Can anyone kindly explain what is meant by “limit”? I am new to investing and from non finance background.

1 Like

over-draft and borrowing limits for capacity expansion and purchasing raw-materials (inventory). basically, short term and long term loans.

The company plans to nearly double its share of exports from 12% in FY24 to 20-25% in FY25. Exports is a 2-4% higher margin business as compared to domestic business. So you can definitely expect some growth in margins.

30%+ volume growth + margin expansion could help bottomline grow by at least 40%-50% in FY25.

4 Likes

The receivables more than doubled from FY23 to FY24. Is there any commentary on it?

Hello everyone,

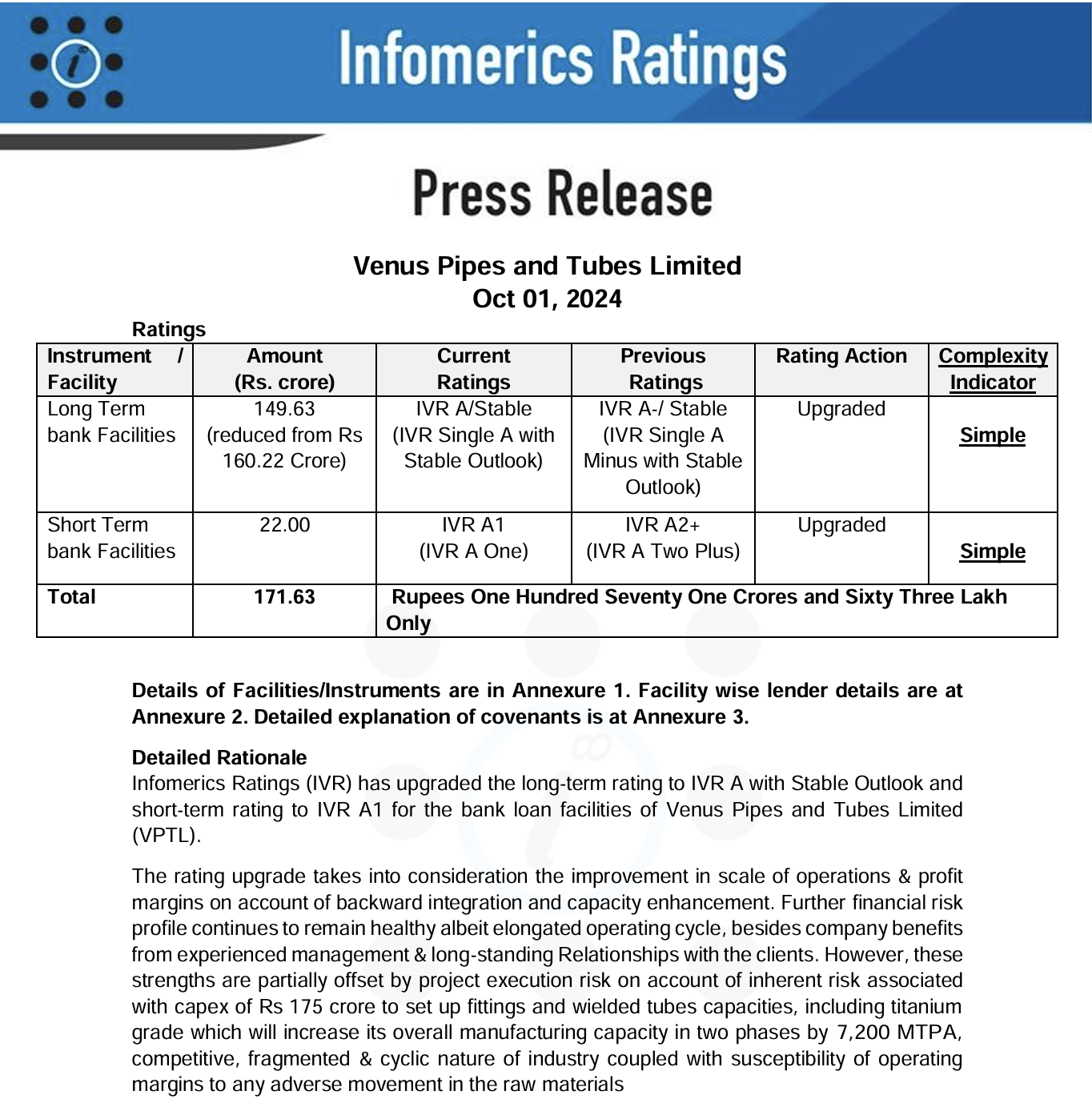

I wanted to share an important update regarding Venus Pipes and Tubes Limited. The company’s credit ratings have recently been upgraded by Infomerics Ratings.

- Long-term bank facilities: Upgraded from IVR A-/Stable to IVR A/Stable.

- Short-term bank facilities: Upgraded from IVR A2+ to IVR A1.

This upgrade reflects the company’s improved scale of operations, stronger profit margins, and continued financial health, despite a somewhat elongated operating cycle. The backward integration and capacity enhancements have significantly boosted their performance.

For more detailed information, you can refer to the latest report on the company’s financials and ratings.

Cheers!

pr-VenusPipesTubes-1oct24.pdf (288.0 KB)

4 Likes

It’s consolidating before a sharp rise. Support of 2000 is pretty strong and PE also looks comfortable. Q2 results shall make it go past its ATH. No bad news.

2 Likes

Venus pipes made a high of 1600 and then dropped to 1200 in 2023. It shot up from there and doubled to 2450 in September 2024 and dropped to 1821 today.

In both the scenarios, the correction is 25%. If Venus repeats history, I believe the fall is over and it shall start its upward journey and double from here to 3600+ within a year.

Again, this is just my observation and not a recommendation to anyone.

Disc- 8% allocation to Venus in my portfolio

2 Likes

All steel and iron companies posting record high growth but most of the stocks either on consolidation phase or correcting significantly. Wondering why

It’s because most companies in the construction and infra sector have struggled with profit margins in the ongoing Q2 results like KEI and Polycab. So, the market is anticipating the same with Venus pipes and discounting it.

Venus and similar companies purchased raw materials at higher price and now have to sell it cheaper because the raw material prices have come down. It’s a cyclical thing so nothing to worry about. The long term story is intact and it’s a good time to accumulate right now.

When everyone is fearful, it’s time to be greedy!

7 Likes

Saw this article on money control on 11/09/2024: with the title “India extends anti-subsidy duty on welded stainless steel pipes and tubes imported from China, Vietnam”. I am assuming this should be a positive for Venus in the medium to long-term? Happy to hear what others think?

4 Likes

The stock was falling because one large FII shareholder was exiting after making handsome returns

2 Likes

Where did you get that information from?

Did you get this news from any reliable source?

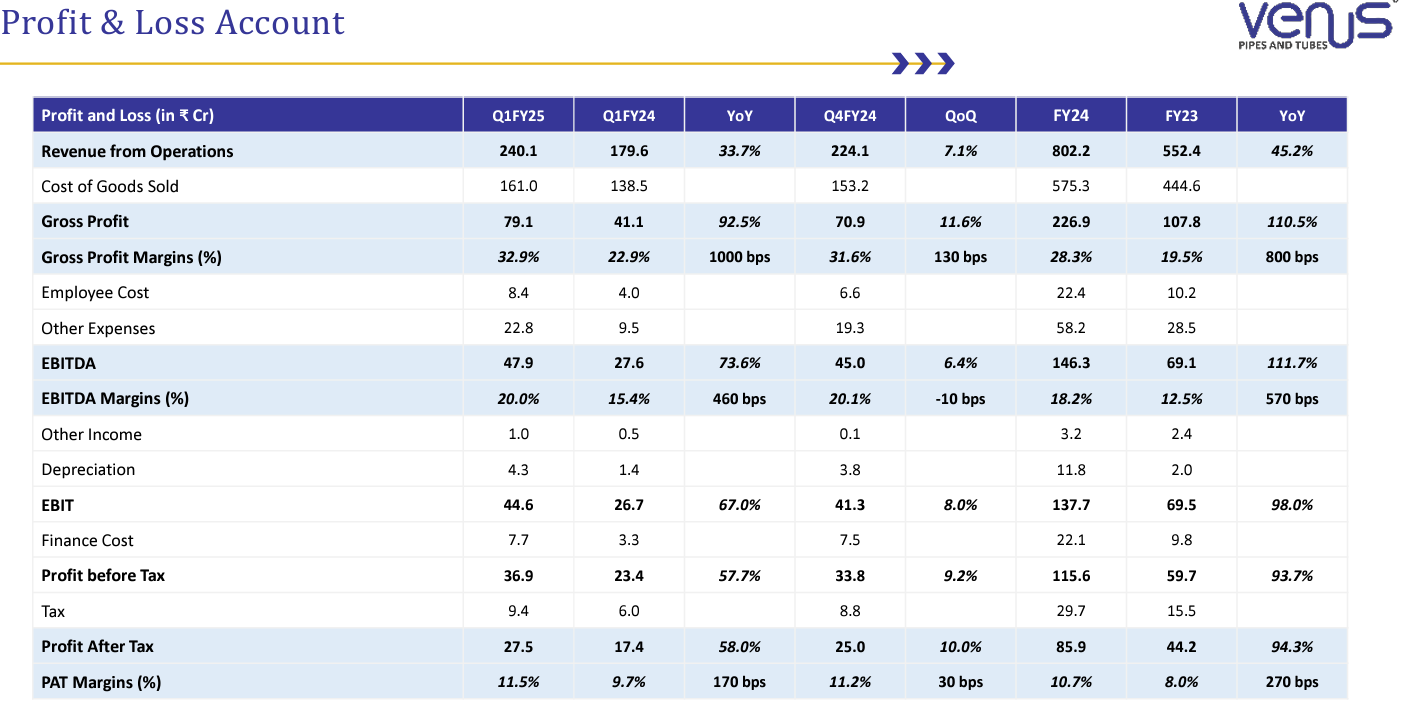

Key financial highlights for Q2 & H1FY25

Revenue of Rs. 229.0 crore, a growth of 20% y-o-y for Q2FY25; H1FY25 revenue stood at Rs. 469.1 crore, a growth stood of 26%

EBITDA of Rs 40.9 crore, a growth of 18% y-o-y with EBITDA margins at 18% for Q2FY25 and Rs. 88.9 crore for H1FY25, growing by 42% y-o-y with margins at 19%

PAT of Rs 23.7 crore, a growth of 17% y-o-y with PAT margins at 10.4%; H1FY25 PAT stood at Rs. 51.2 crore, growing by 36%

5 Likes

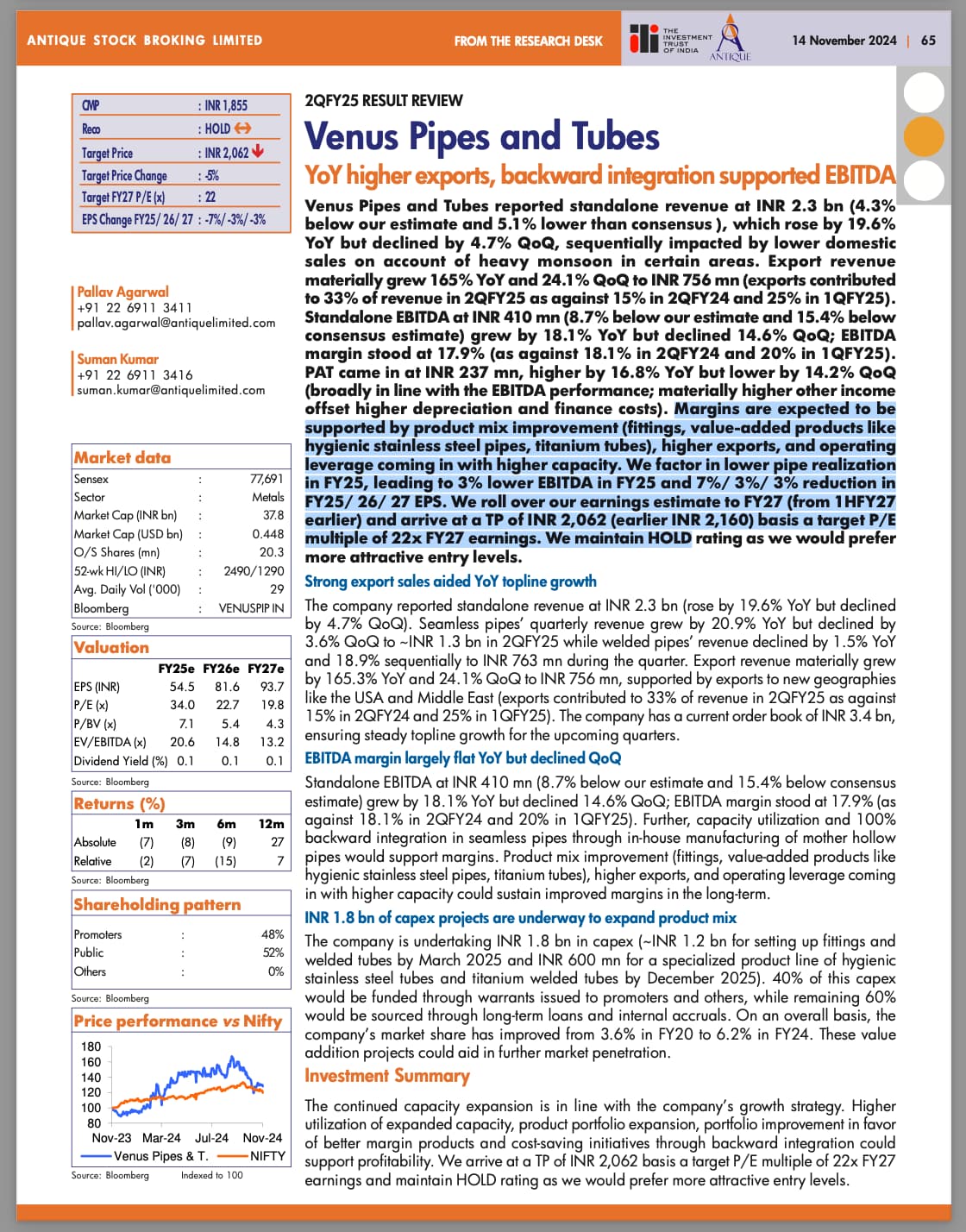

Above commendary from Antique. Domestic sales hit due to stronger and longer monsoon. Exports increase by 160%. Better results expected in coming quarters

7 Likes

Concall Notes - Nov 2024

Financial Performance:

Q2FY25 revenues reached ₹228.9 crores, a solid growth of 19.6% YoY.

H1FY25 revenues stand at ₹469.1 crores, marking impressive growth of 26.4%.

Robust volume growth of 30% YoY for H1FY25.

Achieved an all-time high order book of ₹340 crores.

Export revenue grew by 2.7X, now constituting one-third of total revenue.

Operational Highlights:

Seamless pipes sales increased by 21% YoY; welded pipes saw a slight dip of 2% in Q2FY25 but grew 13% in H1FY25.

Domestic market size expanded from 2.2 lakh metric tons to 3.2 lakh metric tons from FY20-24, with market share increasing from 3.7% to 6.2%.

Management expects to increase market share to low double digits in the coming years through foray into fittings and value-added products.

Team Expansion:

Appointed Mr. Neelanjan as Chief Strategy Officer and Mr. Mark Light as Business Development Officer (Energy).

Mr. Neelanjan brings over 20 years of experience across various industries, while Mr. Mark Light has over 30 years in international sales and business development.

Market Outlook:

Positive export outlook in Europe, with strong demand and quality on par with local manufacturers.

Anticipating growth in the US market post-election uncertainty; appointed local representatives to build connections.

Middle East demand remains strong in the oil and gas sector, with approvals from major players expected to boost orders.

Domestic demand remains solid, particularly in oil and gas, engineering, chemicals, and power sectors.

Challenges:

Some orders were delayed due to heavy rainfall, impacting domestic performance.

Fluctuations in raw material prices affected revenue expectations.

Increased ocean freight costs have softened margins despite strong export growth.

Future Growth Strategies:

Focus on expanding value-added product portfolio, including specialized tubes and fittings.

Anticipating strong second half of FY25 driven by sustained export growth and expansion into new geographies.

Capital investment for expansion is progressing, with the first phase set to launch in March 2025.

Capacity Utilization:

Current capacity utilization for seamless pipes is over 85%, while welded pipes are around 60%.

Targeting seamless utilization of 85-90% and welded at around 70% by year-end.

Market Dynamics:

Anti-dumping duty on welded stainless-steel pipes from Vietnam and Thailand may reduce imports and benefit domestic players.

Management sees a healthy demand for seamless pipes, with expectations of 6-8% market growth overall.

Investment and Capex:

Total CAPEX for FY25 expected to be around ₹150 crores, with ₹100 crores planned for the second half.

Projects are on track for completion by March 31, 2025, despite some delays due to weather conditions.

9 Likes

The only reason of this fall is technicals I’m guessing. The stock is trading below 50DMA and 200DMA.

If you find any more insights or informations kindly share for our understanding.

1 Like

I think their margins will be arnd 18% going forward. At peak, their margins were around 20%, hence the fall.

But I agree that this is a very good quality company and one should accumulate at current levels

3 Likes

According to their concall the orders were shifted to next quarter due to rainfall. I hope H2 will be better and they again sustain their peak margins.

1 Like