and exited the stock -

Stagnant or declining revenue for quite some time (2 years) and no growth in sight for few more quarters at least

Delayed new capacity coming into play will keep a drag on revenue

ATBS future demand growth remains blurr as another round of crude price decline can start anytime if Saudi or Russia increases output.

New products will increase revenue but with lower margin levels. Current EBIDTA levels may not be sustainable going forward

Steady share price despite mediocre performance IMO is due to small float - @75% holding by promoters and tight holding by institutional players. Any sizable chunk coming for sale may create good price discovery

Its quite incredible how Vinati Organics keeps chugging along investment in niche chemicals and try to forward and backward integrate to make the most out of their chemicals. Another highlight was their plans to restart trials of PAP. This is something they have been trying (and failing) since 1998 because they haven’t been able to devise a green process.

Together with the bullish phase in the market and that vinati has not yet been a beneficiary inspite of good track record and financials the stock could show massive gains going forward

Hi @edwardlobo , what is your opinion on valuation discount compared to sector valuation and average valuation from last few years. Any triggers do you see for upcoming few quarters (not only immediate quarter). Appreciate your service in this forum.

There are a few things that are going to work in Vinati’s favour

Vinati supplies a lot to crude industries, crude prices are rising and although the world is talking about electric vehicles, countries like we at India are building one of the largest refineries. We are still auctioning coal and as majority of Indians will now get into upper middle class the demand on electricity will only increase. Most of it will have to be met by traditional resources. Whenever crude does well, Vinati does well due to supply for those industries

Secondly as per the interview, the long awaited basf plant where Vinati supplies ibb has gone live. Vinati has been planning for this for over 2 years by expanding capacity. The demand for ibuprofen is only increasing as people are living longer and have to manage pain, the effects of old age

So I think it’s not just the next time quarter that will be good compared to previous but the numbers are here to stay

From the following quarters after next, they have the new atbs plant taking over some of the extra demand

Market is forward looking as you would see in the case of Paushak markets rallied that stock 3x times just on the news of expansion getting environment clearance

My investement thesis for Vinati Organics is as follows;

Due to long term uncertainity of crude oil demand (due to EV/Solar), oil explorers will be hesitant to make huge capex for complex exploration projects

To maintain supply they will rely on production from existing oil wells

One of the most proven ways to continue/improve production from existing oil wells is fracking (Please note, fracking is not used only in shale oil wells, and is used widely for conventional oil wells also)

ATBS is used for fracking and demand should remain strong

Well, there is no doubt that share is overpriced, considering no growth over last few quarters looking just at the financials, however their is more behind the curtain :

Management has been very proactive and cadid about giving reasons for the same and giving growth projections.

I would not get into details as it is already covered in this forum, however net summary is, management is looking at 50% growth in next 2 years (total 50%) with maintaining a margin of 20%.

Considering Unique and Niche Specialty products and high entry barriers in the segment, along with market leading position, the valuation seems justified.

Business Category: B2B, and Export (~75%) oriented

What likable?

Promoter stake: 74+%

Owner Operator – Vinod Saraf (Chairman: Started the business) and Vinati Saraf Mutreja (Managing Director & CEO, joined in 2006 and took over as MD & CEO from 2018, Daughter of Chairman)

Niche Product – Limited Competition due to cost and technology advantage

Focus on clean and green technology

Excellent Balance sheet – No borrowings, and Cash Surplus

Good NPM (due to Integration approach across value chain), which are main factor in excellent ROE

KPI

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

NPM - NetProfit from Operating Profit/Sales (A)

14%

20%

21%

17%

23%

29%

Sales/Total Assets (B)

1.3

0.9

0.8

0.7

0.9

0.7

Total Assets /Total Equity (C )

1.4

1.3

1.2

1.2

1.2

1.1

ROA (AxB)

18%

19%

16%

12%

21%

21%

ROE (AxBxC)

25%

24%

19%

15%

25%

23%

Company’s Operating Cash Flows are higher than Net Profit and leave surplus cash after taking care of Business (Capex), Lender (Repayment of borrowings) and Shareholders (Dividends), ensuring a sustainable business model.

Revenue dependent on 2 Key products-IBB and ATBS -that have Limited Market opportunity

Instances of overpromise in past ARs but under delivery

Current valuation- Considering key risks such as Opportunity Size, Limited Key Products, Non-Linear Top line Growth and correlation of ATBS (the star product of overall sales) sales to Oil Prices

Key Risks:

Items

Risk

Advantage

Plant Dependence

Only 2 Plants with Geography Concentration

Cheapest Per Ton Capex

Opportunity Size of Key Products

Limited

Lesser Competition

Limited Key Products

Heavy Dependence on 2 products

Customer Stickiness due to Lower Prices, resulting from Economies of Scale

Customer Concentration

What if contract is terminated?

Guaranteed Offtake

Non-Linear Top line Growth

Contract Pricing based on petroleum derivatives

Oil Prices < $70 Barrel

30% of ATBS sales to customers engaged in Oil Exploring - EOR (Enhanced Oil Recovery)

Disclosure – Not invested due to valuations but in watchlist.

ATBS: In FY20, ATBS capacity was 24’000-25’000 MTPA and Vinati was running at full capacity. In FY21, volumes tapered down to ~16’000 MT. Given the current demand forecasts from customers, Vinati should do 30’000-31’000 MT in FY22 (growth of 85%+ over FY21). Most of the incremental growth is coming from abroad markets. 3 global companies make ATBS. Vinati + Chinese player + Japanese company that makes 5’000-6’000 MTPA. Both Japanese and Chinese companies haven’t expanded capacities in the last 5-years. One of the reasons maybe that Vinati is the only backward integrated player. ATBS prices have been $2.5-3.5 per kg over the last decade (its volatility is 20-30% of crude price volatility). Last year ATBS prices were ~$3/kg which has increased to ~$3.5/kg.

Butyl phenol: Currently running at 50-60% of capacity. Expect 250 cr. of revenues from the 4 butyl phenols in FY22. Main raw materials are phenol and isobutylene (backward integrated). Currently, their customers make AOs and Vinati will be competing with them domestically. Wish to become top 5 players in butyl phenol and AOs in the next 4-5 years. Will definitely try to get 80%+ market share domestically.

IB: Current capacity is 40’000 MTPA (can be expanded to 50’000 in case required)

Expect double digit growth in IBB in the next couple of years

Other products contributed 25% of FY21 sales. Should grow at double digits

Debtor and working capital was high in FY21 due to launch of new products. Vinati also gives higher credit period to domestic customers of IBB and butyl phenol which has resulted in higher debtor days.

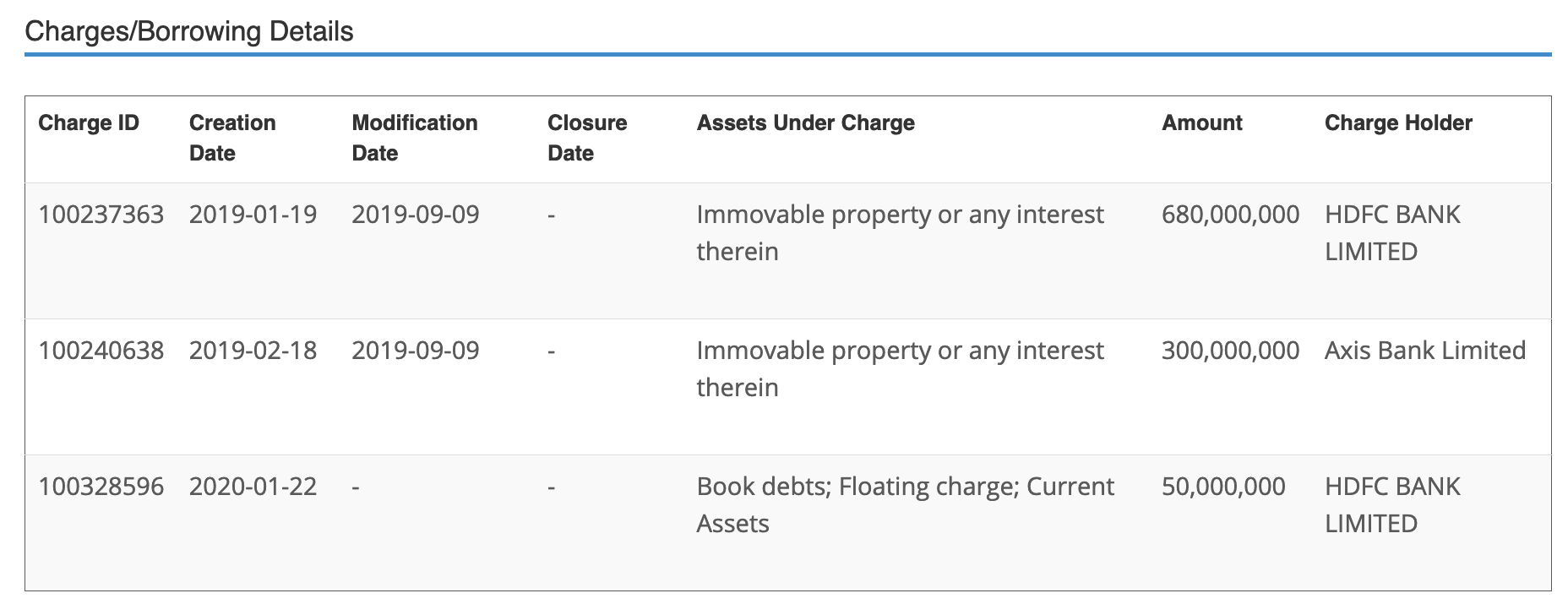

Loans and advances: Vinati has given 133 cr. of loan to Veeral additives pvt ltd. to pay off loans to HDFC bank. This loan should get nullified once merger is approved.

PAP will not be coming in for the next 2-3 years as technology is not in place

Newer products will be in the butyl phenol value chain

FY22 capex: 200 cr. for new products + 60-70 cr. in Veeral additives + Incremental capex for de-bottlenecking. Expect to incur ~300 cr. of capex over the next 3-years. Existing capacity of ATBS, butyl phenol and veeral additives will take care of next 2-3 years of demand

Big chunk of new capex will be in Veeral Organics (100% owned subsidiary) – this was created to avail lower tax rate of 15% (Veeral Organics has land of 20-25 acre in Mahad). Also Vinati Organics have sufficient land within existing facilities