Here’s the latest Investor Presentation - Q4 FY 2019-20:

My thoughts are as follows :

Water Sector will be one of the hot-topics in the coming decade.

Increasing budget allocations from Corporates, Governments, Multi-lateral Organizations, etc. with every passing year

Defensive Sector/Theme (budget allocations irrespective of whether GDP is expanding or contracting)

Very few Indian players with vast expertise, experience and geographical presence.

Please let me know in case there are any other listed companies in this space (directly or indirectly). Having volunteered for an NGO in this sector, I’m super bullish in this thematic play…

However, I completely understand the inherent challenges and risks at play here.

Razor thin margins (9% operating margins and 3% net margins approx.)

Working Capital challenges (heavy capex requirements)

Dependence on Governments for payments

Lack of clear Government policies on water management (esp. in developing countries)

and the infamous APGENGO overdue amount

Given the nature of industry, I don’t expect any changes happening in the first three challenges/risks any soon.

However, even if Wabag just survives (not even thrive) in the coming decade, that’s more than enough for good returns over a 5-7 years horizon, at the current valuations. On top of it, if Wabag can recover overdue payments, or gradually work on decreasing Debtor Days or get more efficient in project financing and capital allocation skills, or win more private contracts, then you have a multi-bagger.

So, at current valuations, I see an investment option with limited down-side but very good up-side. Just that it’s in a boring sector with a slow rate of change. So, it may need higher levels of patience and conviction.

PS: I’m invested, so my inherent biases are clearly visible all over the post I suppose…

Low oil prices will reduce order book from middle east

Positives:

very strong order book

very strong technological hold (european subsidiary keeps them ahead of curve)

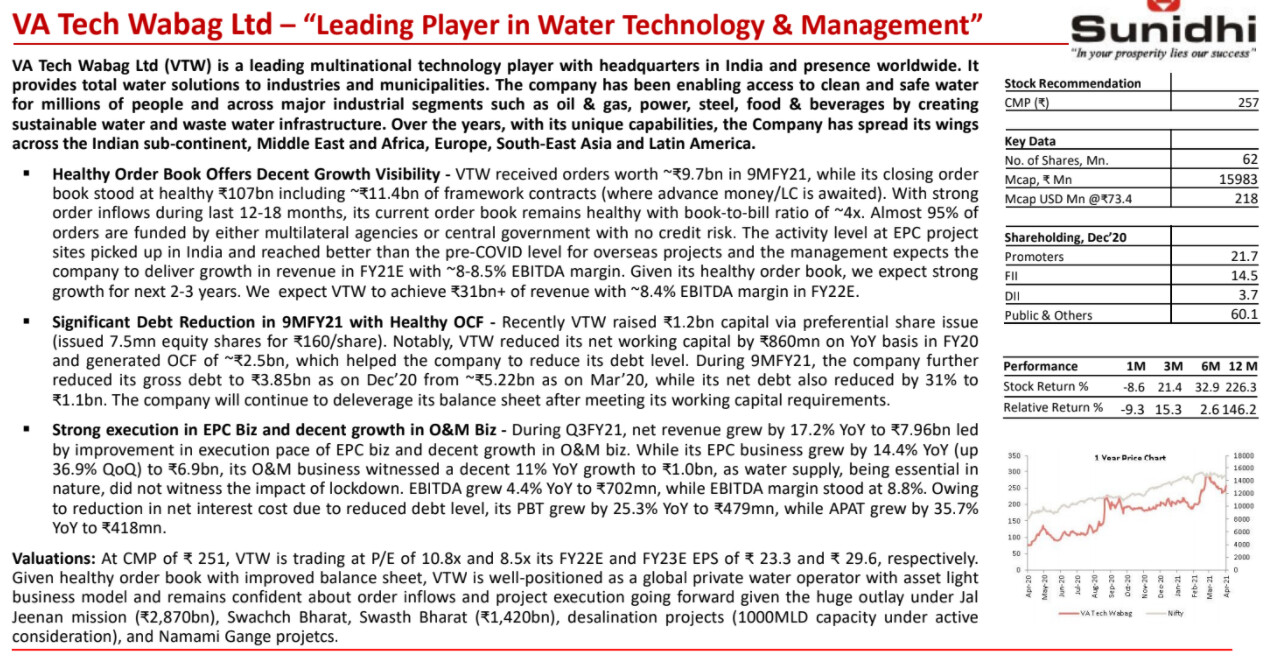

I believe a lot of negatives are already baked in the prices. They had picked up on execution right before COVID and can pull back margins to 3.5-4%. If executed well, next year expected profits could be close to 100-120cr range. Any further PE upside can only come post APGENCO receivables come in (if ever they come)

While I am not a prolific poster, Valuepickr has always been about taking a discussion forward with self effort. In this case, what you can do is first go through relevant links for VA TECH and ION EXCHANGE as well as other content like financial reports. Then you post your thesis on comparison and invite other people to comment. Asking a standalone qn for a direct ans is not how VP is designed to be.

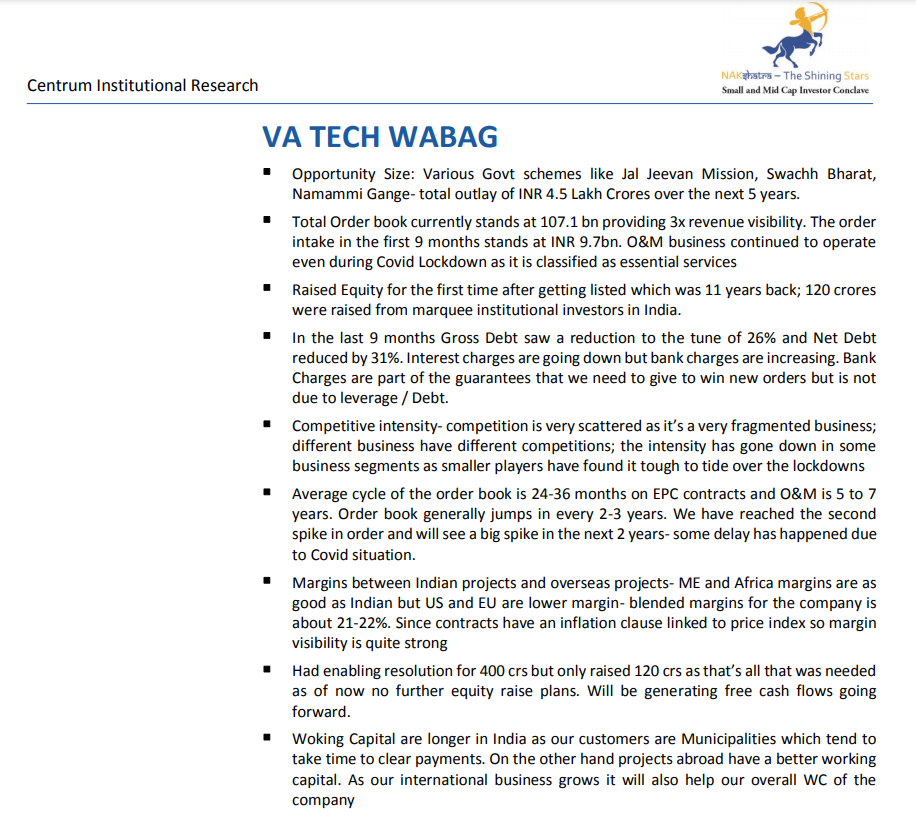

Conference call takeaways

Order inflow pipeline is currently skewed towards international projects as activity

levels on domestic orders has still not picked up pace. Management highlighted that the

company is favourably placed in two large international projects.

VATW expects to achieve financial closure for the Rs 5.7bn Kolkata HAM project in

3QFY21. Execution of the DBO portion is expected to pick up pace in FY22.

Has commenced revenue recognition on the EPC portion of Rs 12bn Bihar project and

should be reflective in 2HFY21. HAM should start contributing to sales from FY22 as

financial closure is still pending for the same.

Ion Exchange vs Va Tech Wabag seems to be like what Buffet says: A great company at a fair price vs a fair company at a great price. He always preferred the former

Seems to be a good business. But while going through the screener data , I find the return ratios for last 3 years are extremely poor… is the data wrong ? No dividend declared so far ?

And promote stake is just 21%.

And as an investor, I am bit skeptical, I may be wrong though.

Am I missing something somewhere…??

Disclosure: tracking the company …not invested

Yes, last three years have been difficult for the company, it has to takeover Andhra Genco projects and around~600 crores got stucked. But last year, it raised 120 cr from, inter-alia, Mr. Jhunjhunwala. As a result, it’s project execution speed has picked up. Greatest moat about the company is its technology, due to which it has a large order book (~3*revenue). Future depends how the execution of order book materializes. (Market is writing off ~600 cr.)