I see a lot of people don’t understand sales potential for capex done by Valiant given somewhat complicated chemical terminology and inability to understand end use cases.

I tried to dig deeper to access the total addressable market for PAP which is an import substitute and used as an KSM for API manufacturing of paracetamol and also comes under PLI scheme announced by GOI. Below are my findings.

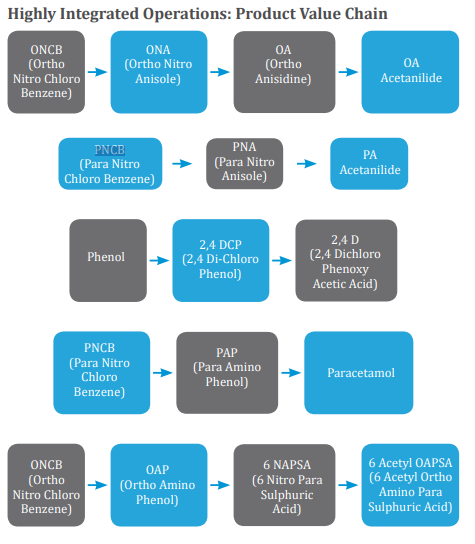

- Paracetamol can be prepared from benzene (key starting material) which is first converted to PNCB (para nitro chloro benzene). Then PNCB is converted into PAP (para amino phenol). PAP is widely imported from China by Indian formulation units because of a wide price margin. It is then used to make the paracetamol API and finally the tablet. (source). (Also see 4th line item in the below chart from Valiant’s AR)

- Currently India imports all 21,000 TPA of its PAP requirement from China. Although based on paracetamol’s capacity, India’s installed base is ~38,500 TPA.(link)

- July PAP pricing remained slightly high at about Rs 227 per KG. On sustainable basis we can assume it to ~Rs180-200 per KG. (see below chart)

- That arrives to about Rs. 400 crore of TAM for PAP (21,000 tons * Rs 190 per KG)

Now there are some important points to consider and take the discussion forward. I would request fellow VP’ians to add their viewpoints:

a. How many other such chemical/pharma companies have ability and chemical knowhow to produce PAP from Benzene derivatives? To my understanding Aarti group is one of the leading producers of Benzene derivatives in India but request other VP’ians to please correct me if I am wrong. If Valiant is the sole player here (which is highly likely, given Aarti’s Benzene dominance in India), we can see entire Rs 400 crore of sales flowing to Valiant. That would imply asset turnover of 4x (on Rs 100 crore of capex done) which seems very high. Maybe they capture 30-50% of PAP market initially and then ramp up from there. This is all an assumption.

b. We need to understand economics of these PAP and Paracetamol API products. Given PLI incentives involved, I have my doubts regarding 30+% EBITDA margin on these products (Valiant’s existing margin structure can come down if these are lower margin products and so can return ratios).

PS: PAP looks like a very decent opportunity and can scale upto 60% of their FY20 sales. We need to be mindful of margins and working capital terms for this new business.