They have multiple capex projects going on,part of the facilities have been commissioned and they are at the stage of trial production,rest are under construction hence the difference in figures.

3 Likes

Hello all,

I have read the complete thread and have a few questions from those invested here.

-

What is the reason for Aarti to have a subsidiary to manufacture the same product that they already do?

-

Is there any signs from the management to move the stock from BSE SME to BSE and NSE?

-

What stops other competitors to enter chloro phenol production? ROCE is 93% with excellent net margins. Is the shift in production to India temporary or sustainable. Company trades at juicy valuations. But very confusing to understand sustainability and growth prospects.

Disc: No holdings

4 Likes

Debt is increasing still no credit rating. Further, today director has disposes 750 shares. Any idea, what is the outlook of the company.

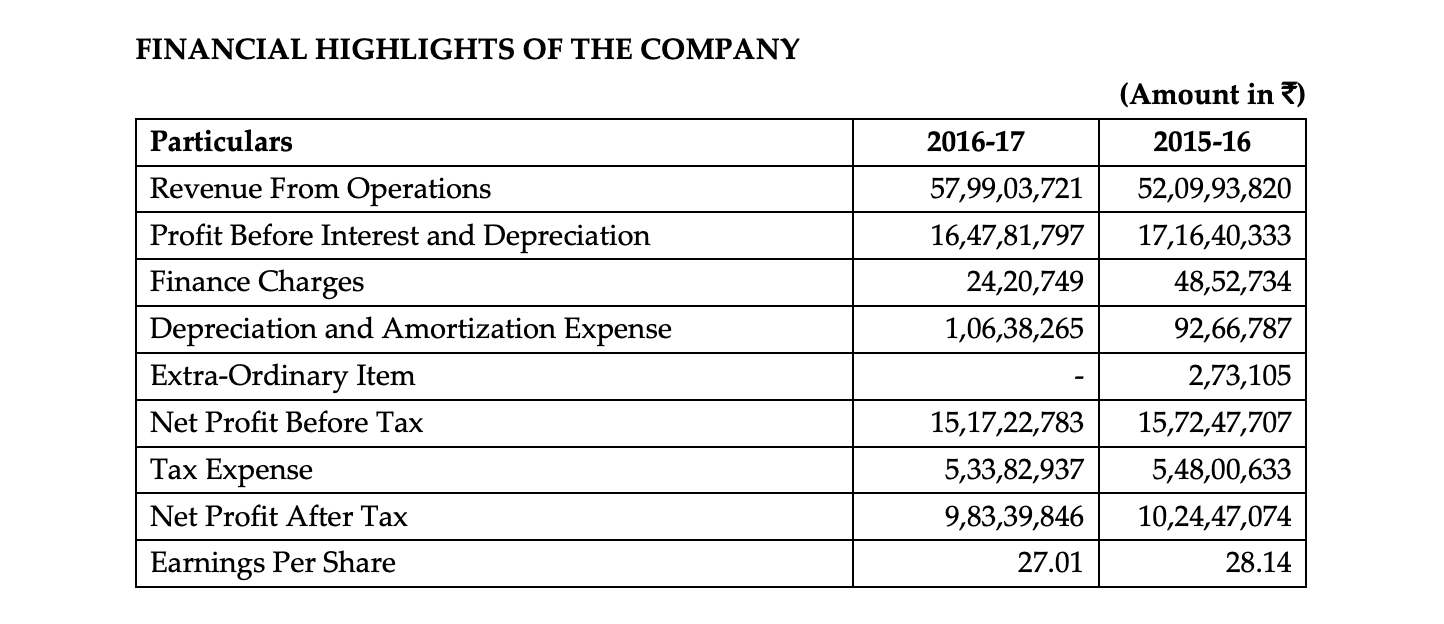

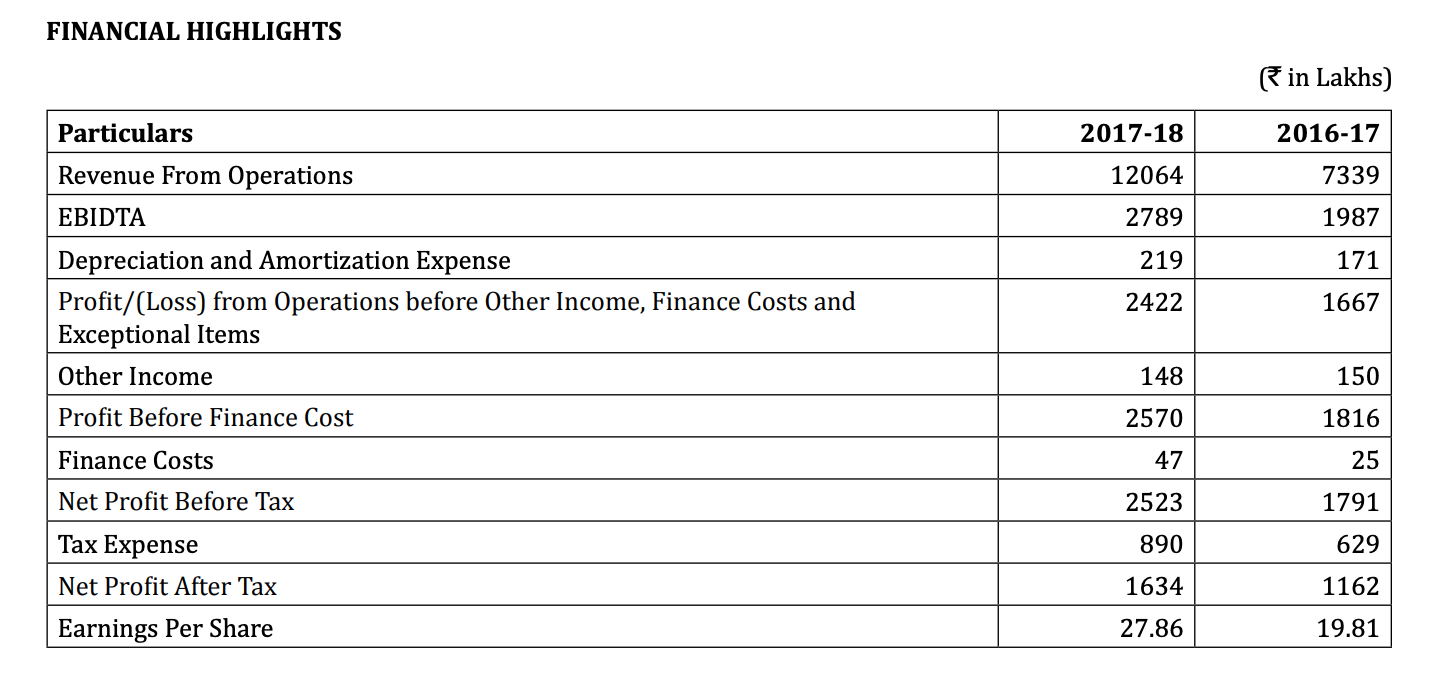

Hi everyone, this is my first post. I was reading the past reports of VOL and found some difference in their reported financial highlights of 2016-17 so thought of asking here. I’ve attached the screenshots.

Can someone please enlighten why this 2016-17 number difference in different reports? Am I missing something?

Though holding by promoter group is less than 50%, still they are gradually disposing the shares. Disposal of 84,000 equity shares worth Rs 1425.60 lacs by promoter groups. Any reasonable explanation. So far no credit rating also. I am not getting any explanation of these things.

1 Like

There are different reasons for which promoters sell. Not always to evade any bad tidings. If you notice Valiant has diverse set of individuals as promoters/ directors- all assembled due to the various companies taken over. These individuals may/ may not have substantial role to play now that Gogris of Aarti Ind are in driving seat. Hence they would exit/ feel compelled to sell for their own needs. I would not read too much in the action. In any case once the stock shifts to main board smaller investors may be able to enter obviating the need to buy minimum 150 shares.

2 Likes

Will list tomorrow(Sep 04,2020) on the BSE mainboard.

Link:https://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20200902-24

- DRHP availabe at link here, on page 78 mentions and I quote

Further, the Company also requires steam for the boiler usage. The same is purchased from our Group entity – Aarti Industries Limited.

How can a company buy steam for boiler from another company unless they are on same premises and their plants for all practical purposes integrated.

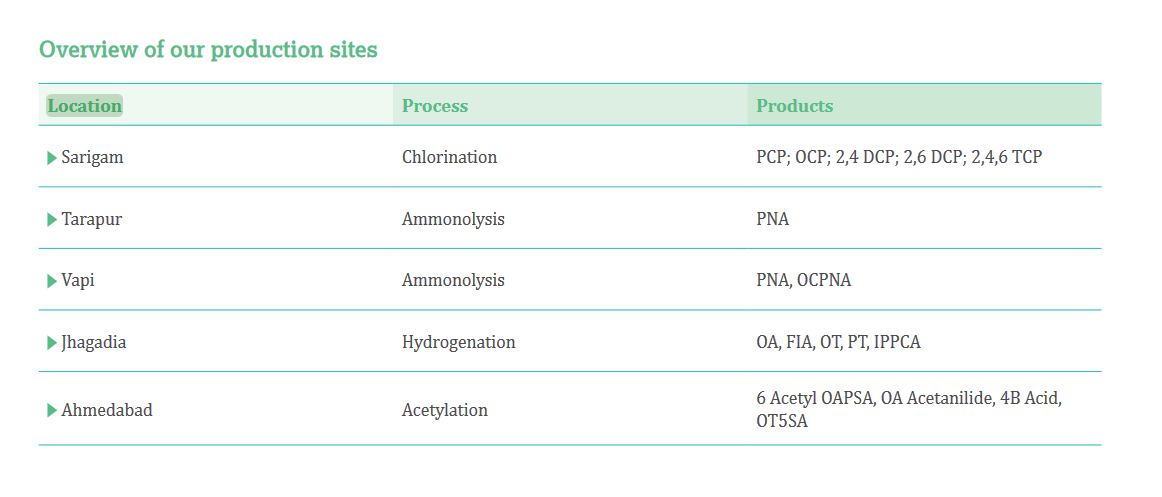

I also checked the latest annual report of Aarti Industries except for Ahmedabad (which I could not confirm) the plants of both the companies are at same location - Vapi, tarapur, jhagadia,sarigam.

I have not seen a single image of plant of Valiant organics.

- Who are the clients of the company? I have read the full thread, drhp and latest annual report but failed to see single mention of name of any of the clients of the company. Is it Aarti Industries again? The company has mentioned that they buy Chlorine from Gujarat Alkalies but no mention of any of the clients!

Clients are BASF, Lanxess, Coromandel, Bayer, Gujarat Insecticides - It is there in the Annual report - please check Page 7 of Annual Report

2 Likes

All their plants are visible from the sky on google maps. It’s amazing the fact that you’ve not done much deep research at all. Valiant and Aarti operate out of the same building on different floors. Valiant’s original plants are extremely integrated into Aarti and all are in close proximity to each other.

4 Likes

I stand corrected.

Therefore, Valiant is in-fact is a “paper company” with certain assets of Aarti Industries put up separately in file and shown to investors as a company.

Please read annual report and visit their website to understand before concluding anything.

Regards,

Raj

1 Like

Excerpts from Mr.Arvind Kanji Chheda’s message to share holders (AR 2019-2020)

Top line : 584 Crores as compared to 606 Crores in the previous year due to loss of production in mar 2020 .

Net profit: 139 Crores against Rs 121 Crores Y-O-Y ( higher by 15%.)

EBITDA increased 5% at 193 Crores, compared to 184 Crores in the previous year.

Earnings Per Share stood at 114.02 as compared to 99.82 in the previous year .

Export to various geographies across the globe contributes 15% to top line .

Acquisition of Amarjyot Chemical Limited during the previous year helped to attain increased manufacturing capacities and also provided significant depth to product offering with a wide spread of value-added products commanding a niche and value-added product portfolio that find applications in dye, pigments, pharma and agro-chemical intermediates industries.

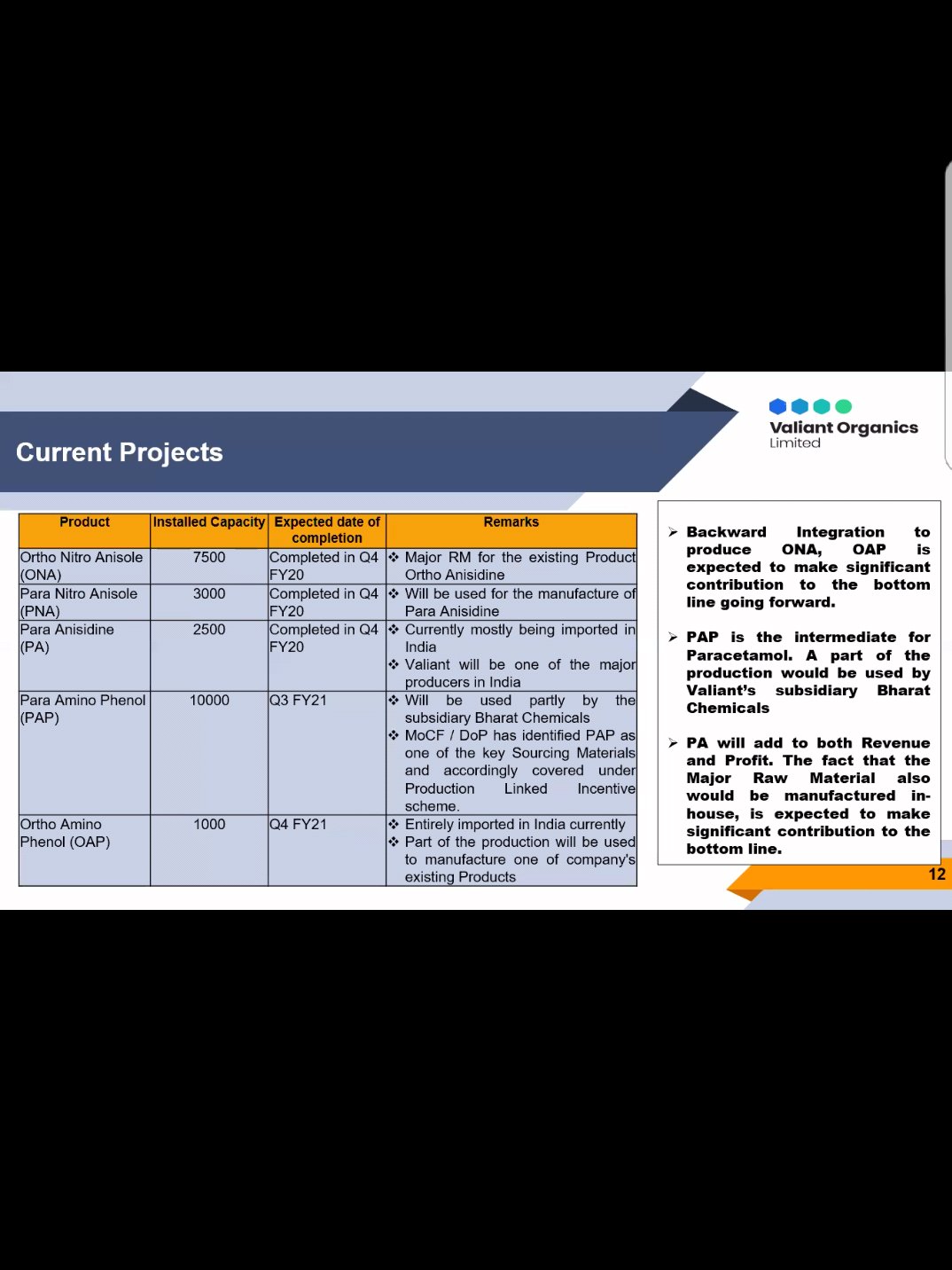

Increased Chlorophenol capacity to 18,000 MTPA from 4800 MTPA by completing the expansion at the Sarigam plant in 2 years

Added Ortho Nitro Anisole and Para Nitro Anisole .

Undertook expansion at the Jhagadia plant for hydrogenation. Backward integration that enabled in manufacturing key raw materials in-house and in providing significant cost savings and better profit margins. 3 new projects with the estimated capex of Rs 100 cr

Increased the capacities of our hydrogenation products from the earlier 18,000 MT per annum to 26,000 MT per annum.

Increasing the Ammonolysis capacity at Tarapur and Vapi plants from 13,000 MT per annum to 16,000 MT per annum.

Likely to commence operations of Para Amino Phenol (PAP) and Ortho Amino Phenol (OAP), which are import substitutes, in the second half of FY 2020-21.

PAP has been identified as key intermediates of pharma products by the government, which is to be incentivised under recently announced PLI Scheme .

The management is considering to set up a plant for Paracetamol with other drug intermediates and APIs in future .

Tarapur, Vapi and Jhagadia plants are in the process of being automated to improve operational yield, cost efficiencies, and safety and to reduce human intervention .

Land bank of 68,000 sq. metres at Sayakha and Dahej, Gujarat, to further develop new products.

Due to closure of many chemical plants at China and increase in cost for the balance plants due to stringent environment & safety norms, Valiant Organics Limited, is well positioned to capitalise on these emerging business opportunities by significantly leveraging operations, expanding capacities and extensive domain knowledge.

Well prepared to take advantage of the growing opportunities in specialty chemicals, as India’s specialty chemicals market sets itself on the growth path for the coming years, and with a rising need for specialty chemicals in the end-use domestic markets. Added specialty chemicals to the portfolio and continually updating product mix and consequently well positioned to capture this growth and become a leading specialty chemicals player in India , delivering sustainable stakeholder growth

7 Likes

Status of projects both commissioned and upcoming as mentioned on listing day. This Arti group co is destined to go to next orbit once these projects making china substitute projects which will be mostly manufactured for first time in India gets commissioned.

Dicl- Invested since ipo@220 in 2016 n bought more on listing .Paisa quality stocks rakhne se banta h. Stay invested as long as tailwinds are strong under ethical promoters who execute well n hv a growth mindset , are the key learning which all VPers must assimilate.

10 Likes

Thank you for your input. Would it be possible to quantify any ballpark additions to the topline and bottom due to these commissioned projects? What benefits would be accrued due to the PCI scheme if you are aware of any?

Thank you for sharing.

Disc: Invested.

PCI Scheme query answered in the abovementioned slide.

I am looking at broader picture with 90% bet on promoter & rest on sector with tailwinds.

U or others VP may do homework of nos projections for next 2-3 years plz.

I am going to be invested for next 2-3 years as tailwinds I believe will be there till then. Peter Lynch also says that the best returns come for those investing today in 4th & 5th year of investment.

Go thru this wonderful thread on this wonderful forum which wud hv created huge wealth for the laborious members who bothered to read the full thread.

7 Likes

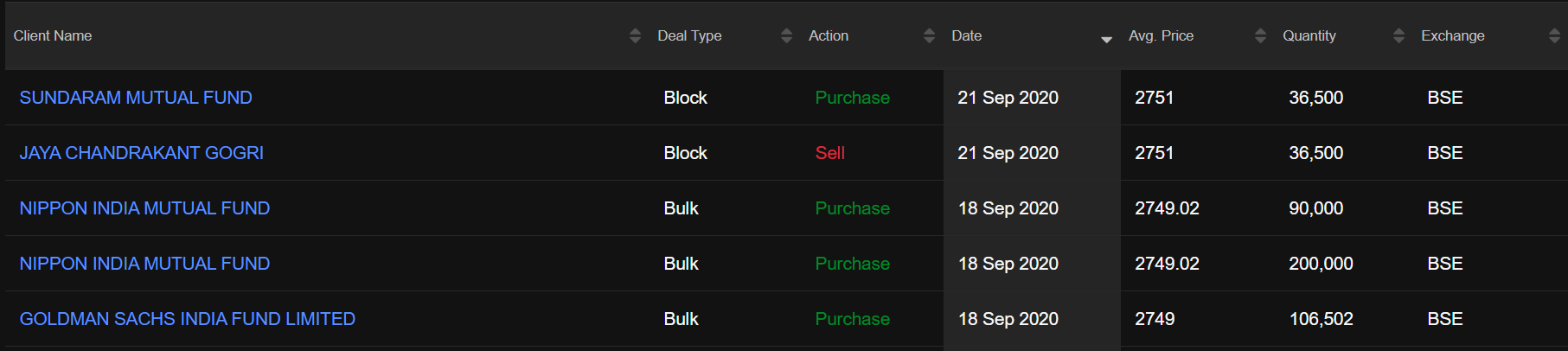

FII ENTRY IN VALIANT ORGANICS

GOLDMAN SACHS INDIA FUND LIMITED purchases 106,502 shares of valiant organics for an average price of 2749 on 18.09.2020.

3 Likes