Given the wide difference in profitability of trading ops (2-5% as per @desaidhwanil) and 20% on manufacturing why should PAT fall 14% if sales fell 18%.

Results look bad prima facie but this was expected. The nos. do suggest drop of volumes in manufacturing business. May be the co. faced teething troubles with new capacity and it didn’t add anything to the quarter.

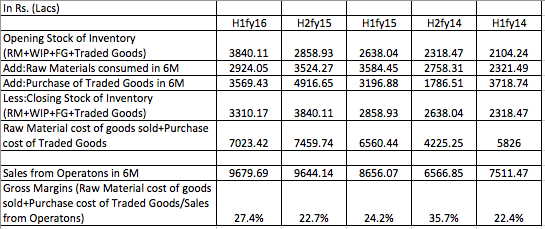

One respite is overall gross margins can be seen moving in the right direction,thanks to declining volume of trading business. I always had a doubt about trading business being loss making at worst and 2-3% margin business at best,data available on both lines of business leaves us inconclusive but following table can give a rough idea.

these short term fluctuations do happen when the companies change their business models. And for the long term the company seems to be on the right path. Technically also, do not see the stock breaking 50-51 levels and around those levels investors could look up to bulk up their position.

Just to clarify, 20% EBIDTA margins is what VDML plans to achieve in next few years and may not be the steady state margins in the near term. Last year was exceptional and their Manufacturing margins were above 20%, however, as always one should never make a steady state margin assumptions on one year number. The only thing we can infer from past data is that EBIDTA margins from manufacturing operations is consistently improving and inching towards their stated goal of 20% which will be achieved over next few years.

My take on Vidhi’s result was that management had indicated that their trading operations will be discontinued and hence topline was bound to fall. Also, the EBIDTA in absolute terms was bound to fall as well. What seems to support the hypothesis is the EBIDTA margin by almost 300 & 200 basis point YoY and QoQ.

What is expected PAT by FY20 if we go by Management comentry of 500 cr top line by 2020.

I think it will be 4-5 bagger at max.by FY2020 based on following assumptions.

FY20 topline 500cr (if we go by management forecast)

EBIDTA (20-25%)= 100 cr to 125 cr

PAT FY20= would be 50 to 63 cr.(at the best case)…

FY15 PAT =12.4 cr

FY 16 PAT = 16.2 cr Expected (6.2cr (H1FY16)+10 cr (H2FY16)…

so PAT will be grown by 3 to 4 times…

am i missing something in bove calculations…

Dhwanil… How did you arrive at 27% Manufacturing EBITDA? I am unable to figure it out.

Closing the trading operation would reduce the interest burden and improve some ratios and possibly free up some management bandwidth. Not a major deal for me.

If they are having 4200 MT rated capacity why produce only 2275 MT actually? Is it some manufacturing constraint or demand constraint or product mix constraint?

Going forward, they will have 125 MT per month additional capacity on stream post October 2015 (as per result announcement) … So, about Rs. 5 - 6 crores of EBITDA addition at 50% capacity utilisation going by historical trend. Am I correct here?

They seem to have no presence in marketing activity … they just manufacture and ship (as it appears from their foreign travel expense which is only Rs. 2 lakhs for a Rs. 108 Cr of FOB Export sales). In this type of situation I guess they would have a very very low pricing power … Except cost cutting / efficiency improvement they don’t have any area of margin improvement.

Total market size for synthetic dye seems to be about Rs. 2000 Cr. only from as derived from the management discussion (40000 MT x Rs. 500000 per ton) … It is a small market so competition possibility is of price erosion / new competition is low whereas big enough for players like Vidhi.

Somewhere one wrote in the post Natural Dye is 10 - 20 times the price of synthetic… What is the trend of price of natural synthetic? Is it coming down / steady / going up in last 5 years? What is the market size of Natural?

If management is to be believed then it would be generating Rs. 50 - 60 Cr NP by 2020 and at 20 PE would be a 3 bagger from present level. What all can go wrong???

I think there seems to be some confusion on EBIDTA margin. The absolute EBIDTA is 27 odd crores while EBIDTA margin for FY 15 is 23%.

Regarding the lower capacity utilization, we need to probe the management further. Also, management has indicated that 25-30% production in FY 15 was affected due to damage to critical equipment during fire so that may explain lower utilization partly. However, the number on capacity utilization and their bullish outlook and aggressive expansion still do not gel in well.

On additional capacity utilization, your calculation on EBIDTA number look broadly correct hence I expect Q3 number and future quarters shall have EBIDTA improvement of atleast this. If not we may need to be skeptical about management’s view/commentary on demand outlook

On low marketing cost- excellent observation. Again, we need to understand this more by talking to management but your hypothesis looks very valid at the moment

Natural Vs. Synthetic: It is difficult to generalize the differential as it is product/color specific. However the realization differential is in the range of 3-10 times. However, this spread is closing slowly but surely with lot of research going on natural colors side and technology advancement. However, key constraint for natural colors remain that it is to be extracted from living organisms hence the supply is not predictable and secure. Total natural color market size is roughly USD 1 billion and is growing at 6-7% CAGR.

Hope this is partially helpful. However, there are many questions that remain unanswered and hence we shall try to prepare a question for management and try to meet then and do Q&A.

The 4200 MT capacity is after new addition of 1400MT which came on line in Sept. So,2275MT on 2800MT seems decent utilisation.

As far as marketing cost is concerned,the co. doesn’t market as such,its got distributors across countries through which the products are sold although the end user F&B majors have entire backward trace of all raw-material inputs as any untoward incident could put the brand in jeopardy. One should find proportional expenses in that regard somewhere on P&L.

Anyone can produce synthetic colours but will reputed end users buy from anyone,that’s where comes the edge,can be validated by the fact that Sensient which sells colours at approx. 50% higher to Vidhi and the likes still holds roughly half the market. Its the trust of end users that wins Vidhi and the likes business is my understanding.

Agree with @desaidhwanil that next quarter and further,EBIDTA improvement should show up.

While reading about the chemical industry, the below 2 things in particular caught my attention:

Chemicals which add ‘Color’ to the final products. Example: Vidhi

Chemicals which add fragrance to the final products. Example: S.H Kelkar, Camphor etc.

If the eternal theme of “Indian consumption” story were to play out, the demand for the products as displayed in the below image will only look up and so the associated auxiliary products which supply to this industry too shall boom.

The colors are there in a shampoo, a soap, a face wash etc. and I think synthetic colors would do and natural colors are not required in these FMCG products.

Does Vidhi’s synthetic colors supply to these FMCG as well? As per the website, cosmetics are included but I tend to understand that majority of the revenue is from food grade colors/food industry?

Does the chemicals Vidhi make suitable to this industry as well? If yes and currently if it forms a lesser part of the revenue, surely the opportunity size is good.

Am I completely misunderstanding the domain of Vidhi?

Difference in pigments and dyes explained above.

Source - Clarinet Chemicals FY15 AR

Clarient had dye business in the sector of textile, paper and emulsion (TPE) and in leather. Both of these businesses have been divested.

They have made agreements with Archroma India Pvt. Ltd to supply TPE dyes and with Stahl India Pvt. Ltd to supply leather dyes on need basis.

Although clarinet is not into food dyes, I think it is a difficult business to be in. May be food dyes due to safety aspect and Vidhi’s export linkages - they are able to maintain such margin.

In 2015 annual report management has pointed that market size of food color is going to touch $2.5 billion(INR 16,500Cr) at page 53. In your management meet they are expecting to capture 20% of market share.

If considering both facts, market share by 20% will result into 3300Cr which is way above than mgmt target of 500cr.

Please correct me if I am missing something or going wrong.

Disc. - Invested 5% of my portfolio and looking to add more if management walks the talk.

they did ramp up their manufacturing so quite possible new people are added and also, there could have been bigger bonus payouts owing to better profits.

point! next thing would be how quickly they can reach maximum utilization of their plant and obviously it will depend upon the demand of their product.

True, though I would be pretty happy with around 30% growth that i can imagine for next FY too. This one is weathering the storm really well (on back of strong growth and dividends) and making newer highs in-between. In all likelihood, chances are (now getting into stock technicals), this would be one of the few stocks to watch out for in the coming year. Also, just getting with the basics, an ever improving RoCE and RoE is surely wonderful.

I am trying to calculate RoCE for the company which should be Operating profit/(total assets - current liabilities) which comes out to be 26.21/(130.87-82.47) = 54%… but screener is showing me 30% (for FY15 calculation). I am no accounting expert but an avid student of it so i may be wrong. Can someone correct me please?