|

Call addressed by Mr. Mithun Chittilappilly MD/Key Highlights by Capital Mkt;

For FY'14, net sales grew by around 11% and stood at Rs 1537 crore. South markets which contribute about 70% of total sales, grew by 4% and Non South market which contribute about 30% of total sales, grew by around 34% YoY. The company has about 20000 dealers, 400 distributors and 4000 channel partners. Going forward, the sale will be more from channel partners, which will reduce the overall working capital requirements of the company. Also there is tremendous scope to improve the sales from existing dealers and distributors in non-South market as compared to sales from existing dealers and distributors from South market. Also there is scope for improvement of average realization from non South market. The Electronics segment, which constitute stabilizers and UPS, which contribute about 30% of total sales in FY'14, degrew by 2% YoY, Electrical which includes pumps, house wiring cable, electric water heater, fans and others, and contribute about 68% of total sales, grew by about 18%, with electric water heater and house wiring cables delivered a healthy growth, while the solar water heater which constitute about 3% of total sales, grew by about 20%. The premium variant of the electric water heater segment launched in FY'14 continues to get good response. Also the induction cooker and mixtures business grew strongly and will start contributing in FY'15 in more effective way. Management expects advertisement spend to continue to hover around 3.5-4% of net sales in FY'15 as well. In FY'14, inverters, de grew by about 28% due to surplus electricity being provided in Southern market due to elections. However, now with elections getting over, the peak summer demand has already started showing strong traction for inverters. Management expects inverters will drive growth in FY'15. Also the wires business is expected to continue its strong growth of about 20-25% given low base and ample opportunity to tap the unorganized market. Overall, for FY'15, management expects net sales growth of around 20% with Ebidta margin of around 8.5-9%. The growth will be led by inverters, stabilizers, wires, electric water heaters and water pump business.Not much capex is expected in FY'15. Tax rate for FY'15 will increase from around 25% in FY'14 to around 29% as two of its factories are losing the 100% tax free deduction and are entering the slab of 30%. |

|

Calladdressed by Mr. Mithun Chittilappilly MD;Key Highlights by Capital Mkt;

Net sales for Q1 FY'15 grew by around 17% driven by strong sales growth in stabilizer, fans and inverter segment. Strong summer and delayed monsoon also helped the sale of these products. Non South Market grew by around 31% in Q1 FY'15 and company gained market share in many product categories. Non South market contributes about 35% of topline as compared to about 31% on YoY basis.Company continue to invest in advertising and promotion activities and management expects ad spend to continue to be around 4% of revenue.Tax rate for FY'15 will increase from around 25% in FY'14 to around 29% as two of its factories are losing the 100% tax free deduction and are entering the slab of 30%.Capex planned for FY'15 is around Rs 15-20 crore. As per the management, it was more of a favorable weather that drove the growth rather than improvement in Consumer sentiment. While sentiments are positive it will take some time to convert them into realty. Management is confident of strong consumer momentum to drive the growth going forward in years to come. Rural revenue was about 50% of total sales and was primarily from pumps, invertors etc.Management expects Cables segment to continue to grow in strong double digit as the company moves this business beyond Kerala and Karnataka and to other Southern and Non South Market. Cable business to grow from around Rs 475 crore in FY'14 to around Rs 700 crore in next 3 years. Management expects Invertors business to grow strongly after a continuous fall for the past 18 months. However a lot to do with how the power scenario develops. Within the invertors space, the Industrial segment share to go up and will drive the growth. In long term, the solar invertors panel will drive the growth. The company is already working on the project for the past couple of years on the same.Management expects Non south market to continue to grow around 35% and South market around 10-12%. Overall, for FY'15, management expects net sales growth of around 20% with Ebidta margin of around 8.5-9%. The growth will be led by inverters, stabilizers, wires, electric water heaters and water pump business. |

Call add by Mr. Mithun Chittilappilly , MD of the Co. Key highlights by Capital Mkt;

- Net sales for Q2 FY15 were up by 29% to Rs 431.3 crore while net profit inclined by 32% to Rs 19.2 crore. OPM inclined by 17 bps to 8.1%.A strong growth recorded in the digital UPS, electric water heater and stabilizer.Digit UPS jumped up by 138% from a low base and stabilizer grew by 25% as power issues in southern states continued

- The mgmt said that inverter segment is under huge pressure since last few years however with demand for power increasing long term prospects remains positive.The launch of new brand called âPebble' in electric water heater on pan-India basis has given lift to its water heater sales

- OPM was impacted due to one-off expenses which includes warranty cost, related to change in after sales service model and new call center services worth Rs4.5 crore in this quarter.The advertising expenses was around 3.3% of sales in this quarter and going forward the mgmt will keep advertisement spend around 3.5-4% for the full year.The south market witnessed a 21% growth on a high base in Q2 FY2015. Growth in South markets was driven by old Andhra Pradesh which has grown by 40-45%, as last year there was disturbance in market which impacted the growth.

- The non-south market registered a robust growth of 47% on a low base and the share of revenue from non-south market touched 33%. Stabilizer, wire, electric water heater, pumps and inverters are main products which are marketed in non-south market.Net working capital days were up from around 70/71 days to 81 days largely due to inventory pile up for winter and festive season ahead. The mgmt said that October saw better offtake and inventory days should stabilize by end Q3 FY15.

- The mgmt said that presently the fall in copper prices may affect negatively due to mark-to-market hit but for long term it is positive as it will bring down the cost.The Company is working with external consultant to improve its supply chain issues like procurement, planning and distribution which will reduce its working capital significantly.The mgmt said that the consumer sentiments are still low and construction activity has not picked up as expected, which has impacted its growth. However mgmt expects both to pick up.The mgmt retained its guidance of 20% revenue growth and EBITDA margin of 8.5-9% for the full year.

Product wise sales break up is as under: -

| Contribution of major products to Top line | |||

| Products | Q2FY2015 Net sales in Rs crore | YoY Var % | Contribution % to sales |

| Stabilizer | 67.9 | 25.1% | 15.7% |

| Standalone UPS | 8.1 | -26.4% | 1.9% |

| Digital UPS | 45.5 | 134.4% | 10.5% |

| Pumps | 40.1 | 18.6% | 9.3% |

| House wiring cable | 140.2 | 19.6% | 32.5% |

| LT Cables | 16.1 | -18.7% | 3.7% |

| Electric water heater | 60.4 | 43.1% | 14.0% |

| Fans | 21 | 36.6% | 4.9% |

| Solar water heater | 12 | 42.3% | 2.8% |

| Others | 20.1 | 59.1% | 4.7% |

| Total | 431.3 | ||

Con Call Key highlights by Capital Mkt

- The mgmt said that euphoria which was there after the formation of new government has died down and consumer feels nothing has changed in environment, which has impacted consumer goods industry. Demand is low for the industry due to â 1) rural demands seems to be impacted as cash crop is badly affected; 2) sustained inflation for last 2-3 yrs which has eaten up the saving of consumer; 3) many high ticket item purchase has been deferred as consumer expects fall in product prices or inflation; and 4) fall in construction activities.

- The mgmt said that leaving 1-2 sectors in consumer goods industry space, overall industry has been impacted in Q3.

- Net sales for Q3 FY15 were up by 11% to Rs 389.80 crore while net profit declined by 47% to Rs 9.22 crore. Revenue growth has been subdued on the back of continued weakness in consumer sentiment with footfalls not improving and construction demand yet to pick up. House-wiring cables, was impacted by the significant reduction seen in copper prices this quarter, leading to lower realizations. Stabilizer and Digital UPS sales continued to be strong, up 23% and 30% respectively.

- The non-south market registered a growth of 17% while south market has grown by 8%. The non-South contribution increased to 32% of sales from 30% a year ago

- Gross margins were slightly higher despite the copper inventory write down. However, EBITDA margins were impacted this quarter due to continued spend on advertising and promotions. Further, there were investments in various BTL activities which will help scale up operations going forward.

- Ad expenditure to sales at 4.9% vs 3.6% in Q3 FY14, up 130 Bps. Ad-spend was at Rs 12 crore vs 7 crore in Q3 FY14. The increase in ad-spend was due to launch of new variants of water heaters.For the quarter, there was Rs 5 crore copper inventory write down.

- Karnataka and Kerala forms 47% of pump business sales. Sales of pump were affected as digging bore-well in Karnataka has been made difficult and also competition has increased from 2 unlisted players. In Kerala, due to more than normal rainfall in last 2 yrs, water level has increased which has impacted pump sales. Along with it, fall in construction activities has impacted pump sales. Also rural demand was low.Debtor days at 41, 3 days improvement QoQ. Inventory days at 81, 7 days improvement QoQ.The mgmt said that wire business margin will be impacted over short term due to high price copper inventory.

- The mgmt has tied up with Amazon and Flipkart for ecommerce sales. The sales from these sites are doing sale at runrate of Rs 1 - 2 crore per month. The mgmt feels that this will be big platform in future but at present its very small and more than 95% of its sales comes from brick and mortar stores. In future it may have separate team to look after e-commerce sales.The mgmt feels demand recovery is 6-7 months away.

- The mgmt said that it will suffer at EBIDTA margin due to high cost inventory at short term, but will bounce back at mid term. The mgmt will pass on some of the fall in raw material cost to bottom-line and some will be used on advertisement and promotion. The mgmt EBIDTA margin target is 10% over long run.

- The mgmt retained its guidance of 20% revenue growth and EBITDA margin was scaled down to 8% against earlier guidance of 8.5-9% for the full year. The margin of 8% is possible with cut in other cost and from sale of high margin products.

Product wise sales break up is as under: -

| Contribution of major products to Top line | |||

| Products | Q3FY2015 Net sales in Rs crore | YoY Var % | Contribution % to sales |

|

Stabilizer |

68.4 |

23.3% |

17% |

|

Standalone UPS |

4.3 |

-23.9% |

1% |

|

Digital UPS |

30.5 |

29.7% |

8% |

|

Pumps |

37.3 |

-8.5% |

9% |

|

House wiring cable |

121 |

7.8% |

31% |

|

LT Cables |

12.4 |

-27.4% |

3% |

|

Electric water heater |

70.2 |

20.6% |

18% |

|

Fans |

22.8 |

41.6% |

6% |

|

Solar water heater |

16.1 |

15.4% |

4% |

|

Others |

12.3 |

24.8% |

3% |

|

Total |

395.4 | ||

Conference Call - Courtesy of Capital Market

V Guard Industries

Expects to sustain a top-line growth of 15% in FY16 with margins between 8-8.5%

V Guard Industries held a conference call to discuss the quarter and year ended March 2015 result, which was addressed by Mr. Mithun Chittilappilly , MD of the company.

Key highlights

• The mgmt said that "FY15 turned out to be a mixed bag year. Consumer spending picked up in the first half owing to the formation of a stable, majority government. The sentiment in the second half was impacted on account of largely unchanged ground realities with rural incomes under pressure and construction activity not picking-up.

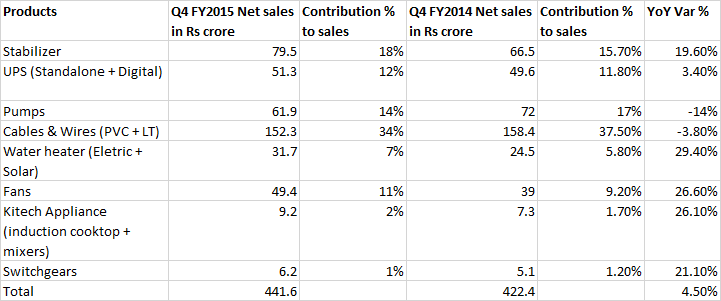

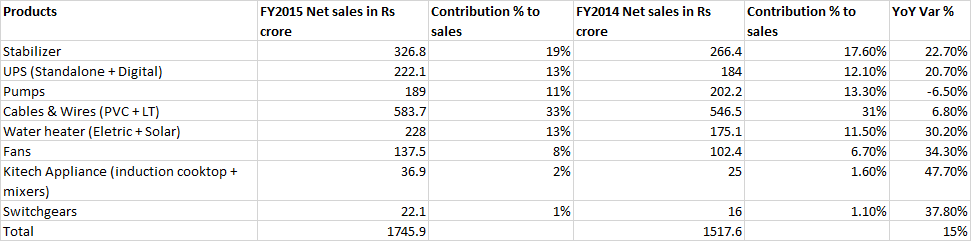

• Net sales for Q4 FY15 were up by 4% to Rs 442 crore while net profit declined by 2% to 20 crore. Wire segment revenues impacted due to lower realizations on account of soft commodity prices. Key markets for pumps segment impacted by local issues

• Ad expenditure to sales at 3.0% vs 3.4% in Q4 FY14

• The company delivered a top-line growth of 15% in FY15 led by strong growth in the water heaters, stabilizers, digital UPS and fans segments. The new kitchen appliance category also received a strong response. Gross margins were higher 60 bps in FY15, despite the significant impact of copper inventory write down, driven by better product mix and lower discounts in the non-South markets. To enhance brand recall in the non-South markets, the company continued to spend aggressively on advertising and promotions which stood at 4% of sales. Non-South markets account for 33% of revenues from 30% a year ago.

• During the year, stabilizer grew by 23% with 20% volume growth. Fan segment has grown by 34%. Induction cooktop was introduced in Tamil Nadu.

• Switchgear grew by 40% in FY15, but it is still small business.

• In stabilizer business, there is some competition from local and branded players in Northern region. Even in such scenario, the company has increased its share in not- so- strong region.

• Capacity utilization in cable business was 80% in FY15. The mgmt is expecting 100% capacity utilization in next 2 years.

• Volume in cable business impacted due to fluctuation in commodity prices. House-wiring cables were impacted by the significant reduction seen in copper prices this quarter, leading to lower realizations.

• Prices for copper were stable from March, till March it was showing downward trend. The mgmt said the copper prices might be not in its favor in first 6 month of FY16, which may result in muted growth for cable and wire business in H1 FY16

• U.P., Rajasthan, West Bengal help to grow in non-south market. Kerala and Maharashtra has shown muted growth. Karnataka is showing signs of recovery.

• The company is selling its fans in South India and West Bengal only. In last 2 years, it has replaced lower margin products in fan with higher margin products. 40% of its fans sales come from premium products.

• The company’s electric water heater sale was Rs 175 crore in FY15 vs Rs 138 crore in FY14.

• In order to improve the quality of customer service and prepare for the next level of growth, the company invested in a franchise-based after-sales service system, upgraded the IT infrastructure and also setup a unified third-party call center. The company expect that these investments will yield benefits going into the next financial year.

• The mgmt said that it will see reduction in employee cost with sales- services person letting off with after-sales service system, upgraded IT infrastructure and also setup a unified third-party call center. For FY16, the mgmt expects employee cost to be around 5% of sales.

• The company’s debt came down by Rs 41 crore to Rs 68 crore. It will future come down in FY16.

• Debtor days stable at 51 days YoY. Inventory days at 74, 8 days improvement YoY.

• The company expects to sustain a top-line growth of 15% in FY16 with better performance in wires and pumps segments and with margins between 8-8.5%.

• For FY16, the mgmt expects around 10% volume growth in cable and wire business at stable copper prices. It expects water heater to grow by 20% and fan by 25%.

• South will pose challenge for growth in FY16.

• The mgmt focus is on increasing distribution in non-south and starting price parity across nation. The mgmt will also focus on market diversification and product diversification. Water heater and fans will be growth driver for the business.

• Capex for FY16 will be around Rs 20-25 crore.

Product wise sales break up is as under: -

Disc: Not invested.

Call was add by Mr Mithun Chittilappilly MD.Key Highlights by Capital Mkt

As per the management, shorter summer, weak housing demand and uncertainty in commodity prices, all affected the overall demand of the company’s products and consumer sentiments in Q2 FY’16.Short summer resulted in lower AC sales, which affected the demand for stabilizers. Uncertain copper prices affected the wiring segment of the company. The Digital UPS demand also got affected as there were hardly any power cuts during the quarter.Gross Margins and Ebidta margins improved to around 28.7% and 8.8% respectively due to lower raw material costs.

Company continues to invest aggressively particularly in Non South Market. Advertisements and Promotions account for about 3.7% of total sales. The company continues to increase its presence in Non-South market.South market which constitute around 67% of total sales, grew by about 3% YoY to Rs 300 crore while Non South market de grew by about 4.7%.

The company was able to reduce its debt by about Rs 91 crore during the quarter. Debt Equity ratio stood at around 0.09 as on Sep’15.

The Electronics segment, which constitutes stabilizers and UPS, which contribute about 27.7% of total sales in Q2 FY’16, de-grew by 1.2% YoY. The de-growth was mainly on account of a 10% fall in sales in UPS to around Rs 48 crore YoY. Electrical which includes pumps, house wiring cable, electric water heater, fans and others, and contribute about 67% of total sales, grew by about 1%, while the new products Swithgears, Kitchen Appliances etc grew by about 4% on a lower base YoY to around Rs 21 crore.The company has launched Water heaters for markets in South and Western India

As per the management some part of the rural economy got affected in Q2, particularly the rural side which is completely dependent on Agriculture. Going forward, rural economy is expected to remain subdued as consumers are postponing their demand. However, festive season, should see some good cheer in H2 FY’16, given a low base of H2 FY’15.

Overall, management revised its net sales growth downward from earlier 15% to around 12% for FY’16. Management expects margins to be around 8-8.5%. As per the management, the festive season, the demand should be good and sentiment has already started in a positive manner.Management does not expect to spend more than Rs 20 crore on capex as most of the capex is done and now only maintenance and warehousing capex is required.

CONFERENCE CALL

V Guard Industries

Expects 5-6% growth in FY16

V Guard Industries held a conference call to discuss the quarter ended December 2015 result.

Key highlights

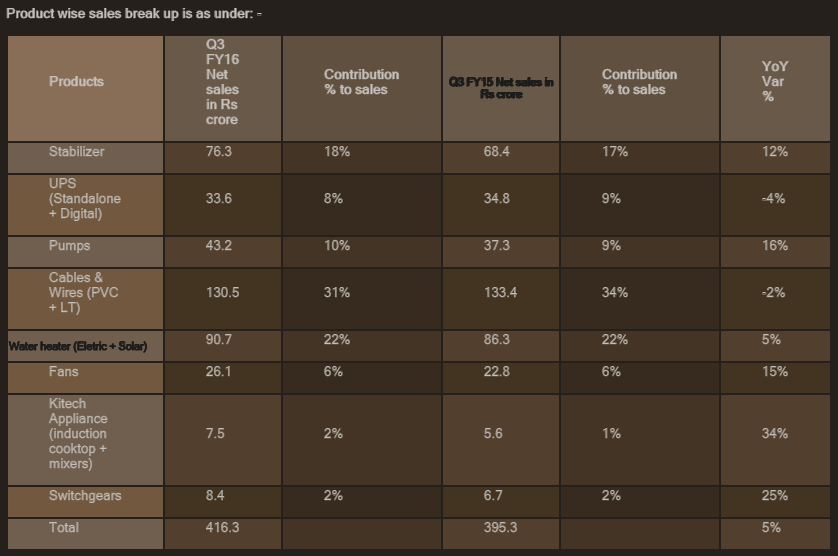

Net sales for Q3 FY16 were up by 5% to Rs 416 crore while net profit inclined by 133% to Rs 21 crore.

Q3 top line growth has been impacted on account of the falling realizations in largest segment, cables and wires, which is linked to the fluctuations in international copper prices. However, volume growth in the segment continued to be healthy at 12%.

Switchgears and kitchen appliances are receiving a good response and seeing healthy growth. The quarter also witnessed a turnaround in the pumps segment. Stabilizer and fans segments continue to track well

Inverter and battery & cable and wires impacted Q3 top-line. The growth was 10 – 11% at top-line excluding these 2 categories.

Gross margins have improved by 220 bps QoQ and 450 bps YoY. Gross margin expanded due to pricing disciple. Only wire and cable reduced prices. But most of the other products are not under pressure to reduce prices.

ASP was 4.5% for 9M .

Gross margin expansion in Q3 is across products categories. Fall in crude price and metal price is good news. The company has not passed all the benefit to customers except for cable and wire business where it has to pass on. Inverter and battery has de-grown in Q3 which are low margin product this helping gross margin

The mgmt said that its margin has improved. But sale is not picking up, lot of overhead cost does not got absorb, thus impacting margin.

Tamil Nadu growing at 15-20%. Apart from Kerala, all 3 states in South India doing well.

Water heater is not performing mainly due to late onset of winter.

Cable and wires 90% of sales is domestic cable. The company is growing in new markets and in some south market where there is activities in construction industry.

The company is seeing food growth in consumer durable products.

Inverter impacted due to not much power cut in southern market this year. There was also product refreshment which is sold in northern market. But product had some problem which resulted in recall, which impacted the sales. But now the product has been corrected.

In inverter and battery, competitors are aggressive; try to cut price and increase their market share. Most of companies are trying to pre-pone their sales, due to expected long summer where power cuts will happen, helping them.

Pump growth seen on low base. Also market has rebounded, which is showing positive sign. The company going forward will focus on larger pumps which are used in apartment for water shortage, bore well, agriculture etc.

Sales from south grew by 8% to Rs 291 crore. Non south was flat at Rs 125 crore. South- Non-south sales ratio was 70:30 in Q3.

The company gets Rs 500- 600 non south business is now. Expects to reach Rs 1000 crore revenue from non south. The company would like to have 40 – 50% revenue from non south markets in coming yrs.

The company is selling only 5 products in non-south:- Stabilizer, wires, water heater, pumps and inverter. It had breakeven at PBT level there. The company was able to reduce price gap with competitor from 10% earlier to 3-4%.

Non south – EBIDTA margin 4% for 9M.

Rs 1.8 crore provided for bonus provision for last 2 yrs in Q3.

Inventory days 7 – 8 days and Debtor days 5 – 8 more in non-south market. Now inventory days coming down.

Lot of WC improvement happens due to improvement in inventory which helps cash flow.

Kitchen business is Rs 45- 50 crore now. Once it hit Rs 100 crore, the company will think of expanding it all over India.

The mgmt expects the new facility in Sikkim for stabilizers to commence operations on a full state basis in 24 months. Once operational, it has a potential of manufacturing goods worth Rs 100 crore apart from benefits through income tax and excise duty exemptions. The exemption is for 10 years and the company estimates tax benefits of Rs 10 crore per annum for initial few years

The company has not seen big improvement in demand after festival season. February is expected to see onset of summer, and as such, the mgmt expects its sales picking up in March.

The mgmt expects 5% - 6% growth in top-line in FY16

The mgmt don’t expect future decline in copper prices. Expect stable level of metal prices and which is expected to rise in coming months as copper companies are cutting down production of copper. As such, trader will start building up low cost inventory which will help revenue growth in FY17. For next year, the company expects strong business in cable and wires due to low base. Stable commodity prices for now

The mgmt expects a long and hot summer this year. Products like stabilizer, inverter and fan are expected to do better.

The mgmt expects 15% growth in FY17.

Gross debt is around Rs 24 crore

CONFERENCE CALL - from Capital Markets

Expects around 15% growth in net sales with Ebidta margins of over 10% in FY’17

The company held its conference call on 5th May 2016 and was addressed by Mr Mithun Chittilappilly MD

Key Highlights

-

Revenues grew by around 16% in Mar’16 quarter on YoY basis. During the Mar’16 quarter, there was a strong growth in stabilizers and fans due to early summer. Excluding wires and cables, revenue growth was around 24% YoY in Mar’16 quarter. Ebidta margins stood at 12.8% during the quarter, largely due to higher contribution from these high margin products.

-

Fans grew by around 46% YoY in Mar’16 quarter due to early summer. AC stabilizer growth was highest in FY’16 as compared to FY’15 and it grew by around 65% in FY’16. Summer picked up only in May’15 last time as compared to early Feb’16 this time. Submersible pump sets also show strong growth due to lower water pressure and people have to dig further for water.

-

The company was able to reduce the discounts in Non-South markets in FY’16, even though it was able to get the benefit of lower raw material prices. Thus Ebidta margin stood at around 9.9% for FY’16, up by 200 bps largely due to better pricing, lower discounts, higher value added product mix and newer products.

-

Geographically, Southern market accounted for around 67% of total sales and grew by around 7.2% in FY’16 while Non-Southern market which accounted for around 33% of total sales grew by around 5.5% in FY’16.

-

During FY’16, about Rs 80 crore was spent on advertisements and branding which accounted for around 4.3% of sales. Management expects ad spend to remain around this level going forward.

-

The Electronics segment, which constitutes stabilizers and UPS, which contribute about 19.8% of total sales in FY’16, grew by around 13%. Electrical which includes pumps, house wiring cable, electric water heater, fans and others, and contribute about 66.1% of total sales, grew by about 8%, while the new products Swithgears, Kitchen Appliances (induction cook tops and mixers) etc grew by about 17% on a lower base YoY to around Rs 69 crore.

-

The company is now third largest player in electric water heaters, second largest in water heaters including solar and the largest national player in solar water heaters. The company has launched new range of stabilizers for inverter ACs which are extremely well-received in the market. The company has now around 7% market share in South India for fans. The company is also a top-5 player in branded house wiring cables and single phase pumps.

-

Debt equity ratio stood at 0.02 as on Mar’16.

-

Going forward, the company expects to increase retailers and increase the revenue per distributor as there is plenty of scope for expansion on existing investment base. Further management expects better pricing in Non-South market to improve margins further.

-

Overall management expects around 15% growth in net sales in FY’17 with Ebidta margins of over 10%.

-

FY’17 the focus will continue to remain to create a nationwide presence and increase the contribution from non South market.

I have been tracking it since long and to me its a great company.The only issue is it has always been overvalued in terms of price (P/E 45 plus and book value of 13) and hence so far only able to get a small chunk of it at an attractive price.The management is transparent - positive for investor considering the dividends and bonus it is paying the only question i had was sustaining growth but seeing the recent move to other products and acquisitions looks like they can grow at same pace for few more years atleast. The debt stands at just 10 crore with a market cap of around 7000 crore plus. I am looking for more indepth details as there are no post after may 2016. if someone can see point out if there are any hurdles for this company.ALso any details on cash flow and Long term assets would be great.Thanks

Not to forget the commodity prices

V-Gurad results are out.

Summary

Annual Revenue - 215062 L (15.5% YoY)

Annual Net profit for FY 17 - 15180 L (36% UP YoY)

Q on Q

Revenue - 62647.10 L (21.55% increase)

Net profit - 4185.78 (0.2% Lower)

Acquisition: Decided to acquire GUTS Electromech Ltd.

As per filing The Company is having its registered office at Hyderabad and is engaged in manufacturing and selling of switch gears, circuit breakers, relays, current transformers and similar electromechanical products. The Company has its plant at Hyderabad and Haridwar and has achieved a turnover of Rs. 29.93 crores during the Financial Year 2015-16.

Highlights

• Net Revenue from operations for the Financial Year ended 2016-17 was Rs.2,150.62

crores; an increase of 15.5% over previous financial year 2015-16 (Rs.l,862.28 crares).

• Profit After Tax for the Financial year 2016-17 was Rs.151.80 crores, an increase of36%

over the previous financial year (Rs.l1 1.68 crores)

• Net Revenue from operations for the Fourth Quarter, ending March 31, 2016-17 fiscal,

was Rs. 623.26 crores; an increase of 21 % over corresponding period of last quarter

(Rs.513.30 crores)

• Profit After Tax for the Quarter, ending March 31, 2016-17 fiscal, was Rs. 41.86 crores,

at the same level when compared with the Profit After Tax of RsA1.97 crores achieved

during the corresponding quarter of previous financial year.

• Recommends dividend of 70% on equity which is Rs.0.70 per share.

Key developments

• Second phase of expansion of House Wiring Cable plant at Chavadi, Coimbatore will

commence commercial production in May, 2017. Capacity will get increased to 8.7lakhs

coils per month. The project was completed at a cost ofRs.12 crores.

For details refer Filing to exchanges: http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/34e88806-c13c-4ffa-bdb8-fa7c22ce75fc.pdf

Views invited future growth prospects especially changes to due to capacity expansion and acquisition

Disc: Tracking.

V Guard Industries - conference call highlights (Source:capital market)

- The revenue for the quarter grew by 15%. Adjusted for GST related price changes, revenue growth for the quarter stood at 21% YoY.

- Broad-based growth across all product categories led by kitchen appliances, stabilizers and Digital UPS.

- Partial recovery seen of the sales lost due to GST in Q1. Sales expected to fully recover over the upcoming quarters.

- PAT grew by 25% to Rs 46 crore

- Commodity price increases were passed on quickly in the market leading to a favorable impact on margin. EBITDA margins expand 100 bps YoY to 12.3%.Favorable product mix and better fix cost absorption help margin improvement

- The company has Rs107 crore of net cash.

- Mgmt said that it is yet to see full restocking. It also had product expansion, which is seasonal in nature and its restocking will start from October.

- Working Capital constraint for wholesale resulting in destocking. If demand raised, these wholesales will run out of inventory, as a result, they will have to start restocking.

- Non south gross margin was at 25% and south of 29% in Q2 FY18 vs Non south of 24% vs south 26% in Q2 FY17.

- South sales were at Rs 718 crore and non south at Rs 410 crore in H1.

- Kitchen Appliances “Mixer grinder” led the segment growth. In kitchen appliance, the company’s strategy to extend product portfolio, which are much different than the present market products for growth

- Durable trade has come back after GST. But electrical trade continue to disturb, also construction activities is standstill which is effecting electrical business. Consumer demand largely remains unaffected after GST. Television sales were good, as result stabilizer sales were good. The mgmt expects electrical trade to come back to normal soon, but has more challenges for them.

- The company has seen no impact in change in business unorganized players to organized due to GST

- Working Capital improvement has happen due to tight control inventory and fine tuning activities towards sales. GST has not helped Working Capital improvement, while it has slight impacted Working Capital.

- 24% like to like stabilizer growth for Q2.

- Expects by Q4 thing to get back to normal.

- Hoping rural demand to be better this year due to good rains. Expects little extra growth to come from non south region, which will help growth in H2

- Cable business saw 3.5% volume growth and 11.8% value growth in Q2.

- In H1, cable volume growth was flat while value growth was 10%.

- Re-stocking is slow in non south market vs south market. The company has regain Rs 20-25 crore lost business of Q1 but balance Rs20-25 crore has to regain.

- The potential market size of kitchen appliances segment is pegged at Rs 22000 crore and management is targeting at least 10% revenue contribution from this segment

- The Sikkim facility may see some increase in employee cost and COGS may be impacted temporarily. Also, the operations cost may be high due to higher transportation cost.

- Project “Udaan” - phase 1 focus on Supply chain efficiency, resulted in reduced inventory, strengthened cash flow and improved efficiency. Phase 2 focus on sourcing more like Centralized procurement and that will be online, new product development and need to place process for better quality.

- Warranty cost is now 1-1.5% of sale. Hope to bring it down future. In last 2-3 yrs, warranty cost has not gone up.

- 1.5% decline in cable business due to discontinuing of LT cables in FY18. Due to low margin and various processes involved in getting business, the company has shut down this busienss.

- 3-5% price growth in kitchen appliance for Q2. 26% and 15% volume growth in induction cooktop and mixer for Q2.

- Stabilisers sales value did not drop drastically as they are still in the 18% tax bracket

- Price rise of 3-5%, planned in April, was effected in June due to resistance from dealers and competitors not increasing prices. A second round of price hikes has been planned in Q3FY18.

- Pricing gap between organized and unorganized segments was in the 20-25% range earlier. However, unorganized dealers have hiked prices now, narrowing the price differential to the 5-6% range

- Management expects 15% comparable revenue growth and 10-12% reported growth for FY18, with margin of 10.0-10.5%.

- Management envisages sales of Rs 100 crore in kitchen appliances in South market alone.

Sharp rise in commodity price (especially Copper) could hurt electrical / cable manufacturing companies. Sharp rise in raw material and lack of strong demand (not much growth in actual realty sector) could be hard impact on bottom line of these companies. Please note that past few quarters such companies’ PAT growth better than Sales due to very low commodity price.

Just commenting. Have never analysed the company.

It is trading at 65x earnings. How much more of a multiple do you want. 100? Mid cap valuations are through the roof. Someone will be left holding the bag. See Porinju email.

Annual Report - FY2017-2018

[https://www.vguard.in/uploads/investor_relations/VG-Annual-Report-2017-18.pdf]

Receivables increased 43% to 449.27 Cr and 5% of the total receivables has been impaired !

Q2 Results

Investor Presentation

Hello, Stabilizer is ~ 18% of the Company’s revenues.

Few months ago I was visiting Shops for purchasing Air Conditioner. My main criteria was energy saving as the AC was meant for regular use.

I was shown many models of Inverter AC by the

Sellers which had some sort of a built in Compressor. As per the shopkeepers there is no need to purchase a separate voltage stabilizer if this is there. I checked it online and found same info on companies websites - https://www.samsung.com/in/support/home-appliances/is-voltage-stabilizer-required-for-an-ac/

Additionally I realised that in developed countries like US, people don’t use voltage stabilizers since there is no major voltage fluctuations.

As similar power transmission technologies get implemented in India, would the demand for Stabilizers keep growing at this rate ?

P.S. - Stabilizers Revenue in H1 FY 19 has de grown by -5% compared to H1 FY 18. In FY 18 it grew only by 3.5% compared on FY 17.