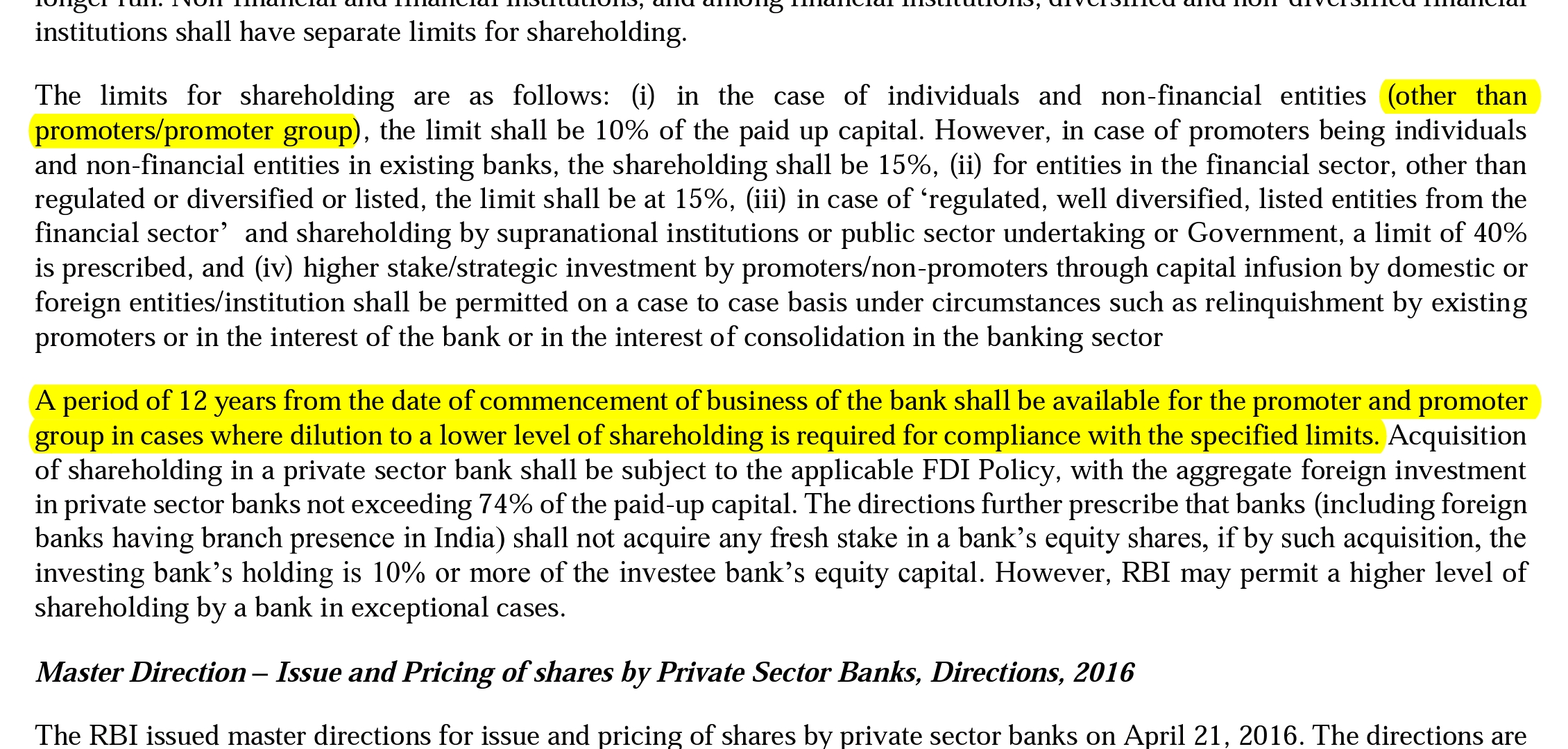

Hi,

@Akash_Padhiyar, that is not how holding company discount is calculated. You would be correct only in special situations where the number of shares outstanding of similar face value, would be equal for both the holding company and the underlying business.

In case of Ujjivan as per FY19 AR, on a consolidated basis, the number of outstanding shares in UFSL as on 31st March 2019 was 121,166,697 shares, PAT was Rs. 150 cr odd and Book Value was 1877 cr odd which gives us a BVPS of 155 odd.

On a standalone basis for UFSL, the shares outstanding are same, PAT was 21.5 cr which is mainly from dividend and interest on FD received from USFB, Book Value was 1787 cr odd which gives us a BVPS of 147 odd.

While USFB as per the same document has 1,640,036,800 shares outstanding inclusive of preference shares, PAT was 204 cr odd and Book Value was 1819 cr odd which gives us a BVPS of 11 odd.

Now, based on Mar -19 Book value, UFSL currently trades at P/B of 2 odd. Now given the IPO, there will be around a 10-15% dilution based on listing valuations. I have shared the table in my previous post.

In the same table, you will see the corresponding Market Cap of USFB at different PB multiples, UFSL’s corresponding holding % at different dilution levels and corresponding market cap values for the holding company at the 50-60% holding company discount.

Your assigned value of 400 to the share price of USFB would give it a P/B of 36, and P/E of 321 which even you will agree is absurd and the discrepancy is due to the different number of shares outstanding in both entities.