Arvind Lifestyle sells Unlimited stores to V-Mart

Read more at:

Arvind Lifestyle sells Unlimited stores to V-Mart

Read more at:

Q2 FY 22

This also comes at a time when the fashion startup is struggling to keep up with competition from online players like Amazon, Flipkart, and Myntra. So far, LimeRoad has raised over $50 million from marquee investors like Matrix Partners, Tiger Global Management, and Lightspeed India Partners.

.

V-Mart will also invest Rs 150 crore to help LimeRoad achieve profitability, it said in a statement. The listed entity currently has a network of 450 stores across the country, while LimeRoad is said to have achieved over two lakh downloads per day along with a gross merchandise value (GMV) of Rs 700 crore. GMV is a commonly used term that refers to the total value of goods and services sold over a period of time by a retail company.

.

LimeRoad will operate as an independent entity under the V-Mart label and the startup’s CEO Suchi Mukherjee will continue her role.

.

The sale is likely to help V-Mart strengthen its online presence through LimeRoad’s user base of five crore online shoppers in Tier II and III markets.

I belive this acquisition was bound to fail from day 1.

Limeroad was already in decline and Vmart don’t have the management capabilities to pull them out.

If one visit the site right now, you will be surprised to see similar content getting repeated.

This is more important when you are competing with likes of myntra and Amazon.

E-commerce require razor sharp focus and very detailed execution. Vmart was already sloppy with their own stores (one should visit Vmart stores and check visual merchandising).

One can clearly see the difference between the two and it will increase with time.

I believe vmart may have acquired limeroad with right intention (establish a online presence) and with right price (distressed sale) but they have underestimate the amount of effort to make it successful.

VMART Q4FY23 Concall Summary. Management says to analysts please be patient and build your models accordingly ![]()

Any ideas on how could you market size V-Mart’s potential customers?

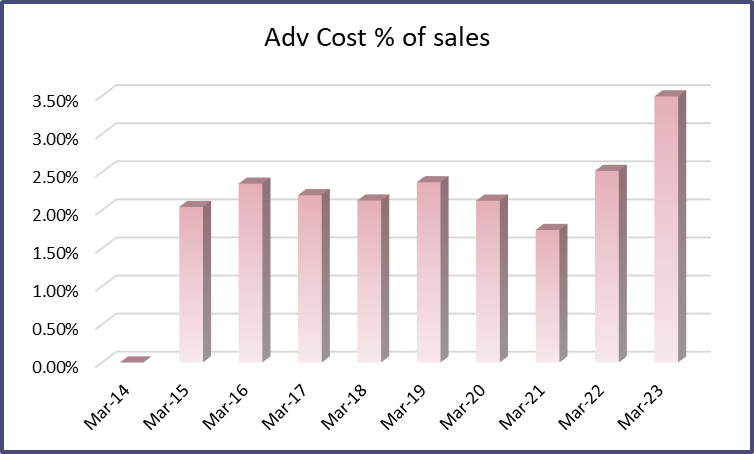

Vmart is Investing for the future, More than doubled its AD Spends from 41 Cr to 86 Cr.

My view - I see some shift in demand and opportunity due to - 1. Offices opening specifically - IT Service 2. Festive time around 3. Rainy season almost in the last leg .

Disclaimer: Invested small amount. Pls do your own research and take advice from your adviser.

VMART Retail Q2FY24 Concall Summary

Few pointers:

Mgmt strategy is to reduce offline ASPs (attract footfall + push sales volumes) and online ASPs to be higher: Slightly confused how this works as most others generally have it the other way around to get rid off stuck inventory etc.

Almost 80% of old inventory is out of system and rising payable days is reducing cash conv cycle

H1 FY24 sales > H1 FY23 sales in spite of delayed diwali + adhik mas included in FY24.

They have a slightly higher churn rate in terms of stores closures i feel, 12 last FY and 3 already current FY. Maybe the older ones are struggling due to competition. (They open new stores in Tier 3 under exposed cities)

Opened 57 stores prev FY, target of another 50 this FY. Could be interesting if they can sustain this pace, doubtful though.

V-mart still looks abysmal at current valuations (In mns)

FY26 Ebitda- 4,388(12% margins after 16% growth on FY24 numbers)

Rent payment - 2,481(2050 for current year, 10% growth for two years)

Capex - 600 ( stable state)

FCF - 1,307

Market cap - 42,570

P/FCF - 33 times FY26

This is even without factoring any working capital requirements

Hi - anyone here tracking V-Mart closely and still optimistic or foresee a turnaround considering overhang around Limeroad acquisition, rural economy, rising competition with big brands making inroads into smaller cities? Holding a big position and contemplating switching out. Having second thoughts considering the size of opportunity here. Thanks in advance

They’re churning out underperforming stores basically reducing high cost rentals, focusing on increasing units sold only (volume) rather than ASPs. The strategy is to wait and play for the compounding effect to play out: If I buy something and price seems fine, 1. Will probably increase frequency of visits 2. potentially buy more 3. recommend others who might repeat the same process.

And we cannot wait forever for this to play out, so once mgmt feel alright we are getting the volume growth, they will look to increase ASP once the retail upcycle kicks in.

May want to wait and watch how this plays out.