I don’t think there will be any decrease in ad spend.Infact I see the ad spend increase due to clearance of old stock with all GST offers.

Year gone by was flattish with topline growing by a whisker…operating margins were more or less stagnant. Is anybody still following thus company? What are the triggers to unleash revenue growth here. Going digital was supposed to bode well fir the industry in terms if operating leverage, but isn’t visible so far.

Its english channel is at no 3 position. Aaj tak despite retaining its position isn’t able to consolidate it further. My question - is this a valuevtrap at 14 pe? Debt free company, great brand, but unable to milk it?

I think the Dec Quarter last year was bad for TV today. It could be due to demonetization. Hence there was not great sales growth last year.I think it was same across most companies. This year could be better. If there are state elections that could trigger revenue growth specifically for News Channels. If you look at Mar-17 the results were good as there were state elections. There are state election this year in gujarat and himachal pradesh so that quarter is crucial. As far a value trap is concerned it appears to be the less expensive compared to other media stocks . If compared across different financial parameters in totality like ROCE, Earning yield .etc it does not look expensive.

This does look cheap…no doubt. And has good return ratios. What i am trying to understand is if the future potential is there to improve the topline while maintaining bottomline here. They have got high profile anchors like Rajdeep, Karan, Rahul Kanwal, but the revenues that were expected to boost haven’t yet boosted. Usually people keep switching the channel, so is there any moat despite being a good brand?

TV today is number one in Hindi and Number 3 in English news channel for some years now.This means they have ability to stay at top and have some moat. They also have retained their key employees.As far as switching channels is concerned it should be a major threat.The market cap of the companies of news channel in US like fox is in Billions and TV Today is in millions. In spite of digitization these channels are still around. Even though they still get news through other medium like twitter ,digital ,we still watch news channels. However India has lot of regional channels too so that could affect the pricing power. But TV today is just making only 100 crores in net profit so i feel there is a long way to go. The reach of Indian news channels are far greater than US due to size of the population . With increase in rural income and more sector moving to organised the ad spend and ad rate could only go upwards . However its hard to predict what would happen in the short term

Does any one has any clue what is happening inside TV Today ?

See Koel Purie Director resigning today, and 2 days back it was CEO Ashish Kumar Bagga resigning. However dont see stock price reacting much to Ashish Kumar’s resignation

TV Today is trading at 13.3 X FY17 and 12 X FY18E (assuming no black swan event) with 200 Cr net cash on book. Can such a undervalued FCF stock fall further ?

Most of the youngsters now day’s are streaming content from smart phone devices with screen mirroring. Many of my friends now directly stream content from hotstar etc on TV. But I believe this is more for entertainment content. For sports, news channel - real time streaming as its own importance. So this are should not be affected.

Agreed, it’s quite undervalued and hence I am interested in it. However, the Director & CEO resigning this week believe it was not known to the market prior and hence it was not valued in the price. Also, I think in short term markets react more on news and in long term it works more on valuation. So I am curious to understand why both of them resigned as well as not much price movement.

Yes, most of the youngsters are streaming online content. However, these youngsters are from urban (~1/3rd of India population) and also youngsters streaming online would be at most ~1/3rd of urban population --> So overall almost 1/9th population. Rest of it should be watching news on TV. Also, considering recent digitization and ongoing inclusion at rural area will lead to substantial subscription revenues and increased customer base. And Aaj Tak being #1 Hindi News channel, should be the most benefitted out here.

Note: My views might be biased, suggestions invited.

Debt Free

Consistent Revenue Growth Since Last 14 Years

Brand Value in Business

Marketcap/Revenue less than half compared to peers

Cheapest company among top 4 in its sector

P/E near or under 20 when Peers trade at 35+ easily.

Consistent Dividend since last 14 years.

The business has presence in almost all average Indian Households.

Triple digit net profits (highest annual profit in fy17 since listing)

Double Digit net margins

Tv Today Network.

Disclosure: Not invested

~Long post alert~

This thread has been dormant for over a year now but this company came on one of my screens and I decided to take a look. I have looked at the numbers for last 5 years & also highlighted the impact of the “New tariff Order” issued by TRAI. I do not understand why this company is touching 52 week lows and is available at a PE of ~13X (based on TTM earnings) because the numbers till now don’t look bad at all! So here goes:

-

TV Today earned Rs. 123 crores (standalone) in FY18 and Rs. 110 crores in first 3 quarters (standalone) of FY19. The company is available at a market capitalisation of Rs. 1900 crores.

-

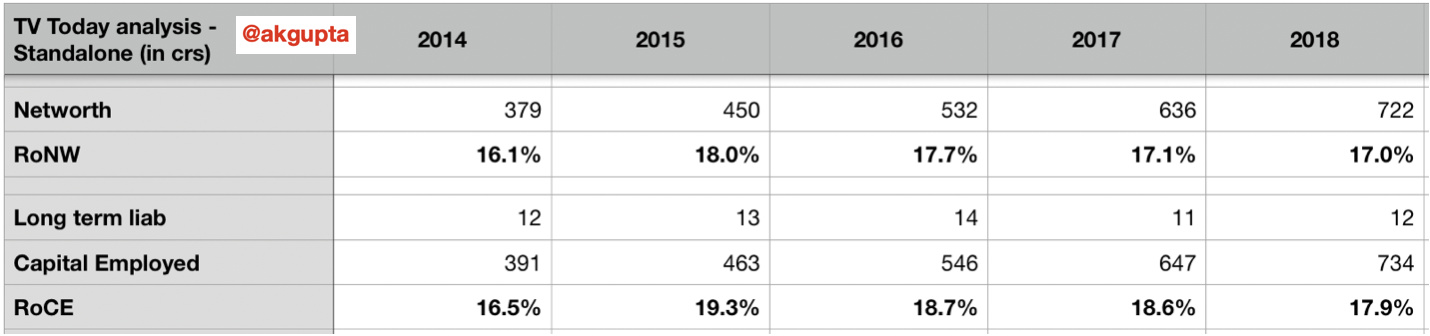

The Book Value or Net Worth of of the company as of FY18 (standalone) is Rs. 722 crores with approximately Rs. 300 crores in cash & bank balances (200 in current deposits & 100 in term deposits).

-

The company has grown its Operating revenue by ~15% over last 5 years from Rs. 400 crores in FY14 to Rs. 715 crores in FY18. There are 4 streams of revenues - Advertising, Subscription, Digital & Others. Here is a brief snapshot of 5 year performance of these 4 segments:

- While advertising brings in the most revenues (~85%-90%), Digital is growing fast. As the below snapshot proves, Digital’s contribution to Operating revenues has gone from nil to ~9% in just 3 years. This is in keeping with the overall strategy of the company to boost digital content consumption. Also, Subscription revenue is steadily declining:

- Company’s EBITDA margin is a handsome 30%+. As the below snapshot shows, EBITDA margin has never been less than 30%. In FY18 it was 34% & in the first 3 quarters of FY19, EBITDA margin is also 34%: (Could it be that Digital revenue is EBITDA accretive…will be good to find out)

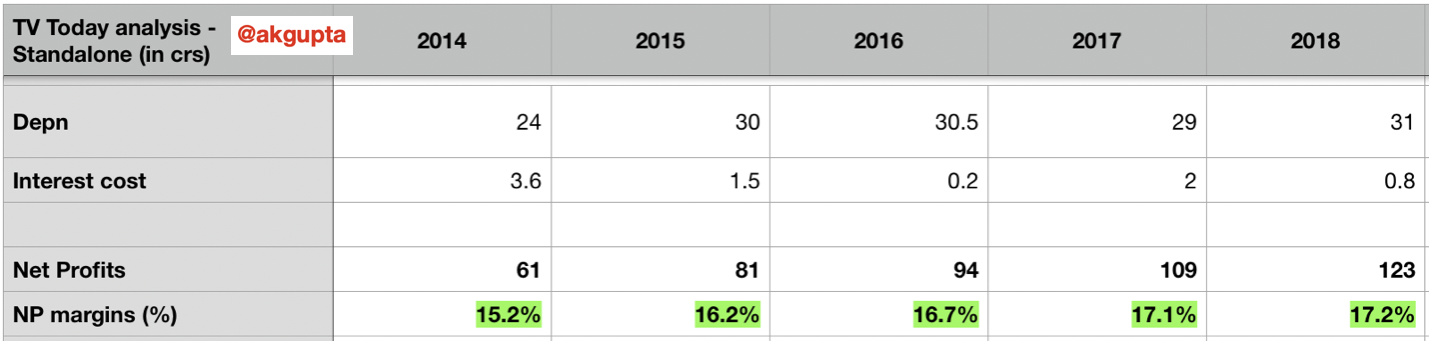

- Company has a steady depreciation of around 30 crores pa & finance cost is on a declining trend - the company paid Rs. 3.6 crores in interest in FY14 & that has come down to 0.8 crores in FY18. For YTD FY19, company paid out Rs. 26 lacs in interest. So the company is debt free & more importantly that it doesn’t need a lot of fixed capital investment to grow.

All of these factors (growing revenues, high & stable EBITDA Margin, steady depreciation & declining interest expense) are helping the company grow its Net profits at an impressive 19% CAGR from FY14 (Rs. 61 crores) to FY18 (Rs. 123 crores)

- The company employed average capital of Rs. 690 crores in FY18 to earn profits before interest & taxes of Rs. 124 crores which means a healthy RoCE of 18%. In fact, the trend of high RoCE is visible all throughout last 5 years:

- Television is a working capital intensive business which shows in the numbers as well. From FY14-18, Working capital employed in the business went up by 3 times from Rs. 108 crores to Rs. 295 crores. The majority of this working capital is in Cash & bank (Rs. 199 crores) & trade receivables net of payables (Rs. 100 crores):

-

In addition to working capital of Rs. 295 crores, company needs fixed business assets (PPE & intangibles) of Rs. 255 crores. The good thing is the need for Capex to grow earnings of the business is quite low - from FY14 to FY18, Non-current business assets grew from Rs. 217 crores to Rs. 255 crores, while profits more than doubled.

-

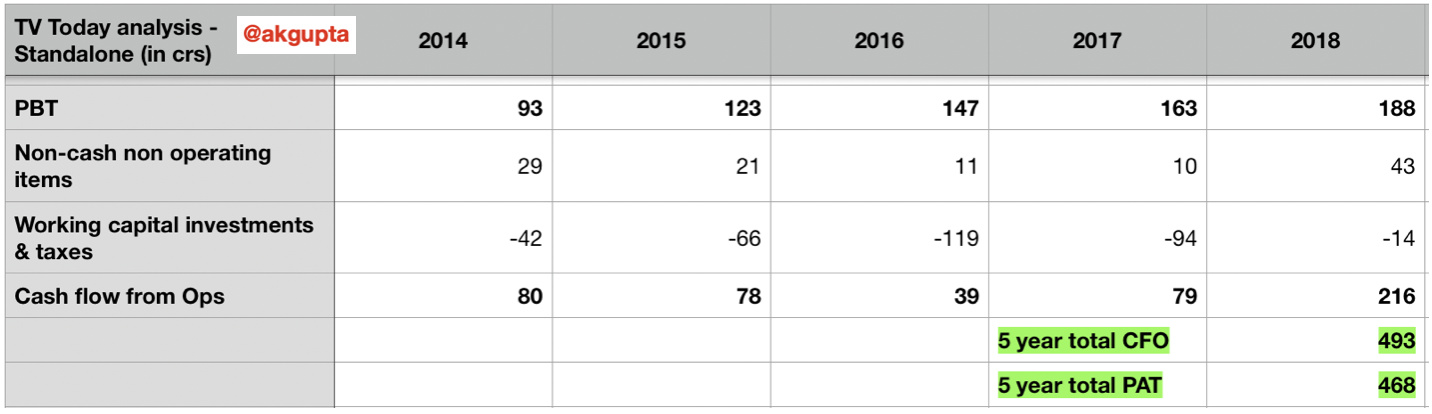

Another positive aspect of the business is this - combined cash flow from operations over the last 5 years is Rs. 493 crores exceeds combined 5 year Profits after taxes of Rs. 468 crores:

-

It is quite evident that TV Today has a very good looking P&L, Balance Sheet & Cash flow picture - today.

However what matters is can the company sustain this performance over the next 5 years ?* For this, it’s important to understand the “New Tariff Order” issued by TRAI, the regulator.

What is the NTO?

-

The New Tariff Order seeks to provide more choice to TV audiences by forcing cable/DTH operators - like Tata Sky or Airtel TV - to provide all TV channels on an a’ la carte basis rather than in a bundled way (Deluxe Pack, Super Deluxe Pack etc). Each channels monthly price will be clearly shown by operator on the Program Guide screen.

-

However, Broadcasters - like TV Today Network - can choose to provide their whole bouquet of channels to audiences in a bundled way. For eg. If Viacom18, a broadcaster, has 10 channels ranging from entertainment to news to sports, it can provide all those channels as a bundle for a defined price per month or per year.

-

The MRP of any Pay based channel bundle that the customer chooses shouldn’t be less than 85% of the sum of individual prices of those channels. Further, there is an upper cap of Rs. 19 for any channel.

-

“The NTO was implemented on February 1, 2019 & the extended deadline to complete the migration from the old framework to the new one is March 31, 2019 . As per TRAI, India has about 170 million television households of which around 100 million are cable subscribers while 70 million uses DTH (Direct-To-Home).”

-

“On February 12, 2019 TRAI was quoted announcing that 90 million homes have already migrated to the new tariff order of which 65 million were cable TV households and 25 million were DTH subscribers.” [Refer this link]

-

An interesting article I came across in Livemint mentions some pointers as to how the NTO is affecting all stakeholders in the TV business:

- Customers are not happy since many of them (54% as per a survey) are paying more.

- Broadcasters are not happy since many of them are seeing their subscription rates drop.

- Advertisers are confused & will likely remain so unless viewership ratings settle after the migration to new framework is complete for all 17 crore of population.

- Disruption from online mediums (Airtel TV, Jio TV) which are offering 300-400 channels free on the go is a major threat for Pay TV’s ad based business model.

- Consolidation of channels by broadcasters looks imminent. “Broadcasters may re-evaluate the feasibility of certain channels (which are niche & don’t attract mass genres) in their portfolios. For instance, Sony India recently shut down three premium HD channels—Sony Rox, Sony LePlex and Ten Golf.”

Implications of NTO on TV Today’s business:

-

By TV Today’s Chairman’s admission, “key impact of the order would be a possible reduction in number of channels to end customer, closure of under performing channels and regulation of channel prices. This could have an impact on subscription revenue and distribution cost of your Company.” [AR FY18 Chairman’s comments]

-

So this order raises some questions which will decide TV Today’s future: Will 17 crore odd households (currently subscribing to cable/DTH) choose “Aaj Tak” in their respective bundles? Because if people don’t subscribe to “Aaj Tak”, its viewership will decline & it will lose ad revenue as well which is ~85-90% of total revenue as we saw above.

Side Note:

- Promoter Aroon Purie is buying shares from the open market. In Feb’19, he has bought shares worth Rs. ~2.1 crore. HDFC Small cap fund has also bought shares in the last quarter.

Disclosure: Invested recently as I think:

- the company will keep in performing despite the NTO. “Aaj Tak” clearly has staying power which shows in both viewership numbers over the years & financials.

- The new digital initiatives including the “Tak” brand of online only channels catering to not just news but also lifestyle audiences bode well for growth in digital revenue.

- There is a possibility that lagging channels might have to shut operations which will help in industry consolidation as well.

- The price is reasonably attractive. I think the market is reacting to the adverse impact of NTO. The exact impact should become clear over the next 1 year.

11 Likes

This new tariff order will lead to consolidation on the basis of language and quality. India Today is still featured among top 5 english news channels while Aaj Tak retained its top position in the list of hindi news channels.

In last week of Dec 2018, India Today had 2,19,000 weekly impressions while in mid-march it has 2,11,000 weekly impressions.

For Aaj Tak, in the last week of 2018 it had 13.01 crore weekly impressions and in mid-march it has 14.58 crore weekly impressions.

The viewership loss in english news channel is miniscule if compared to the gain in hindi news channel.

News is not a dying business but with digital, everything is getting more focused and consumer-centric. Their foray in radio was something of interest and seemed a way to extend their brand into entertainment but seems they did not want to invest because of long gestation period or competition. Stand-alone not sure how long can they wade of losing the sheen and edge as generations change it also changes their likings, and spend patterns. TV today is trying to get a foothold into the rural market whereas advertisers and marketers are focusing more on a niche market and the audience who are compulsive spender rather than a larger audience. An interesting twist and it needs to be seen the quality of management in thinking beyond the boundaries. They have the cash to play but are they willing to take the risk or going to run their time tested business model and keep hoping they will succeed.

I think republic Bharat could prove to be a serious competition. If Rohit Sardana goes to republic Bharat, thenso would all the viewership.

Hi Viraj

Can you please share the source of this information…the number of impressions ?

Thanks

Here’s the source - https://www.bloombergquint.com/bq-blue-exclusive/new-tv-tariff-rules-trigger-collapse-of-english-genre

1 Like

See I don’t think this business is dependent on a particular journalist joining or leaving a channel. Yes some anchors become popular & it’s good to have them. But don’t you think Aroon Purie will know who’s important for his business and who he can afford to lose in a poaching attempt ? I think one has to put in some faith in the promoter as well who has a lot more to lose than us retail investors !

3 Likes

What all things constitutes the digital revenue? TV today streams on hotstar so does hotstar share some part of revenue with them on the basis of impressions etc? Likewise what are other mediums of revenue through digital?

Today, the company is available at 6 PE net of cash. It has no debt with 30% operating margins, 30% ROCE, 20% ROE and no equity dilution for last 9 years.

Thinking aloud, the markets are usually forward looking and it seems that they are not sure of the future of news media considering the onslaught of TRAI orders and OTT apps along-with news app like InShorts etc. In my opinion all these negatives are already priced in and this looks like a too negative reaction for the stock.

The yearly ad spend of HUL is 4000 crores while the market cap of Aaj Tak and India Today combined is 1800 crores only. In the words of Ramesh Damani, HUL can take over and rename the channel to Unilever Aaj Tak