There is a conference call planned at 4:00 PM today.

1 Like

did anyone join? unable to join… saying wait for an operator

Luckily got in even though late…

Some take aways…

- Promoters sold the stake to bid for the upcoming tenders…

- There is no plan for more sale right now…

- Promoters selling stake was because they didn’t wanted to raise debt from outside … (they want to remain debt free as far as possible… and i am wondering how power company can ever remain debt free… if they succeed it would be an example …

)

) - In future Warrants/Preference or QIP can be considered.

)

)What i felt good is they are reasonably confident on future of the company…projects etc…

They also clarified there is no risk on REC inventory front…no write offs would be needed

2 Likes

Couple more points

- He did mention that REC’s have a 2yr validity period beyond which they may need to written off. Off the current inventory there is no risk.

- Also he mentioned that the cost of REC’s are on their way down from April 1st

- The 60 cr obtained from stake sale would be put back into the company as loans and advances at very soft interest rates

- This 60 cr would be deployed to get orders to the tune of 250 MW. He talked about a 20% stake holding in bigger projects, which has become a sort of norm for bigger projects. They could sell the minority stake back to the majority

- This 250MW could result in 1000cr revenue for the company over the years.

- They tried to get capital through QIP, but since it was getting delayed and they missed out on couple of projects because of the delay. Hence they went for the stake sale to raise the money

- They are done with their requirements to raise capital. No further reduction in Promoter stake in the immediate future

1 Like

I joined the call too. And on the face of it, Anurag looked genuine. Very

difficult to say it is a fraudulent move to sell stake in open market after

hearing him. He assured that promoters will get a very soft ( low )

interest when they loan this money to company. He also said that they will

use this money to get a minority stake for Ujaas in some small solar park

projects ( 5 - 50 MW) with the condition to the majority shareholder that

the EPC should come to Ujaas company without competitive bidding. And Ujaas

will exit the minority shareholding in 2 - 3 yrs at a profit. .The whole

idea of this model is that Ujaas will continue to remain asset light in

future too. He also said that the promoters cannot loan the money to Ujaas

at zero interest as it will be considered as an income to Ujaas…

It is a hard call - whether they are honest are not…But my gut feel at

this time still goes slightly more in favor that they are still

honest…Time can only tell the truth…

Disc: Still invested…Not sold the holdings…views are biased to that

extent…

2 Likes

This will help improving margins

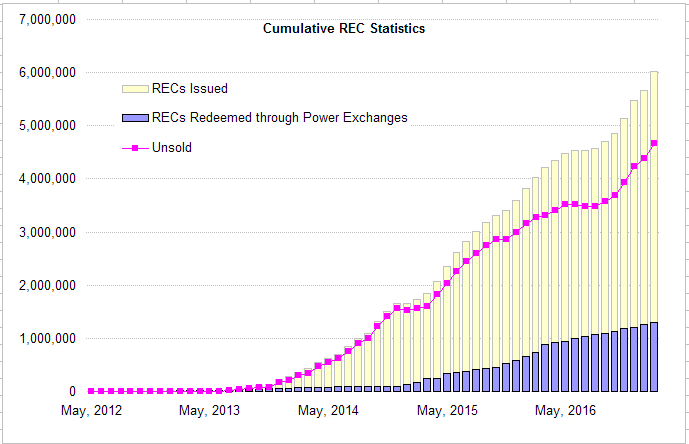

REC issuance has far exceeded REC redemption since Solar RECs were issued from 2012. There was a jump in redemption when price was reduced to 3500. This can be further reduced as current prices are valid till 31 March 2017. Inventory of unsold RECs is pilling up fast.

Following chart shows cumulative RECs issued, redeemed and unsold since 2012.

Source: https://www.recregistryindia.nic.in/index.php/general/publics/recs

Disc: No position. This is for discussion purpose only. Not a buy/sell recommendation.

3 Likes

So basically, they want to contribute 1/5th the equity and get 100% of the EPC done themselves. Nice idea. I’m not sure they can get better margins (per project) than they currently get - margins might even reduce. However since they get 4-7 times the number of projects (if things work out), it seems ok. What I like best is their apathy towards debt.

@ayushmit I’m dying to hear your views on this if you’re following this company.

1 Like

Company’s business model appears to be centered around RECs. This is from their IPO prospectus

They are running the parks and executing EPC contracts (at a low margin) and banking on sale of RECs to generate extra income. They can make money if purchases of RECs picks up. It will be interesting to see what effects the lower prices of RECs (if it is lowered) will have on volume of sales.

3 Likes

Concall - 23/Feb/17 - Promoter stake sale

We do not wish take debt and own assets.

We wish to be solution providers

We can join hands with bidder and get the EPC contracts

There are 10-15 competitors in EPC segment…it is highly competitive

EPC margin would be 9-10%

So what can company do to protect the margins and also not own assets?

Take a minority equity stake in the project

Illustration :

100 MW project. Cost 500 cr. Debt 400 cr. Equity 100 cr

Big players are saying Ujaas also take some equity

Say 20%…so Ujaas will need to contribute 20 cr i.e. 20% equity

The EPC contract would be 450 cr…company can earn margin of around 45 cr

There would be working capital and other financial costs….say 5 cr

Company would make net 40 cr on the equity investment of 20 cr

Once the project is stabilised the company can sell its minority stake to the

Majority player or 3rd party

The project is bidded around 15% IRR. After project is stabilised there is no

project risk…and hence the project can be sold at 13% IRR after 2 years

1 year construction, 6 months stabilisation and 6 month contigency

So after year2 the company can sell its equity for about 30 cr

Plus company would earn O&M revenue with high margin (1.25-1.5% of the project value)

24-02-17 24-02-18 24-02-19

-20 40 30

Xirr 158%

For this the company needs money for which Promoters have sold shares in market

The money received on sale of shares would be put in the company by way of loans/advances

or any other instrument

This is not the most ideal way of raising funds (selling in market).

The company tried a lot to raise money by QIP,etc etc…but coud not raise and lost couple of

good opportunities

Hence the promoters decided to raise the funds by selling.

In this whole exercise……promoters wont be the ones to gain the most

It would be for the benefit of the company and biggest beneficiary of this whole

exercise is of the company

Rumours in market about accounting/audit concerns

There is absolutely no problem. In last 25 years we have never received any qualification

There were rumours that no vouchers for 40% of exps. We are SAP company. It does not

allow to over write

(This point was very strongly defied by Anurag Mundra)

Why there was no mention in Q3 earnings call for raising funds. Why no transparency

Yes that’s the fact we have not discussed in last the call.

Can we change the auditor…one of the big four firm

Current auditors are most reputable in Indore. We are open to change in auditor and take

one of the big four firms.

How would we manage working capital for these large projects

Working capital is mainly in form of non fund based facilities.

some part of money raised would be invested as equities and some part would be used

as margin for working capital limits

There wont be increase in borrowing. Only LC/BG

7.75% diluted….raised close to 60 cr

Sold on market floors…… Not a negotiated deal. These are financial investors

The efforts of QIP were taking time

As of now we are not looking at this option for raising funds in future

We would lend money to company at soft interest rates

There is absolutely no challenge on banking front for raising working capital / long term

loans

Tender size that we are looking at more than 50 MW.

Ujaas would take minority equity stake between 5-25%

I assure that as of now we are done with diluting the stake

Why promoters did not pledge and take debt.

We are debt averse and don’t like debt

There is no pledge and there was not pledge ever

There is any expiry for REC…. Yes REC valid for two years

There is proposal to extend the expiry in a significant way

What is validity of current REC inventory

No exact figure but there is no danger of any expiry of REC inventory

Can the promoters not consider infusing money by way of Warrants/Preferntial Issue instead of loan

(I asked this question)

Response - As per regulation for 6 months I cannot do reverse transaciton i.e. cannot buy/subscribe after

selling the shares

Will the promoters consider after 6 months?

Yes it’s a good suggestion we would look at it

Total business size we are working is around 200 MW

If the company is unable to win the tenders what would you do with 60 cr?

We are pretty confident of winning the tenders. The market opportunity is huge

4 Likes

There is big doubt in my mind about the fate of REC inventory. A quick calculation from AR 2016 shows that company accrued REC inventory of 23.3 cr in FY15 and 23.10 cr in FY16.

The sale in FY16 and FY15 was 8.95 cr and 3.03 cr. The opening inventory as on 1.4.14 was 8.04 cr.

So in effect they have sold RECs of 3.94 cr (8.95 cr+ 3.03 cr - 8.04 cr) from the accrual of 23.3 cr in FY15 assuming FIFO basis. So 19.36 worth RECs (23.3-3.94) would expire by 31.March.17 giving the benefit that entire 23.3 cr in FY15 was accrued on 31.March.15.

The Management said that RECs have expiry of two years.

So if these RECs (accrued in FY15) are not sold by 31.march.17 then the company needs to w/o. The sale upto Nov 16 was 3 cr (concall with Valorem Advisors) That means they need to sell further 16.36 cr worth RECs (19.36-3) in remaining 4 months…which looks extremely difficult.

Also if one removes the REC accrual net of sale (23.1 + 23.3 - 8.95-3.04) i.e. 34.41 cr from two years PBT of FY16 and FY15 (41 cr + 19 cr) then PBT before net REC accrual = 26 cr for these two years instead of 60 cr.

The talk of margin of 10% in EPC and 15% in park business…is not justified if the above is correct.

Please re-verify the above and would be happy to know if I have erred in my analysis.

regards

Do not hold any position.

4 Likes

That is a wonderful summary of yesterday’s concall. Thanks…

i attended the call. Overall, my impression is there is no transparency. It has left a very bad taste among the investors. The way the sale has been done smells more than what promoter said on the call. He has lost credibility. I exited my position post the call.

@Vulture I might be missing a point here, but afaik there was no trading on NSE or BSE after the concall till now, due to Shivratri holiday on Friday[quote=“Vulture, post:158, topic:1467, full:true”]

i attended the call. Overall, my impression is there is no transparency. It has left a very bad taste among the investors. The way the sale has been done smells more than what promoter said on the call. He has lost credibility. I exited my position post the call.

[/quote]

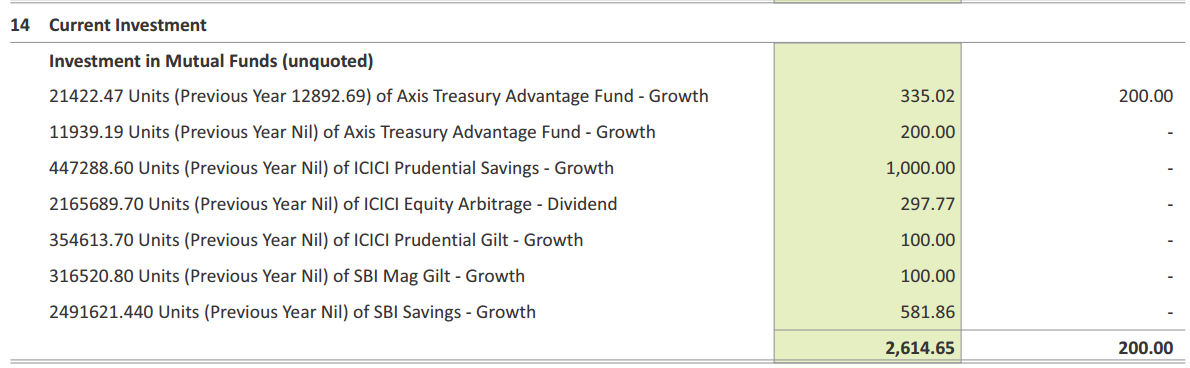

Company reported 18.7Cr in current investments (MF) as per the H1Fy17 B/s, which was 26 Cr. as on 31-Mar-2016 (Please see image of AR16, footnote below). Also, it had 49Cr cash on its B/s as of Sept-2016. These two figures add up to roughly 67Cr (18+49), which is similar to the amount (60Cr) raised by Promoters by way of stake sale of 7.8%

It would be interesting to understand that- Why did the promoters dilute their stake to raise 60Cr, which will be in turn brought back into the firm by way of loan from promoters. When instead they could have used the money already present on b/s.

Now, a counter argument/answer to the above question can be that- the cash is required to be maintained/earmarked for bank guarantee and other related stuff.

But, this would be a partial answer, as we need to understand the break-up of it. Also, the 18-20 Cr from MF is another avenue that should have been tapped for fulfilling any such fund needs. (Were these investments diluted?)

Regards,

Yogansh Jeswani

Disclosure: Not invested.

3 Likes

Sold ont he days of the call. The Promoter selling 60 Crs worth stock is a big negative for me. And that too in the open market and not negotiated, with no pre announcement. Reflects poor governance. There may be some urgency that we all are not aware of- some debt prepayment or private commitments to warrant such a sale. Not comfortable holding such a company.

@yogansh Company is making late payments, by 90-120 days, to Chinese suppliers. This has resulted in spike in cash on b/s.

@Vulture ohk, it makes sense that you sold before the call.

Discl.: Continue to hold full quantity.

Friends

Promoters sold 10% stake…agreed. And they hold 63% of the stake even

now…Will they do anything to bring down their stock value which is 90% of

their wealth…So, the 10% sale has some real reason…My gut feel is that

what they say is real…Keeping fingers crossed…will know the truth in the

next 3-6 weeks or so when they do/do not get EPC contracts due to this

strategy…

Disc: Holding the full qty till date…

Had planned to hold this for the next 2-3 years but this flaky behaviour of promoters put me off. Sold off on that day. Will keep it on trading watch list now.

I am yet to understand how come good fundamentals become bad overnight due to promoters selling of 8%. Are not they still holding 62%? If market capital is eroded they will be the biggest losers. Renewable energy is getting a lot of emphasis these days, would the management do something stupid at this junction? I would be waiting to see Q4 results and management already told in CNBC that Ujaas even quarters are normally better than odd quarters. In the meantime, who knows they might be able to secure new projects and people will again become bullish?

Disclosure: Holding and plan to add more if price comes 32 or below.

1 Like