As per annual reports after buy back of almost 20 outstanding shares. They have still 800+ cr. Investment and 197+ cr cash and liquid cash.so total comes around 1000 cr. And mkt comes 1220 cr . so 3 API plants + 3 formulation plant + 1 lab in goa with 300 + scientists are available in just 220 cr.

One red flag is there they loss one suit in European cort in which if they loss then liability to pay comes arou 108 cr.

If we assume they lost then still good bargains are there.

Please advise seniors

One thing that needs to be dived should be its subsidiaries. 3 of its subsidiaries are in losses. Also, they have impaired their investments in Unichem Brasil completely this year. Unichem USA seems to be profitable on thin margins.

Also for FY 17-18 cash balance was 673.61 crores. It is INR 191.03 FY18-19. Probably they bought a stake in 2 companies in Hyderabad Optimus Drug P Ltd and Optimax Lab pvt Ltd which have USFDA approvals with that money. It seems the company is developing an inorganic route for growth.

Also, the % increase in salary of MD is 188% whereas the median increase is just 11.5%

In all the AR, the amount invested in Brazil facility is impaired every year.

What is the total amount invested in this subsidiary?

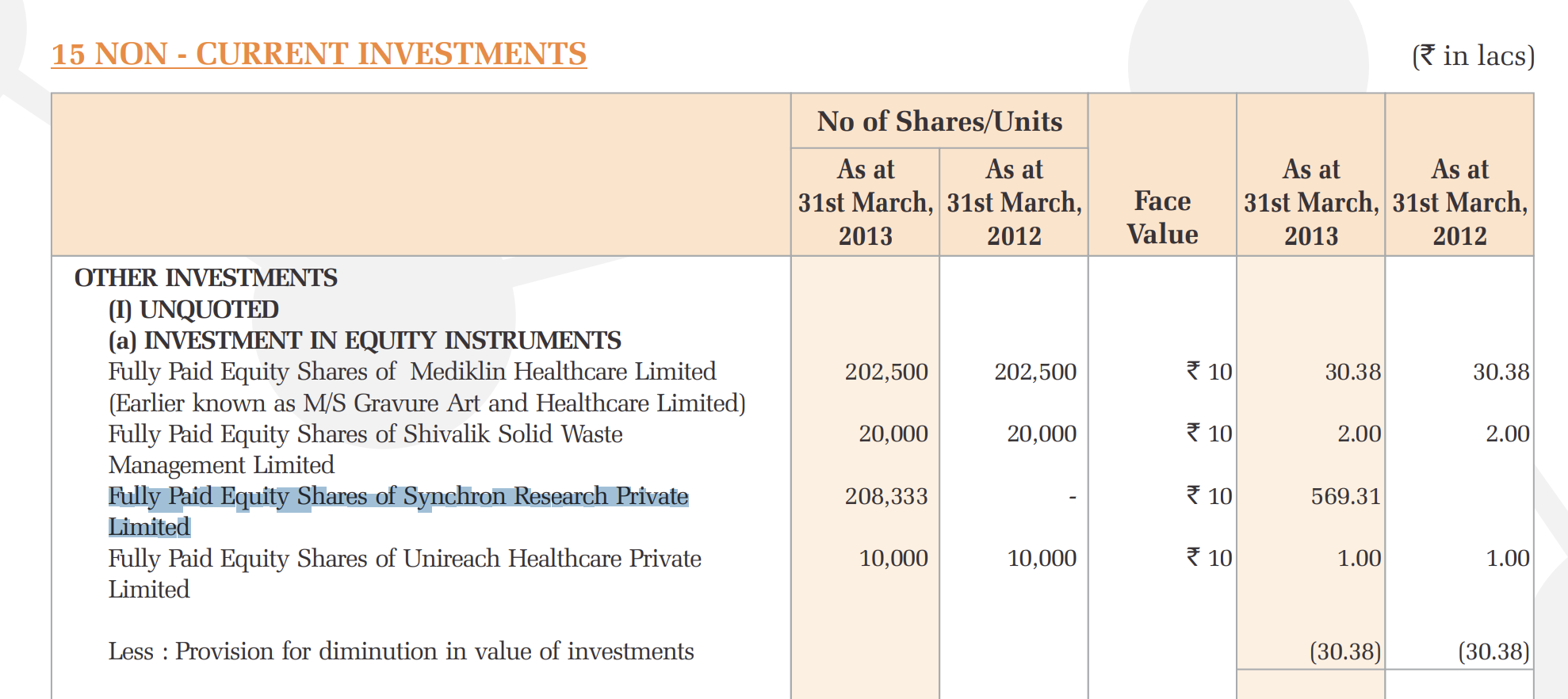

From AR 2019 “The Company has reviewed its investments in wholly owned subsidiaries. In respect of its investment in Unichem Farmaceutica Do Brasil Ltda ,Brazil , Impairment loss recognised for this investment for the year 302.83 Lakhs (P.Y.511.71 Lakhs). This has resulted in the aggregate Impairment loss to 7,086.72 Lakhs (P.Y.6,783.89 Lakhs) on a total investment of `7,086.72 Lakhs”

1 Like

The company has following

Pro

- More than 1000 + cr of cash/cash equ.

- Global API business

- Integral management.

- No debt

- Conservative accounting policies- expensing all R&D expenses upfront.

Con

- Uncertainty about business in next year or two.

- Not sure when the company will report profit.

- Not sure how management will utilise 1000 cr cash.

Many people (including myself) having not tracked the company for long, will find the company interesting based above key points. However, the market is having a different thought may be because market does not give much value to cash on balance sheet, or may be I am missing something.

@hitesh2710 bhai- You have been in this stock for a long time (not now, but earlier, I think). Do you not see a potential in the company any more? Any views?

unichem labs @147, almost at 5year low

book value - 387 rupees

Does anyone know why the company stopped doing conference calls post the slump sale to Torrent in 2018? Also, the management no longer comes for interviews.

2 Likes

Why Unichem Lab has very low OPM% compared to other pharma companies, still Unichem is just 2500cr Marcket cap, and it has Reserve of almost 2500cr, seems strange (Market cap is just valued reserve of the company)

If you go through the entire thread, you will see Unichem sold of its domestic business, somewhere around 2017-18 period, post that they are only focussed on international business. The international business has been growing since the change in trajectory of the business, but they were in the initial days, were making losses. Only recently the numbers have turned positive. The margins are reflection of that. Check the last few quarters results, you will see the margins were negative.

Disc. Invested.

4 Likes

Unichem Laboratories announced that it has received Tentative Approval for ANDA of Aripiprazole Tablets, USP, 2 mg, 5 mg, 10 mg, 15 mg, 20 mg and 30 mg from the United States Food and Drug Administration (USFDA) for a generic version of ABILIFY® (Aripiprazole Tablets) 2 mg, 5 mg, 10 mg, 15 mg, 20 mg and 30 mg of Otsuka Pharmaceutical Co Ltd.

Anyone has come across this legal case between Unichem and another party in the UK Courts. Am aware of the EU case wrt to Niche, their European subsidiary, but have not come across this in their AR.

As per this video, Aditya Khemka has a sizeable position in Unichem laboratories.

Unichem has been focusing on US business and growing its presence by filing a number of ANDA in the US. Also, after selling their domestic formulation business, they have zero presence in the domestic market.

Mr Khemka is very clear that the US formulation business, which targets the generic market, is a commodity business. If I look at Unichems Annual reports, it talks very briefly about biologic and but most of their commentary is about US formulation business.

So I am curious to understand why he is investing in Unichem when it is focusing on the US formulation business? Or Am I missing something?

I know that Unichem is as secretive as it can be when it comes to disclosure and investor communication, but is Mr Khmeha knows more about the business than what is general perspective about the company?

It would be great if someone can post any link he /she may have referred to in his(Mr Khemka) talk/investor communication.

1 Like

Here are my notes from their AR21:

- Filed 5 ANDAs (including 1 Para IV), 2 DMFs in US, and 1 CEP

- Received 9 ANDA approvals and launched 8 products in USA and 2 in Brazil

- Revenues grew by 12% to 1235.14 cr. and PAT turned positive at 34.32 cr.

- US contributes 57% of revenues

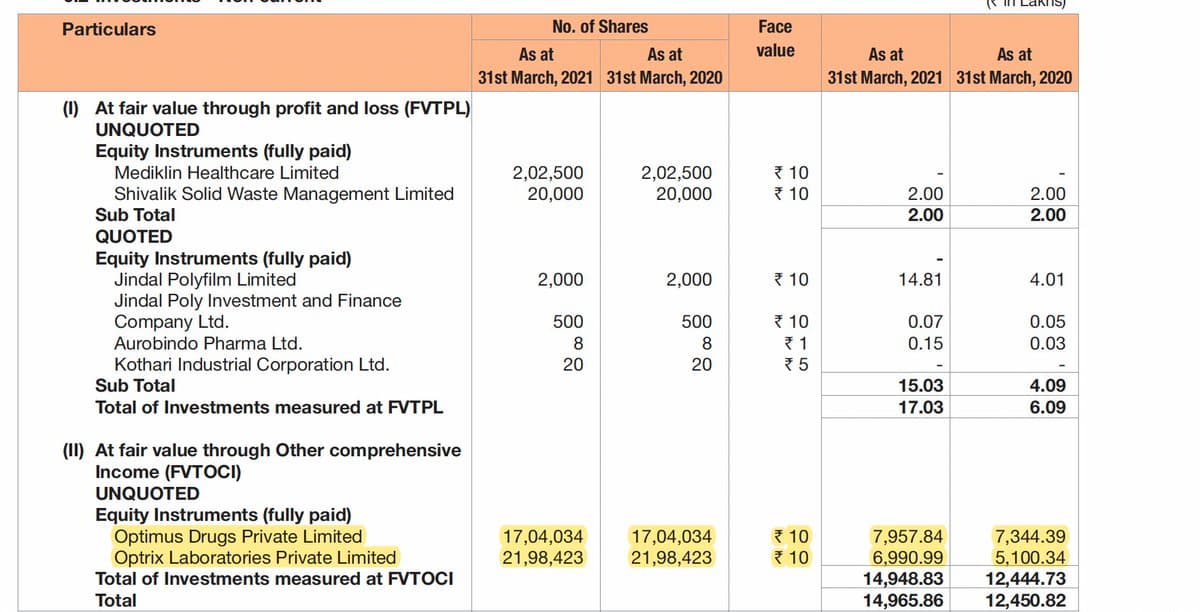

- API: Strategic investments in two entities, Optimus Drugs Private Limited and Optrix Laboratories Private Limited, both engaged in the business of APIs and intermediates. Management of these Companies had decided to merge Optrix Laboratories with Optimus Drugs to combine the activities and operations in a single Company

- Underwent successful EU audit of Baddi and the Ukraine audit of Ghaziabad plant

- R&D:

o Centre of Excellence in Goa is served by 300 scientists including 30 PhDs

o Formulations R&D has facilities to undertake formulation development of tablets, capsules, liquid orals, creams, ointments and, a separate facility for injectable and pre-formulation laboratories to carry out drug-excipient compatibility studies and physical characterisation of API

o Undertakes formulation services on contract research and development projects for several leading global pharmaceutical companies

o Has a Bio-Tech facility engaged in developing novel or biosimilar products using Recombinant DNA platform technology - CAPEX of 334.89 cr.

- Gross margins improved by 4.4% due to better product mix

- Number of employees: 3090 (992 contractual) (Managerial salary increased by 9.07% and other employees by 10.11%_

- Share price: low (121.1), high (360.6), # shareholders: 34’714

- EU fine contingent liability: Euro 13.96mn (120.45 cr.)

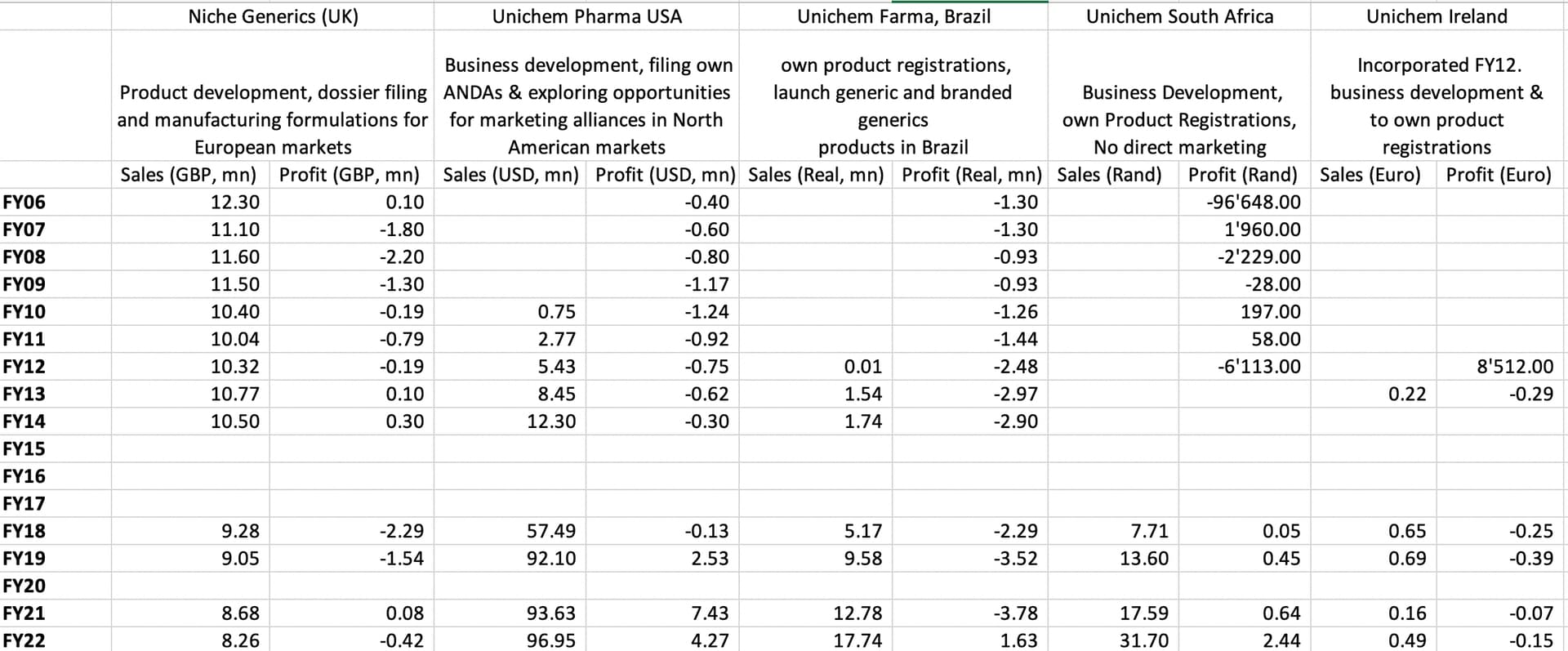

The key monitorable is how US business shapes us, currently US is doing revenues of $93.63 mn and PAT of $7.43 mn. This number was $92.1 mn and $2.53 mn in FY19. So revenues have not grown much but margins have improved significantly. UK (Niche Generics) continues to struggling with revenues going below GBP 9mn and very marginal profits. South Africa operations have scaled up well from 7.7 mn Rand in FY18 to 17.59 mn Rand in FY21 and profits increasing to 0.64 mn Rand.

Disclosure: No investments

4 Likes

The impact of FDA actions on Synchron discussed in the Laurus thread can have significant impact on Unichem due to Unichem’s equity investment in Synchron (5.69 cr. made in FY13)

https://www.bseindia.com/bseplus/AnnualReport/506690/5066900313.pdf#page=93

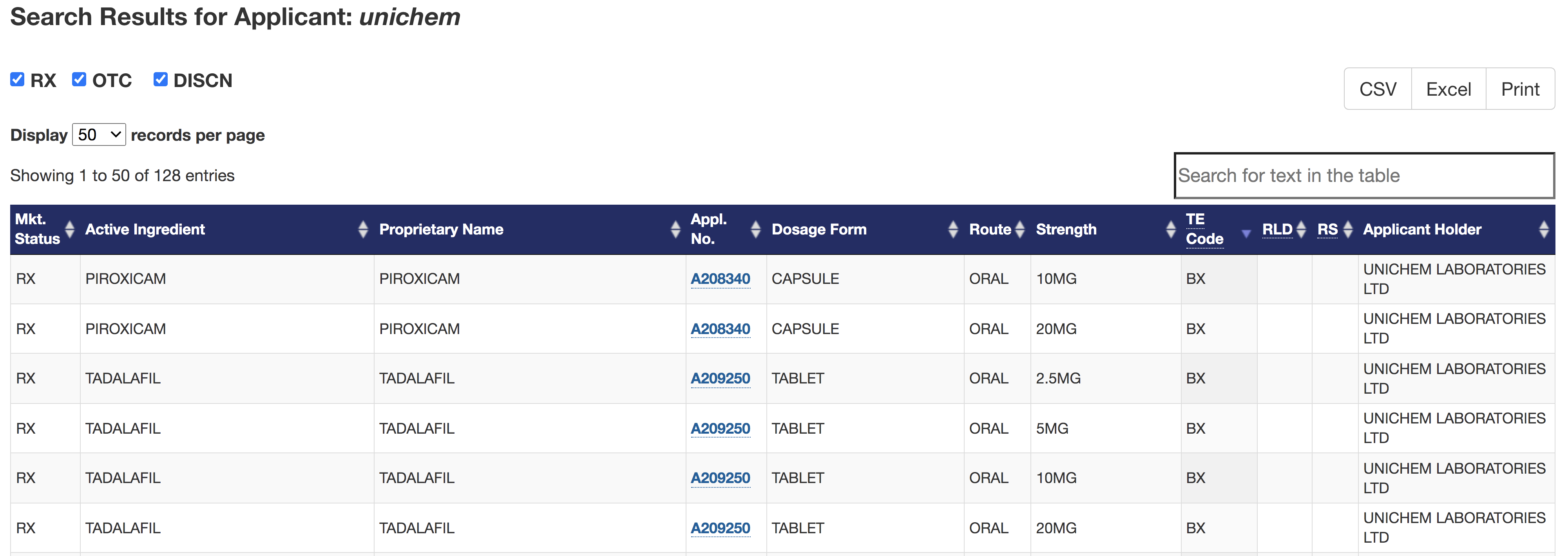

Synchron leases office space from Unichem and is categorized as an associate. Unichem also uses their bioequivalence services for their own ANDA filings, two of these filings have now been categorized as “BX” status, meaning they cannot be interchanged with innovator RLD at pharmacy level.

Disclosure: Not invested

8 Likes

Harsh, appreciate the alert. Could you share how manage to track it down? Have set up some system of alert or do you manually keep track of the the FDA notifications? I do monitor the FDA site, through through their email alerts, which they email every week or so. Bit this alert was not mentioned their email alerts. Will be very helpful if you can share how track it. Thank you.

Untitled letter sent to Synchron by USFDA. Very detailed, highlights the lapses in their system. Not sure of how many drug applications approved or in the pipeline of Unichem might get affected due to this ruling. Tried to access the website of Synchron research, was not able to. It can be also be useful to understand other clients of Synchron research, who may get affected due to this issue. Any ideas how it could be done?

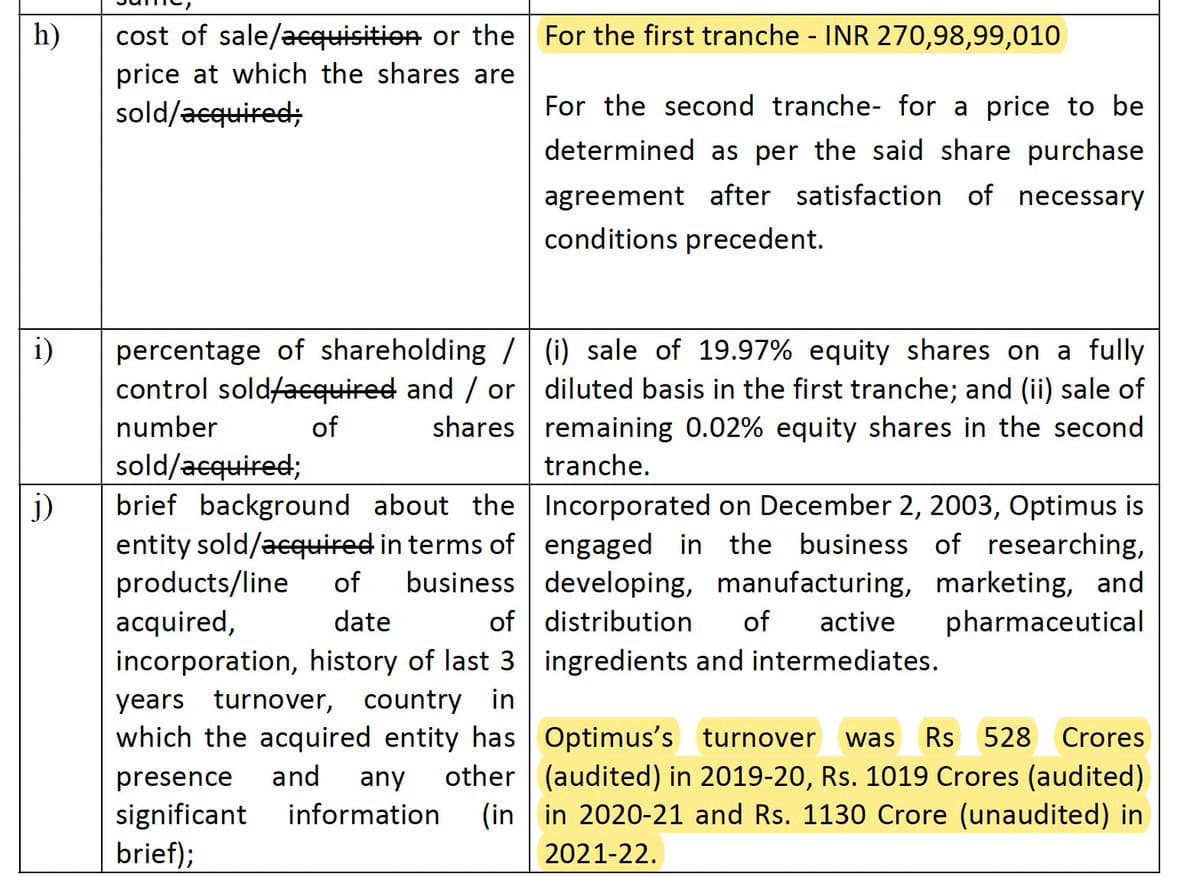

Unichem Lab sells their stake in Optimus Drugs & Optrix Labs for 270 cr., they had cumulatively invested 150 cr. upto FY21. Sales growth for Optimus has been spectacular (from 528 cr. in FY20 to 1130 cr. in FY22). Optically, it looks like a very cheap sale. No idea how company buys/sells their investments.

Disclosure: Not invested

4 Likes

Two key points from Unichem AR

Unichem concluded its major capex-cycle spread over the last 3 years at all its manufacturing facilities i.e. for formulations, APIs and at its R&D centre. This will ensure that we are ready to unfold the market opportunities while maintaining the highest quality standards. Most importantly, this capex was funded entirely from the internal accruals. With most of these facilities commencing operations, we expect an easing of pressure on our operating free cash flow in the coming years. With this newly built capacity and capabilities, we are hopeful that we will continue to deliver value and strengthen our foundation for growth.

We have built new capacities and capabilities, including R&D, Manufacturing and Quality and expanded our product portfolio to deliver long-term, sustainable growth in our generics business. We are hopeful that we will continue to deliver value and strengthen our foundation for growth. With formulations constituting the core of the Company’s business, Unichem is backward integrated to API manufacturing, which will add value to the customer in terms of quality and sustainability going forward. The outlook for the Company remains bright, going by the number of products/filings filed or lined up in coming years.

1 Like

FY22 AR notes:

- Filed 5 ANDAs, 1 DMF in US, and 1 CEP

- Received 5 ANDA approvals and launched 5 products in USA and 2 in Brazil

- Revenues grew by 2.8% to 1270 cr. and PAT remained at 33 cr.

- US contributes 58% of revenues (vs 57% in FY21)

- 3 formulation plants (Ghaziabad, Goa, Baddi) and 3 API plants (Roha, Pithampur, Kolhapur)

- Core strategy is to sell formulations and be backward integrated into APIs

- Strategic investments into Optimus Drugs Private Limited and Optrix Laboratories Private Limited of 120 cr. (in Nov 2018) were sold for 271 cr. + some more money in second tranche giving gains of 76 cr. Carrying value on balance sheet was 226 cr.

- Impaired investment in Synchron (4.87 cr.)

- CAPEX of 127 cr. (vs 335 cr. in FY21), capex cycle over last-3 years is finished and should drive higher operating cashflows

- Gross margins declined by 2% to ~68% due to pricing pressure and product mix change

- Implemented Success Factors Learning Management System (LMS) at four sites which was a significant step towards digitization of training records and processes.

- Number of employees: 3’167 (vs 3’090 in FY21) (888 contractual) (Managerial salary increased by 9.98% and other employees by 10.55%)

- Share price: low (197.5), high (375), # shareholders: 34’539 (vs 34’714 in FY21)

- EU fine: Has not provided for liabilities coming from EU fine on Niche UK (122.67 cr.). Auditor is of the view that this should be provided whereas management thinks it should be provided once court gives unfavorable verdict

- Auditor remuneration: 1.52 cr. (vs 1.33 cr. in FY21)

R&D:

- Spent 118.96 cr.

- Centre of Excellence in Goa is served by 300 scientists including 30 PhDs

- Formulations R&D has facilities to undertake formulation development of tablets, capsules, liquid orals, creams, ointments and, a separate facility for injectable and pre-formulation laboratories to carry out drug-excipient compatibility studies and physical characterisation of API

- Undertakes formulation services on contract research and development projects for several leading global pharmaceutical companies

- Has a Bio-Tech facility engaged in developing novel or biosimilar products using Recombinant DNA platform technology

Longer term financials of subsidiary: US operations have scaled to $100mn, Brazilian and South African operations have also scaled well. However, UK operations continue to be subscale and loss making.

Disclosure: Not invested

6 Likes