http://www.idfc.com/investor_relations/shareholder_info-demerger-scheme.htm

1 Like

These two are not only option I guess to do listing and it is possible to list without bringing ipo. For example by scheme of arrangement where sfb can be listed directly and each owner of holding company can be given share in proportionate basis. What difference does ipo bring existing shareholder is also public shareholder. Why they can not be allocated share in new entity in lie of their holding in parent company. Actually bankers brokers and promoters prefer ipo rout because it can help them short charge existing shareholders and they can get good fees etc. However here situation is different as there is no promoters and shareholders is only promoters. RBI guidelines just need listing wether by ipo or scheme of arrangement makes no difference to rule and don’t violate any conditions of banking license etc

2 Likes

There is no mandate for listing with dilution at 40%. RBI mentioned, promoter holdings cannot come below 40%. In new IPO even 10% dilution is fine but listing to be done for SFBs, not the holding cos

RBI mandate is - within next 3 years from listing, promoter holding should come down to 40% as happened for Bandhan…

even if they come with IPO and assume holdco sells 50% stake to new investors, at 2xbook it will get 2k crores which get distributed to holdco shareholders, they get 1600cr(20% DDT) . plus holdco would still own 2k worth of shares of the bank (4k cr mktcap at 2x BV) . ofcourse this is pure speculation,

plus there would stay a high possibility of merger. So the holdco discount would be even less.

2x book is a fairly conservative price to ask. And if theres really an IPO, the holdco shareholders would benefit even more. the downside from here is the business hitting another speedbump. Theres a very near-zero possibility of existing shareholders getting shortchanged.

Remember Bandhan pricing its IPO at an extortionate 6 times book…

3 Likes

To get sfb licenses 3 years back even likes of Bharat financial are also in race however RBI choose ujjivan equitas au and bandhan etc because they find them to be much better in various criteria including corporate governance. It shows happen that due to demotisation and sfb rollout both of them are bit slow to transition which allowed valuation to reach to so reasonable level. Now considering liquidity issues in nbfc sector and npas issues in banking sector both equitas and ujjivan seem to be best placed in terms of balance sheet quality may be next to HDFC bank or Kotak bank only so they can feel the gap in small town and urban areas.

Disagree with some points. Bharat financial is doing very well without a SFB license. Bandhan doesn’t have an SFB license but a bank license. As far as the liquidity crisis is concerned, it doesn’t mean much at present for SFBs as Ujjivan has barely scaled up its CASA deposits to be an effective cushion. It will take a few years for any sort of benefit to accrue from CASA deposits. Being in investment stage, the cost structure of the SFBs will not give EPS gains for shareholders in the short to medium term. SFB license should not be holy grail for NBFC investors because at end of the day, yields and ROE are what matter. Risks, as recent events have shown can come in any form or shape and are not confined to microfinance. No one knows how the NBFC/banking industry will evolve and competitive forces will take shape. There’s a scenario that MFIs continue to grow (due to the specialized form of their lending) and small finance banks struggle to compete for traditional banking channels.

Till this point all nbfcs was doing well and major beneficiary of banking npas and demotisation and adhar card integration etc. However post IL&FS fiasco there is very high likelihood that RBI may come with tough regulations for nbfcs which can make them closer to current banking regulation which in turn can affect their ability to lend 95 percentage of capital and which can reduce their return ratios because they may pose systematic risk. All nbfcs need to adjust their business practices based on those new regulations while for ujjivan and equitas being all ready a bank those regulations changes don’t likely to have much impact. Now current management of both can able to take advantage of those regulations need to be seen.

1 Like

RBI Halts Small Bank Promoters’ Reverse Merger Plans

THE PLAN Equitas and Ujjivan small fin banks wanted a reverse merger of their holding cos with banks

Kolkata:

Promoters of Equitas Small Finance Bank and Ujjivan Small Finance Bank have been exploring a reverse merger of their holding companies with the banks, but last week’s RBI order has put a stop to this possibility.

The central bank said the banks have to be listed within three years, without fail.

“We had requested the regulator to give permission for reverse merger of the holding company with the bank, which would avoid the dilution of shareholders’ value. This would have made the bank listed automatically,” Ujjivan Small Finance Bank managing director Samit Ghosh told ET. Had the RBI allowed the reverse merger, promoter holding in small finance banks would have come down below 40%. This was perhaps the principal reason behind RBI’s insistence on listing their banks separately.

“We were advised to follow the original condition of the licence, which requires the bank to be listed within three years while promoters’ minimum 40% shareholding has to be maintained for initial five years,” Ghosh said. The holding companies can still be reverse merged, but may be only after the bank’s listing and after the lockin period of promoters’ holding. ET learnt that promoters of Equitas and Ujjivan were in talks with RBI on this issue for the past couple of months. The RBI diktat last week ended the dialogue.

In a filing to stock exchanges, Equitas said the company would consider at its next board meetings the steps to get the shares of the small finance bank listed within the prescribed timelines, and a plan to approach the regulator for an approval to merge with the bank at an appropriate time, after the lockin period. Promoters of both banks listed their respective holding companies even before they launched banking. Now, they will have to list their banks separately.

Analysts said that if the banking business is listed separately, the holding company will have no business left and would trade at a discounted price. Interestingly, RBI allowed small finance banks to either be set up under holding companies or as standalone units. Out of eight microfinance-tuned-SFBs, four including ESAF and Vanarasi-based Utkarsh followed the holding company structure.

2. Through this process, Equitas Holdings Limited (EHL) plans to dilute upto 60%of its

holdings in ESFBL in favour of its existing shareholders and to remain a nonoperating

Core Investment Company till such time that it gets regulatory approvals

, to merge with the bank.

Equitas filing to exchanges.

Can someone please explain what does it mean in layman terms?

Thanks!

Suppose you have 100 shares of equitas today and management decides to issue 1 share of SFB for 1 share of holdco then you will get 60 new shares (of SFB) in your demat. While you will hold 40 shares of SFBs indirectly via your 100 shares of holdco. So in an ideal world if suppose the day this happens, equitas (currently listed) share was trading at 100 then the share price will fall to 40 while the 60 new shares will trade at 60 so your total value remains 100. In real world, because of holdco discount, instead of 40 the holdco share might trade at 20. In this case, unless the SFB starts trading at a premium - say 80 - you will lose money. On the other hand if SFB starts trading at much higher premium - say 100 - you can even gain from this split.

7 Likes

Both companies ujjivan and equitas are poised for strong growth in medium term. They have relatively strong balance sheet more important they have strong culture to serve small retail customers at urban and rural area which is not easy to be served by other banks. By the time this new bank listing shall happen there book can rise by 30 percentage which at current valuation is enough to support the stock price even with holding company discount. How many pan India bank is available with market cap of 3000 cr and 2000cr. They are slow to transition to a bank because they are listed while bandhan and au bank got listed after luanched bank so they are able to move fast otherwise equitas and ujjivan has better reputation than au bank atleast.

2 Likes

Personal feel on the recent meltdown in Ujjivan shares on listing of SFB’s is that there are a lot of legal ways to ensure that shareholders of holding company do not suffer on account of what is IMO a pretty arbitrary decision by the RBI. Giving all shareholders a free share of the SFB in same proportion as holding company is an obvious one, but I’m sure there are other ways to restructure this as well. I guess the promoters will have to work out tax efficient ways of doing this on which clarity will emerge in a couple of months.

The holding company has no business other than the SFB, so all stakeholder’s incentives are aligned with getting a good resolution for this which is the most effective indicator that this should happen. Operational shortcomings may be a different issue but don’t see this as a negative long term.

1 Like

Sharing some on-the-ground experience with Ujjivan. I have been talking to their sales executives in getting an FD opened for couple my family members. In this context I happened to be present for their formal inauguration event of a new branch in Bangalore. Below are my observations:

- This new branch is not exactly a net new addition to their branch count. They closed down a smaller and interior located branch and opened this bigger and main road facing branch (right on the main road and next to ICICI bank branch).

- The typical branch staff strength is about 30 people (mostly employees) out of which 10% are into sales helping to build CASA, 10-20% supporting staff and the remaining staff are all on asset side (selling and servicing loans). This was the case for a few branches that I enquired about in Bangalore, but I am not sure if this is a good representation of the overall network of branches.

- The sales staff were mostly freshers and lesser tenured (less than 4 years of overall work experience), and might need a little more grooming. Never the less they were all very committed to their job and one of them had even purchased few Ujjivan shares

- The account opening and FD servicing (if any) were all done at the doorstep as promised. Sales executives use an android tablet that is attached to a hand held printer and biometric device. Overall account opening experience was good.

- The branch inauguration event had a local leader, area police officer and a senior citizen as chief guests. The event reflected religious pluralism with a mulla, a priest and a poojari all performing their respective duties and praying for good luck to the bank, staff and customers.

- Most of the customers invited for the event were women availing loans to earn an income for the family and spoke well of the bank.

- Casual conversation with the sales staff indicated good response to the FD schemes from senior citizens. Some of them moving their deposits from other private banks.

20 Likes

I am quite disappointed by the approach taken by Ujjivan Financial Services Limited (USFL) board. I have following points to make

-

What is the meaning of “best interest of all stakeholders”? Who are the stakeholders here? I could only think of two stakeholders - Shareholders of UFSL and Regulator. These words are making me very uncomfortable. Looks like in addition to Regulator and Shareholders their is some other force at work here jeopardizing the interest of Shareholders, imposing some kind of cost on them for their naivety in trusting the Board/Management particularly the Founder.

-

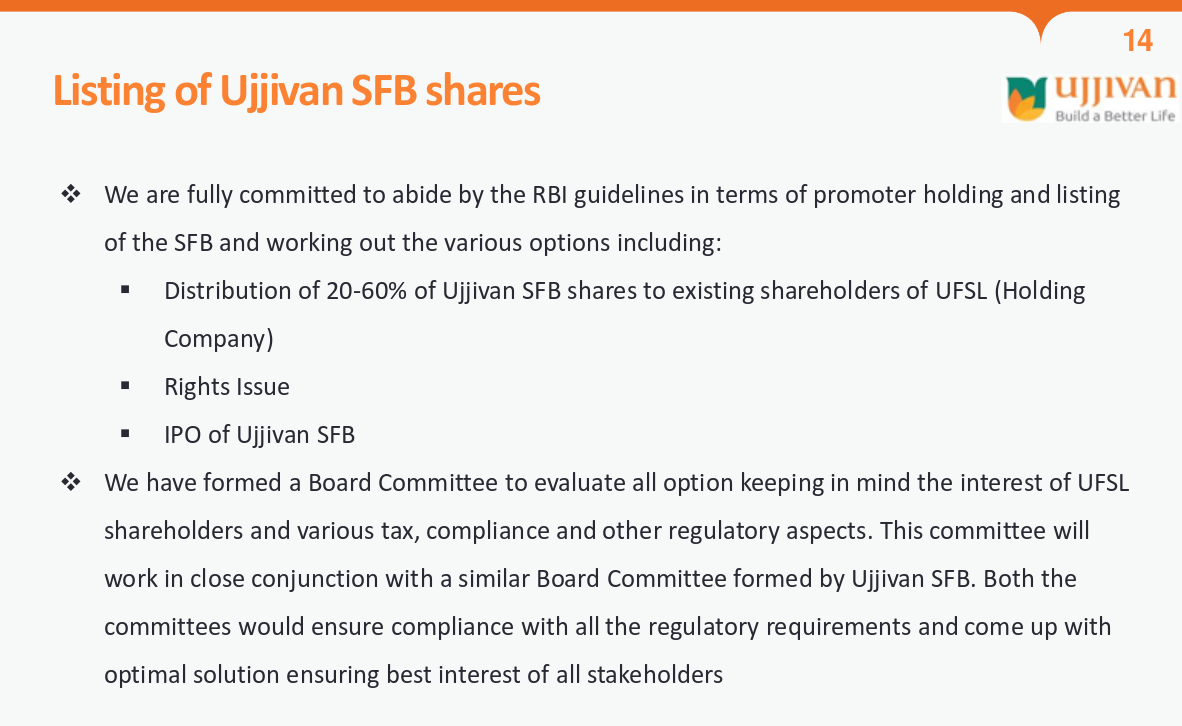

“Distribution of 20-60% of Ujjivan SFB shares to existing shareholders of UFSL” - I am not comfortable with owing anything less than 100% because that is what I thought I own. But since Regulator does not allow I can own 60% of SFB and 40% indirectly through USFL again some force at play is trying to reduce 60% to 20%.

-

“Rights Issue & IPO of Ujjivan SFB” How is the interest of shareholders of UFSL rightful owner of Ujjivan SFB is protected in this?

-

I am also quite disappointed that the a decision as not been made till date whereas Equitas clarified that they will give 60% of their shareholding to existing shareholders of holding company.

-

I am very disappointed in the Founder - Mr. Samit Ghosh of the company who never cared to bring this issue to shareholders of UFSL.

Disclosure - Invested.

2 Likes

As per the Q2 presentation report, the Portfolio At Risk (PAR) in absolute terms has increased from Rs.256Cr to Rs.267Cr. Isn’t this a sign of GNPA increasing in the coming quarter at least in absolute terms?

Bharat Financials has done a fair good job at bringing down the GNPA to sub 1% quickly. I still see a few more quarters before Ujjivan can return to its glory days where GNPA was less than 0.5%. I am assuming MSME loans and Individual micro finance loans are playing a spoilsport.

Please correct me if I am wrong in any of the above assumptions.

Also, I like the fact that Ujjivan has a conservative stance in terms of their Provision Coverage Ratio. However, the ratio has fallen from 88% to 85% Q-o-Q. Could someone please help me understand whether it’s completely up to the discretion of the management to decide what should be the PCR?

Appreciate your answers, thanks.

There could be two reasons for this.

- Equitas has less than one year to list while Ujjivan has another year (or two) more than Equitas to make that decision.

- Mr. Samit Ghosh is retiring and the focus is on finding a new CEO. Once the CEO issue is sorted, may be listing issue will come up.

Having said that, I hope what Equitas has done will also set a precedence and put some pressure on Ujjivan management to not do much worse than what Equitas is doing for existing shareholders.

The article seems to indicate that the management is doing 60% distribution because as per RBI norms 40% has to be with the promoter.

I am not sure if that statement should be taken at face value but it is it a possible reason for the 60% number. Given that holding company does not have any business other than the SFB ideally promoter and shareholder should be aligned, but it can be a clause that has potential for misuse . But given RBI monitoring, promoter enriching himself at cost of minority shareholders will not be as easy as for someone like Meghmani. Waiting for concall to throw more clarity.

2 Likes

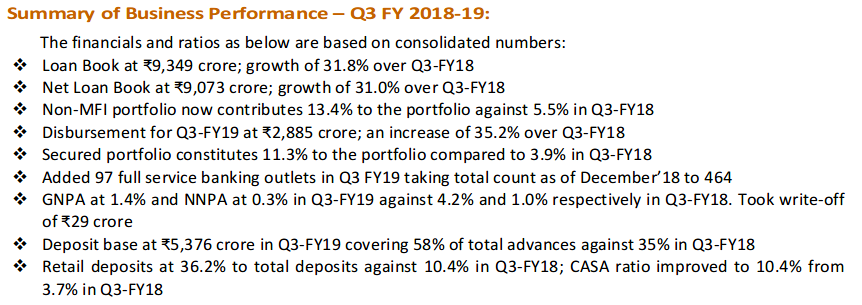

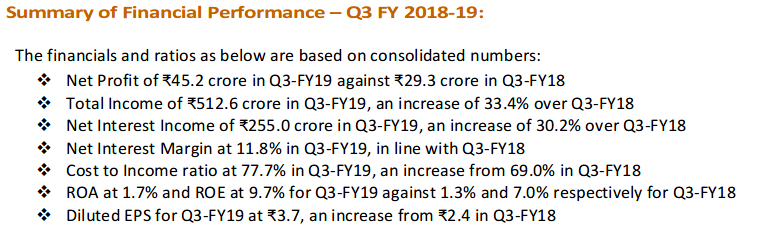

Ujjivan Q3 results.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0a8b0316-5451-493c-ad4b-c933790b76b0.pdf

Note: I can see only standalone numbers reported. Consolidated numbers only in press release and Presentation.

Summary from press release: