Sorry for asking a slightly unrelated question. But how do you invest in US equities? My only exposure is through PPFAS MF. I use zerodha and they don’t support it. I am reading that HDFC securities supports it. Please delete this post if it is not appropriate. Thanks

PF as on 1/6.

Indian equities:

ITC - 11.6%

Syngene - 10.2%

Marico - 8%

Thyrocare - 5.8%

PPFAS MF - 8.2%

Quantum MF - 3.1%

US equities:

Facebook - 18.7%

Fiverr - 11.3%

Google - 7.2%

Debt+other - 13.3%

Cash - 2.7%

Fiverr managed to do impressively well as stock moved from 18$ to 63$. However allocation to PF initially was small. Inspite of concerns above about Facebook, it has delivered 28% returns(plus around 10% in currency depreciation) over the last 1 year. Syngene and Marico have done well too. Thyrocare and ITC not so much.

I’m collecting cash from salary currently for comfort. Haven’t added much to equity part in last 2 months.

How can we invest directly in US equities from India?

1 Like

Scroll up. I’ve posted a link.

Hey,

Can you in brief talk about Fiver, talk about your rationale and then the current valuation? If you don’t mind should be very helpful

It is an online marketplace and almost has a monopoly in easy to buy freelancer/gig economy market. I had invested at P/S of 4-5 but it has since run up more than 4x in INR terms. I’m not sure valuations are cheap anymore at EV/S of 17.5x to offer margin of safety, but doesn’t mean it can’t deliver good returns going forward. It will continue to grow at around 45%.

Hi. I am from health sector. Just wanted to give my view regarding Thyrocare. Apart from technicality and all fundamentals, we do have trust issues with thyrocare. Most of my patients who come from north and east part of India does their test from Local or Lal Path Lab. Here in Delhi we also prefer Metropolis for specialised test. New players like Quest, Helathians etc are taking market share in Metro due to pricing power. In south Metropolis has also strong presence esp Maharashtra. The franchise system in thyrocare is bad and gives false reports on many occasions. This may be narrow range view, but you may check into if they are not fudging their balance sheets and also if any other avenues they are growing into.

Thanks for the concern. My Mother operates a lab and deals heavily with Thyrocare. She has only had good things to say about it. Thyrocare’s moat is in volumes and it is unlikely other players will manage to breach that anytime soon. I don’t think we should discuss in depth about a specific portfolio stock, especially when they have their own threads.

I remain positive on the company and would have allocated a higher position to Thyrocare if not for their capex heavy Nueclear PET-CT business that I do not like.

So how do you research US stocks ? Any website or subscription you are following.

The only website I like is Seeking Alpha. Rest is by reading ARs, sector knowledge, concalls etc.

1 Like

There are few websites which gives the financial information like morningstar.com, Yahoo finance, tikr.com. seeking alpha and Motley fool gives very good articles and AR, 10k, company websites give good information about US companies. www.tikr.com gives 10 year financial results including detailed cash flow which is very useful

2 Likes

PF on 1/8.

Indian equities:

Syngene - 11%

ITC - 9.9%

Marico - 7.3%

Thyrocare - 6.6%

PPFAS MF - 8.4%

Quantum MF - 2.9%

US equities:

Facebook - 16.8%

Fiverr - 13.3%

Google - 6.2%

Debt+other - 12.6%

Cash - 7%

2 Likes

Hi Varun, you got good concentrated profile, the companies you own are making all time high. Could you also share your selling/ profit booking strategy ? Thanks !

Hi ak83. US stocks, which I’ve been adding since last 1 year or so is up 94% in USD terms(and likely >100%) in INR terms on absolute basis. Individual Indian individual stocks are up around 28% since YTD.

I have not taken any gains off the table and am riding it out.

1 Like

PF on 1/11

Fiverr (US) - 20.4%

Facebook (US) - 18.6%

Thyrocare - 10.3%

Syngene - 10.1%

ITC - 8%

Marico - 6%

PPFAS MF - 7.5%

Quantum MF - 2.6%

PPF+other - 8%

Cash - 8.5%

Fiverr completed the magical 10x(in INR terms). Facebook & other Indian holdings other than ITC have done very well too. Sold out of Google as I felt core search product had growth slowing and headwinds coming up.

4 Likes

Wanted to update my PF.

Fiverr(US) 28.5%

Facebook(US) 27.1%

Syngene 9.1%

ITC 8.5%

Marico 6.7%

Quantum MF 3%

PPFAS MF 10.3%

PPF 6.8%

Net addition has been little. I sold out of Thyrocare due to promoter’s micro-management and high valuations. Cash+proceeds from sale was used to increase allocation to US stocks. Don’t hold any cash, haven’t done so since Jan.

Going forward I want to take money out from Quantum since it’s a small position. Waiting for ELSS lock-in to finish.

3 Likes

I really appreciate your concentrated profile and stocks you own are doing great. Specifically for Fiverr, which is now consolidating at ~200 levels after the high of ~330, whats your take on it ? I have not checked too much details about the company/financial but the company is yet to be profitable, do you think it could be turn around company and how it is better than other freelancing platform.

I really appreciate your concentrated profile and stocks you own are doing great. Specifically for Fiverr, which is now consolidating at ~200 levels after the high of ~330, whats your take on it ? I have not checked too much details about the company/financial but the company is yet to be profitable, do you think it could be turn around company and how it is better than other freelancing platform.

Companies like Fiverr have high front loaded costs(marketing, admin). Important thing to check is gross margins and marketing efficiency. With 83-85% gross margin, long term EBITDA margins should be around 45-50%. Due to strong WC, CFO margin should be ~50%. At CMP, you’re buying it at normalised forward EV/CFO of 47x or EV/EBITDA of ~50x, with long term growth at ~45-60%. You decide if that’s expensive(or not)!

Most of my buying has been at much lower levels(20-40, then some at 160 and 190) and position has run up so looks optically high. I can’t advise you what to do. I continue to hold it because TAM and opportunity is much much higher than current MC/EV.

I personally like FB more at current levels. It’s trading at NTM EV/EBITDA of 13.5x, with revenue growth at 20-30%. I would be comfortable paying 2x CMP for it. I feel regulation and anti-trust concerns are overblown, but emergence of AAPL as a competitor can’t be ignored.

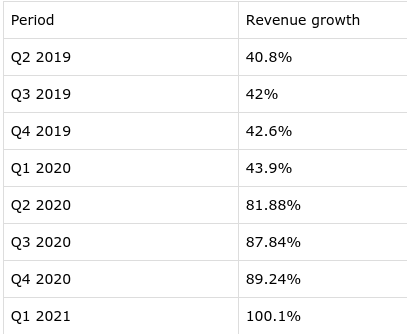

To add another important aspect for Fiverr is network effects that should accelerate revenue growth further. These are the YoY revenue growth figures for last few quarters.

2 Likes

Thanks for sharing the info !

1 Like